MNI ASIA OPEN: Still Waiting For U.S. Data Fog To Lift

Nov-13 2025 20:26By: Tim Cooper

APAC

MNI (NEW YORK) -

EXECUTIVE SUMMARY

- MNI INTERVIEW: Private Credit Poses Systemic Risks - Ghamami

- MNI BRIEF: Fed's Kashkari Says Inflation Is Still Too High

- MNI BRIEF: Fed's Daly Keeping Open Mind On December Rate Move

- MNI BRIEF: Musalem - Limited Room For Further Fed Easing

- US DATA: Dept of Labor Likely To Publish Payrolls Next Week: Yahoo Finance

NEWS

MNI INTERVIEW: Private Credit Poses Systemic Risks - Ghamami

A lack of transparency in the rapidly-expanding market for private credit raises risks to stability, particularly as it deepens links between different parts of the financial system, former Securities and Exchange Commission economist Samim Ghamami told MNI. “Private credit has deepened the interconnectedness of the financial system in times of stress,” Ghamami, also a former economist at Treasury and the Fed board, said in the latest episode of MNI’s FedSpeak Podcast. “Under large negative shocks, a highly interconnected financial system can actually become highly fragile.”

MNI BRIEF: Fed's Kashkari Says Inflation Is Still Too High

Federal Reserve Bank of Minneapolis President Neel Kashkari said Thursday inflation pressures are running above the central bank's target at about 3%. "We have inflation that's still too high, running at about 3%. Some sectors of the US economy look like they're doing great. Some sectors of the labor market look like they're under pressure," he said in welcoming remarks at the Minneapolis Fed’s Opportunity and Inclusive Growth Institute’s annual research conference. (See: MNI INTERVIEW: More Fed Cuts Risk Inflation Spike-Weinberg)

MNI BRIEF: Fed's Daly Keeping Open Mind On December Rate Move

San Francisco Fed President Mary Daly said Thursday she's keeping an open mind about the December FOMC meeting, adding it would be premature to lean in either direction of an interest rate cut or hold. "I really think there's a premium on waiting to decide until you have as much information as you can possibly have to make a good decision, but not waiting so long that you become inactive, because you're paralyzed with not having the last piece of information you think you might use," Daly said in Q&A at an Institute of International and European Affairs event in Ireland. "I have an open mind, but I haven't made a final decision on what I think."

MNI BRIEF: Musalem - Limited Room For Further Fed Easing

Federal Reserve Bank of St. Louis President Alberto Musalem cautioned Thursday there's limited room to ease monetary policy after already lowering the central bank's benchmark overnight rate 150 bps since 2024. "We need to proceed and tread with caution, because I think there's limited room for further easing without monetary policy becoming overly accommodative," he told the Evansville Regional Economic Partnership in Indiana. "Remember, inflation is still at 3% and I believe policy right now is somewhere between modesty restrictive and neutral and is probably getting closer to neutral than to modestly restrictive."

US DATA: Dept of Labor Likely To Publish Payrolls Next Week: Yahoo Finance

Yahoo Finance's Jennifer Schonberger reports on X.com citing the Department of Labor that the September nonfarm payrolls report will likely be out next week, and that the BLS will produce an updated release schedule "in the coming days".

SECURITY: Trump Briefed On Military Operations In Venezuela, Keeps Options Open (CBS)

CBS reports that the senior military officials have presented President Donald Trump with “updated options for potential operations in Venezuela, including strikes on land,” but no final decision has been made. The report tracks with a recent NYT piece claiming Trump has been presented with a range of options, “including direct attacks on military units that protect President Nicolás Maduro and moves to seize control of the country’s oil fields.”

MNI: EU Member States Plot Further ETS2 Pushback -Officials

A one-year delay in the extension of the European Union’s ETS2 emissions trading scheme to heating and road transport is likely be only the first step in a campaign by several member states to further dilute or even kill the measure, EU officials told MNI. The Nov 4-5 climate talks in Brussels which resulted in agreement by energy ministers to delay the extension of ETS2 until 2028 ran through the night, with one senior official from an EU state describing the marathon debate and involvement of prime ministers as "unprecedented".

