US TSYS: Treasuries Weaken As Doubts Grow Over Next Fed Cut

Renewed skepticism over prospects of a Fed cut in December and a weak long-end auction saw the Treasury curve bear steepen Thursday.

- 2025 FOMC voter and Boston Fed President Collins's commentary late Wednesday that she preferred a rate hold in December wasn't entirely a surprise given her previous statements, but combined with other hawkish views among current voters since the October meeting, there now looks to be an increasingly sizable and vocal minority calling for a hold.

- In keeping with this theme, Fed commentary Thursday skewed neutral-to-hawkish: SF's Daly and Minneapolis's Kashkari, who are two of the 19 FOMC members among the most likely to support a December rate cut, were non-committal on the prospect Thursday; meanwhile Cleveland's Hammack and St Louis's Musalem (also a 2025 voter) continued to portray a patient stance.

- Overall, prospects for a Dec cut were pared to 50/50 vs closer to 65% before Collins's appearance.

- But the curve leaned bear steeper on the day, in part because another weak 30Y Bond auction (4th tail in the last 5 sales) followed on from Wednesday's 10Y tail, pushing long-end yields to session highs. As we write, the 30Y yield is set for its joint-highest close since October 9.

- Latest cash levels: The 2-Yr yield is up 2.3bps at 3.5909%, 5-Yr is up 3.7bps at 3.7082%, 10-Yr is up 4.4bps at 4.1134%, and 30-Yr is up 4.1bps at 4.7054%. Dec 10-Yr futures (TY) down 8.5/32 at 112-23.5 (L: 112-22 / H: 113-01.5)

- The above largely overshadowed the lack of developments on the data front after Wednesday night's conclusion to the government shutdown. Indeed the likely lack of new CPI and up-to-date labor market reports before the December 10 FOMC decision implies that it will be even more difficult to shift hawks' inertia.

- There had been some anticipation that we would get a schedule Thursday for shutdown-postponed data releases from the BLS, but Yahoo Finance cited the Labor Department in saying an updated schedule would be out "in the coming days" while September's nonfarm payrolls report would likely be out next week.

- Even if we have to wait until Friday or later to get an update on data releases, we're still expected to get state-level weekly jobless claims data after the close (and analyst estimates of national-level claims). Friday's calendar is largely Fed-speak related (Schmid, Logan, and Bostic make appearances) with PPI and Retail Sales almost certain to be postponed.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Boston's Collins Still Sees "A Bit" More Easing This Year