MNI BRIEF: EU Eyes Common Borrowing Options For Ukraine

The European Commission and EU states are looking at common borrowing as one alternative solution for Ukraine' urgent and looming financing needs, Economy Commissioner Valdis Dombrovskis confirmed Thursday. Dombrovskis stressed that the option of of using cash balances from immobilised Russian assets mainly held by Euroclear in Brussels to provide Ukraine with EUR140bn in grants remained the "most feasible" route, although strong and continuing Belgian objections are pushing Brussels to consider other options.

EU Debating Pooling Of US Dollars To Lessen Fed Reliance - Reuters

Reuters has reported that “European financial stability officials are debating whether to create an alternative to Federal Reserve funding backstops by pooling dollars held by non-U.S. central banks in a bid to reduce their reliance on the U.S. under the Trump administration, five officials familiar with the matter said.”

SNB: Tschudin Sees SNB Monetary Policy Having Desired Effects On Funding Markets

SNB governing board member Petra Tschudin strikes a content tone at the SNB's money market event in Geneva in her speech about "Bank funding costs: latest developments from a monetary policy perspective". She concludes that the SNB's monetary policy continues to have the desired effects on funding markets.

MNI INTERVIEW: Banxico Nearing End Of Easing Cycle - Zaga

The Central Bank of Mexico is likely near the end of its easing cycle after a 25-basis-point rate cut last week to 7.25%, as core inflation remains at high levels, former Economy Ministry deputy general director Daniel Zaga told MNI.

MNI INTERVIEW: Czech Fiscal Gap To Hit 3% GDP-Council Chair

The Czech Republic’s new government is likely to increase the country’s fiscal deficit to 3% of GDP by the end of 2027, the chair of the Czech Fiscal Council told MNI in an interview, adding that while the chances of agreeing a 2026 budget have increased, there are still major gaps to be filled.

US TSYS: Treasuries Weaken As Doubts Grow Over Next Fed Cut

Renewed skepticism over prospects of a Fed cut in December and a weak long-end auction saw the Treasury curve bear steepen Thursday.

- 2025 FOMC voter and Boston Fed President Collins's commentary late Wednesday that she preferred a rate hold in December wasn't entirely a surprise given her previous statements, but combined with other hawkish views among current voters since the October meeting, there now looks to be an increasingly sizable and vocal minority calling for a hold.

- In keeping with this theme, Fed commentary Thursday skewed neutral-to-hawkish: SF's Daly and Minneapolis's Kashkari, who are two of the 19 FOMC members among the most likely to support a December rate cut, were non-committal on the prospect Thursday; meanwhile Cleveland's Hammack and St Louis's Musalem (also a 2025 voter) continued to portray a patient stance.

- Overall, prospects for a Dec cut were pared to 50/50 vs closer to 65% before Collins's appearance.

- But the curve leaned bear steeper on the day, in part because another weak 30Y Bond auction (4th tail in the last 5 sales) followed on from Wednesday's 10Y tail, pushing long-end yields to session highs. As we write, the 30Y yield is set for its joint-highest close since October 9.

- Latest cash levels: The 2-Yr yield is up 2.3bps at 3.5909%, 5-Yr is up 3.7bps at 3.7082%, 10-Yr is up 4.4bps at 4.1134%, and 30-Yr is up 4.1bps at 4.7054%. Dec 10-Yr futures (TY) down 8.5/32 at 112-23.5 (L: 112-22 / H: 113-01.5)

- The above largely overshadowed the lack of developments on the data front after Wednesday night's conclusion to the government shutdown. Indeed the likely lack of new CPI and up-to-date labor market reports before the December 10 FOMC decision implies that it will be even more difficult to shift hawks' inertia.

- There had been some anticipation that we would get a schedule Thursday for shutdown-postponed data releases from the BLS, but Yahoo Finance cited the Labor Department in saying an updated schedule would be out "in the coming days" while September's nonfarm payrolls report would likely be out next week.

- Even if we have to wait until Friday or later to get an update on data releases, we're still expected to get state-level weekly jobless claims data after the close (and analyst estimates of national-level claims). Friday's calendar is largely Fed-speak related (Schmid, Logan, and Bostic make appearances) with PPI and Retail Sales almost certain to be postponed.

DATA

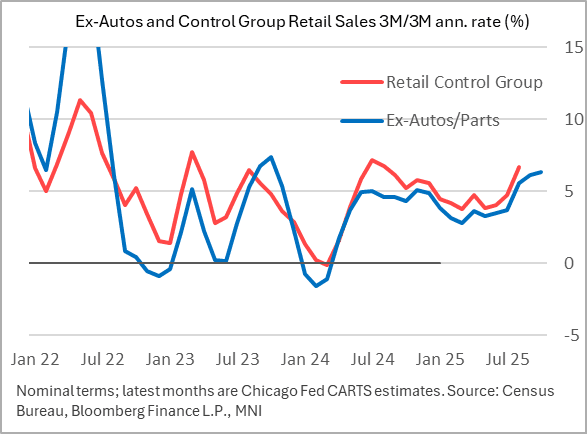

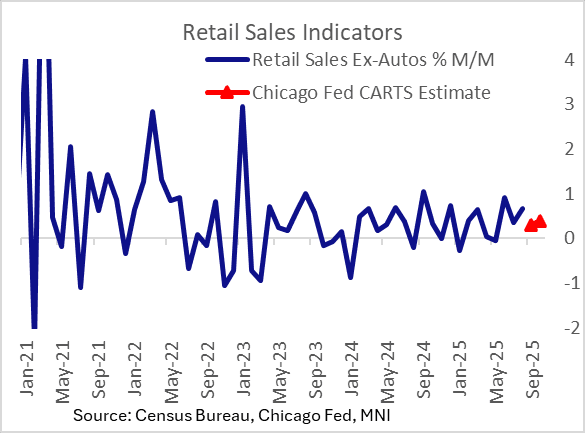

US DATA: Chicago CARTS Points To Strong Core Retail Sale Dynamics In October

The Chicago Fed's final CARTS estimate for October ex-autos/parts retail sales is for 0.39% M/M growth, up from 0.30% they estimated for September.

- Of course we haven't yet gotten the Census Bureau's official September data due to the federal government shutdown, and Friday's advance release for October is almost certain to be postponed.

- In the meantime we have other proxies for retail sales growth over the last couple of months and for the most part they've been solid, including CARTS and Redbook weekly sales.

- Though the ex-autos sales figures would represent a slowdown from 0.66% in August, and vehicle sales look to have fallen sharply in October (due largely to expiring government EV incentives) which will depress headline sales, "core" retail sales continue to grow at an elevated rate going into Q3.

- If the CARTS estimates are correct, then ex-autos retail sales grew at a 6.3% quarterly (3M/3M) annualized rate in October, which would be the fastest since October 2023 and a pickup from the 3.5% recorded in June (Q2).

- That's in nominal and not real terms, but suggests no discernable letup in consumption overall, even when inflation-adjusted.

- As the chart below shows, ex-autos are a good proxy for the GDP-input Control Group retail sales (which exclude auto sales, the largest single retail category), and suggests some of the strongest growth in years in that category continues.