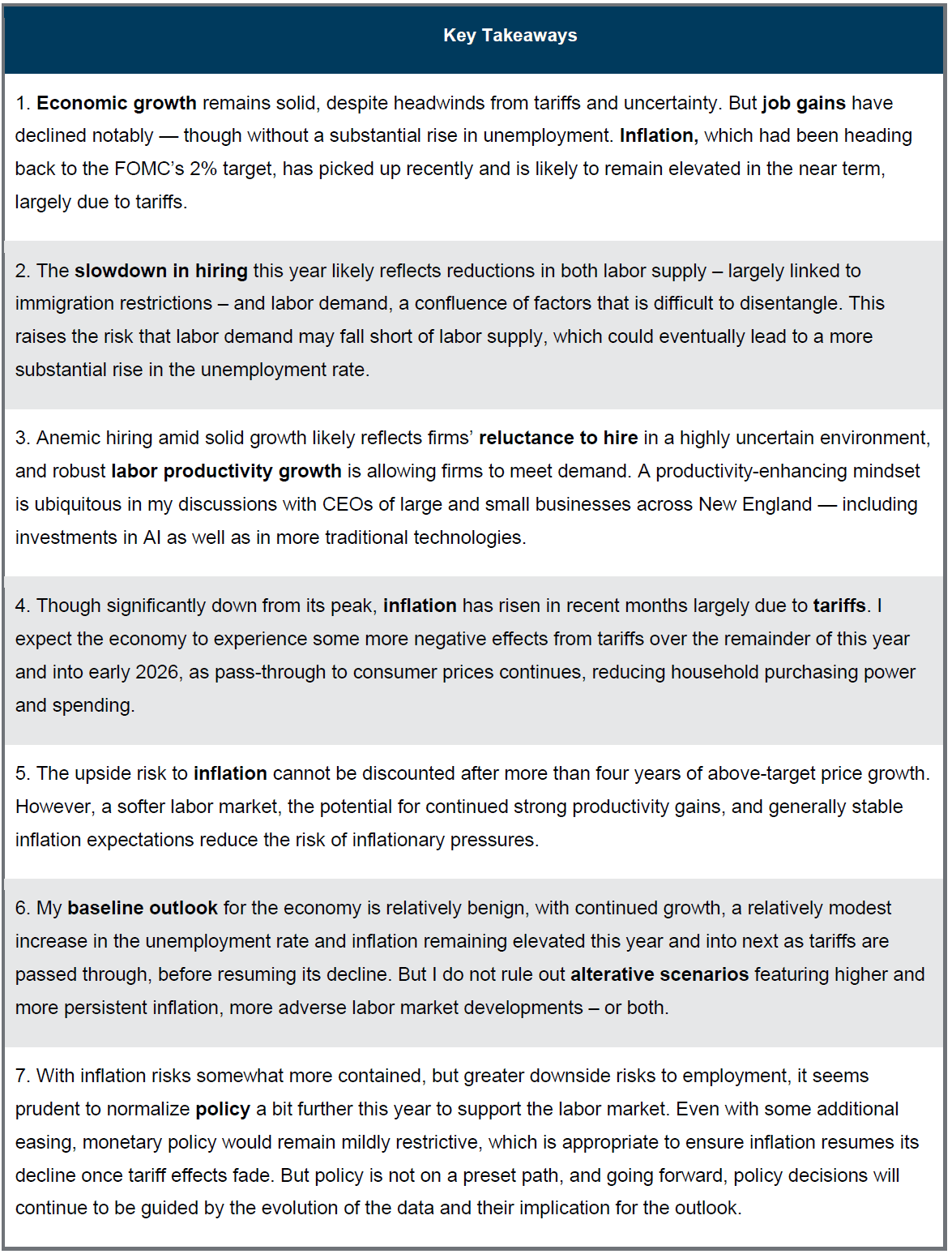

The key takeaways from Boston Fed President Collins's (2025 FOMC voter) speech on "Assessing The Balance Of Risks In The Economy" Tuesday (link) are in the image below, very similar to her speech on September 29 but with greater depth to her arguments.

- We still peg Collins as a "one more cut" submission in the September SEP, though there is an argument she is one of the median 9 (of 19 members) who sees 2 more cuts. In particular, she again notes scope for normalizing policy "a bit further" this year; having previously described the September 25bp cut as "a bit of easing", it would stand to reason she is referring to 25bp moves in both instances. Additionally she says she could envisage a scenario where no further cuts this year are warranted.

- The key passage on monetary policy: "with inflation risks somewhat more contained, but greater downside risks to employment, it seems prudent to normalize policy a bit further this year to support the labor market. Importantly, even with some additional easing, monetary policy would remain mildly restrictive, which is appropriate for ensuring that inflation resumes its decline once tariff effects filter through the economy. But policy is not on a pre-set path, and I can envision scenarios where appropriate policy calls for holding rates steady later this year and into next, as we assess effects of the recent policy actions and get more information. Going forward, my policy decisions will continue to be guided by my best assessment of all available data, their implications for the outlook, and the evolving risks."

- Similar to her previous appearance, Collins says Tuesday "While I see inflation risks as somewhat more contained than I previously thought, downside risks to the labor market have likely risen."

- She again highlights the slower growth in both labor supply and demand, pointing to a 40k "breakeven" rate of payrolls growth. She says however that the "broad-based slowdown in hiring raises the risk that labor demand may fall short of supply, which could eventually lead to a more substantial increase in the unemployment rate than we have seen so far this year."

- She notes "a few reasons to expect further price pressures from tariffs going forward", while "Overall, my baseline economic outlook is relatively benign. I see continued growth in activity, little further rise in the unemployment rate, and inflation remaining elevated this year and into early 2026 as tariffs are passed through more fully, before resuming its decline".

- "while that is my baseline view, I do not rule out scenarios featuring higher and more persistent inflation, more adverse labor market developments, or both."

- She sees inflation expectations as "relatively stable". And "a softer labor market with strong productivity growth reduces the risk of inflationary pressures from wage growth." "But all of this warrants careful attention, and a lack of comprehensive price data (given the government shutdown) will complicate assessing the inflation environment."

USDCAD TECHS: Bullish Trend Structure

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4167 50.0% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.4111 High Apr 10

- RES 1: 1.4080 Intraday high

- PRICE: 1.4042 @ 17:20 BST Oct 14

- SUP 1: 1.3928/3863 20- and 50-day EMA values

- SUP 2: 1.3799 Bull channel base drawn from the Jul 23 low

- SUP 3: 1.3727 Low Aug 29 and a bear trigger

- SUP 4: 1.3689 Low Jul 28

A bull cycle in USDCAD remains intact and this week’s firm start reinforces current conditions. Last Thursday’s rally confirmed a recent bull flag on the daily chart and a resumption of the current uptrend. MA studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4111 next, the Apr 10 high, and further out scope is seen for an extension towards 1.4167, a Fibonacci retracement. First key support is 1.3863, 50-day EMA.

CROSS ASSET: Equities Bear Brunt Of Trump Re-Escalation Of Trade Rhetoric

While President Trump's Truth Social comments re China focus primarily on cooking oil as an area of retaliatory trade action for China "purposefully not buying our Soybeans...an Economically Hostile Act", the re-ratcheting up of hostile rhetoric as well as threatening "other elements of Trade, as retribution" has had a risk-off impact on markets largely focused on equities.

- S&P emini futures drop 0.6% on the headline, erasing the afternoon's gains to now sit about 0.3% lower on the day at 6,685. TY futures tick up to afternoon highs at 113-15+, still below session highs of 113-17+. Dollar ticks a little higher but not much in the move.

- While this will likely be digested as a negotiating tactic ahead of US-China talks later this month, it's clear there remains heightened sensitivity to escalations in rhetoric in these matters.