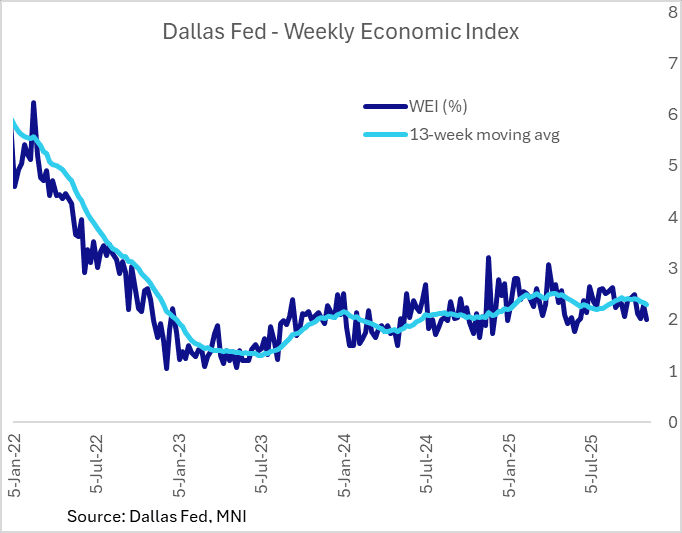

US DATA: Dallas Fed Weekly Econ Activity Index Starting To Roll Over

The Dallas Fed's Weekly Economic Index (WEI) printed the lowest in 22 weeks in the week to Nov 8, at 2.00% (scaled to 4-quarter GDP growth), vs 2.27% prior. That saw the 13-week (ie quarterly) moving average dip to 2.30% from 2.34% prior, lowest since mid-August.

- In keeping with the federal government shutdown's data blackout, however, there are some increasingly large holes in the Dallas Fed's visibility: "Initial claims for unemployment insurance, fuel sales, and electricity output are missing for the week ended Nov. 8 and continuing claims for unemployment insurance are missing for the week ended Nov. 1."

- Once official data is released for the missing weeks, the Dallas Fed will retroactively revise the series.

- For now though it looks as though growth is slowly rolling over versus a pickup in October.

- So far this quarter it's tracking the equivalent of roughly 1.5% Q/Q SAAR growth for Q4, vs around 4% in each of Q2 and Q3 after a small contraction in Q1 (which proved to be roughly accurate, around the actual/Atlanta Fed GDPNow estimates).

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

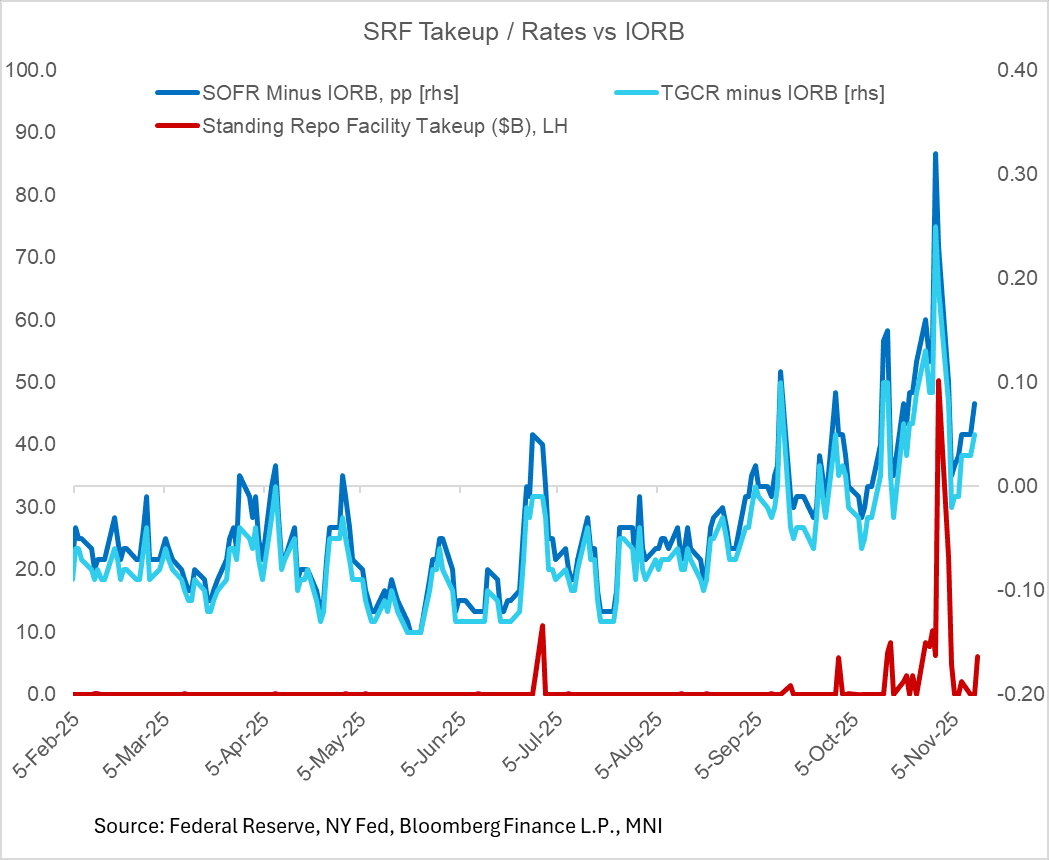

US TSYS/OVERNIGHT REPO: Secured Rates Remain Elevated, Little Relief Imminent

As anticipated, funding market rates remained firm Wednesday, in part due to Treasury bill settlements though overall suggestive of reserve conditions closer to "ample" than "abundant".

- SOFR picked up 3bp Wednesday (3.98%) with TGCR up 2bp (3.95%) with both remaining above the Fed's IORB rate (3.90%), while there was also continued takeup of the Fed's standing repo facility in this morning's operation ($3.9B, after $6.1B total Wednesday).

- After raising $14B in net cash Wednesday through bill settlements, Treasury raises $23B Thursday which is expected to keep rates underpinned.

- There might be some subsiding Friday, but Monday sees another $27B in coupon settlements before GSE cash is expected to come into market from next Tuesday to apply some downside pressure on rates (offsetting $14B in bill settlements on Tuesday).

- However, there was no change in effective Fed funds (3.87%).

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 3.98%, 0.03%, $3209B

* Broad General Collateral Rate (BGCR): 3.95%, 0.02%, $1263B

* Tri-Party General Collateral Rate (TGCR): 3.95%, 0.02%, $1231B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 3.87%, no change, volume: $77B

* Daily Overnight Bank Funding Rate: 3.87%, no change, volume: $156B

BONDS: EGBs-GILTS CASH CLOSE: Bear Steeper As US Government Re-Opens

European curves bear steepened Thursday.

- After a modest uptick in early trade, US Treasuries led a global rise in yields following Federal Reserve commentary late Wednesday that cast doubt on a December rate cut, as well as confirmation that the federal government would re-open Thursday.

- That US-led weakness, which started in the late European morning, continued in orderly fashion throughout the rest of the cash session.

- Both the UK and German curves bear steepened on the day, failing to benefit from any kind of safe-haven bid as equities pulled back - with Bunds underperforming Gilts at the long end.

- Periphery/semi-core EGB spreads traded mixed but overall instruments were flat to Bunds.

- UK Q3 preliminary GDP came in slightly softer-than-expected (0.1% Q/Q vs 0.2% cons, 0.3%% prior) but the data was "noisy" and it had little apparent impact on BOE cut pricing.

- Eurozone August industrial production was likewise softer than expected with typical noise in the data (Ireland-related).

- Friday data includes some Eurozone data (second reading of Q3 GDP along with prelim Q3 employment), as well as final October inflation readings (France, Spain). There's also commentary scheduled from ECB's Lane, Ecriva, and Vujcic.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3bps at 2.028%, 5-Yr is up 4.6bps at 2.293%, 10-Yr is up 4.5bps at 2.688%, and 30-Yr is up 5.2bps at 3.28%.

- UK: The 2-Yr yield is up 3.6bps at 3.764%, 5-Yr is up 3.4bps at 3.901%, 10-Yr is up 3.9bps at 4.437%, and 30-Yr is up 4bps at 5.231%.

- Italian BTP spread up 0.3bps at 73.1bps / French OAT down 0.5bps at 73.1bps

EUROPE OPTIONS: Call Structure Activity Remains Predominant In European Rates

Thursday's Europe rates/bond options flow included:

- ERH6 97.75/9800ps, bought for 6 in 10k

- ERM6 98.06/98.18/98.43/98.56c condor, bought for 2.75 in 4k

- ERM6 98.25/98.50cs, bought for 2.5 in 3k

- 0RM6 98.00/98.25cs, bought for 6 in 20k

- SFIM6 96.70/96.85/96.90/97.05 thin body call condor paper paid 2.75 on 6K

- SFIM6 96.55/96.70 call spread vs. 96.50/96.30 put spread paper paid 1.0 on 4K.

- SFIM6 96.85/97.00cs, bought for 3 in 5k

FOREX: USD Slide Continues, Further De-linking FX with Rates & Equities

- As the US government reopened, the USD fell against broader G10, prompting a new November low for the USD Index. In further evidence that the currency and rates markets are diverging, the USD found very little solace in either the strength and show above 4.11% in the US 10y yield, or the persistent trimming of Fed rate cut pricing for the December FOMC, which now stands at less than 50%.

- The USD is slipping as markets seem to be adopting a pro-growth phase after the end of the government shutdown, which was estimated to be costing as much as $15bln per day - however the test for the USD's ability to sustain itself at lower levels will be tested by the incoming data. This covers not only the official agency releases, but the private sector data also, including next week's ADP weekly jobless estimate.

- That said, a negative session for equities paints a less positive picture. Underperformance in megacap tech names (NVIDIA dropped near 3.5%) undermined headline index performance, which dragged AUD, NZD and other growth proxy currencies off highs, while favouring haven FX including JPY and CHF.

- Meanwhile, Gold saw renewed gains early Thursday, putting prices at the highest since the October 21 pullback. While prices have faded, a positive close today would be the 7th consecutive higher daily close. Only partial pricing for a Dec Fed cut opens up potential for a dovish turn in rates should incoming data surprise to the downside, which should prove positive for gold prices.

- Focus Friday shifts to the potential publication of advisories and schedules for the still-missing US economic releases. With the government still in the process of reopening, we expect September NFP to be released imminently, and in it's full format, however the October release that follows may be lacking key data on the unemployment rate - a message affirmed by White House Advisor Kevin Hassett today.

- Chinese retail sales and industrial production data are due Friday, with speeches also due from ECB's Escriva, Vujcic, Elderson & Lane, while Fed's Schmid, Logan & Bostic (who announced his retirement this week) round things off in the US.

FX OPTIONS: Larger FX Option Pipeline

- EUR/USD: Nov17 $1.2100(E1.4bln); Nov19 $1.1800(E1.5bln)

| Date | GMT/Local | Impact | Country | Event |

| 14/11/2025 | 0001/0001 | KPMG/REC Report on Jobs | ||

| 14/11/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 14/11/2025 | 0200/1000 | *** | Retail Sales | |

| 14/11/2025 | 0200/1000 | *** | Industrial Output | |

| 14/11/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 14/11/2025 | 0700/0800 | ** | Unemployment | |

| 14/11/2025 | 0745/0845 | *** | HICP (f) | |

| 14/11/2025 | 0800/0900 | *** | HICP (f) | |

| 14/11/2025 | 0900/1000 | Foreign Trade | ||

| 14/11/2025 | 1000/1100 | * | Trade Balance | |

| 14/11/2025 | 1000/1100 | *** | EZ GDP 2nd (Flash) | |

| 14/11/2025 | 1030/1130 | ECB Elderson Keynote at ECB Banking Supervision Forum | ||

| 14/11/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 14/11/2025 | 1330/0830 | ** | Wholesale Trade | |

| 14/11/2025 | 1330/0830 | *** | Retail Sales | |

| 14/11/2025 | 1330/0830 | *** | PPI | |

| 14/11/2025 | 1330/1430 | ECB Elderson Remarks at COP30 Finance Day | ||

| 14/11/2025 | 1500/1000 | * | Business Inventories | |

| 14/11/2025 | 1500/1600 | ECB Lane Panel at Workshop on International Macroeconomics and Finance | ||

| 14/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1930/1430 | Dallas Fed's Lorie Logan | ||

| 14/11/2025 | 2020/1520 | Atlanta Fed's Raphael Bostic |