FOREX: USD Slide Continues, Further De-linking FX with Rates & Equities

- As the US government reopened, the USD fell against broader G10, prompting a new November low for the USD Index. In further evidence that the currency and rates markets are diverging, the USD found very little solace in either the strength and show above 4.11% in the US 10y yield, or the persistent trimming of Fed rate cut pricing for the December FOMC, which now stands at less than 50%.

- The USD is slipping as markets seem to be adopting a pro-growth phase after the end of the government shutdown, which was estimated to be costing as much as $15bln per day - however the test for the USD's ability to sustain itself at lower levels will be tested by the incoming data. This covers not only the official agency releases, but the private sector data also, including next week's ADP weekly jobless estimate.

- That said, a negative session for equities paints a less positive picture. Underperformance in megacap tech names (NVIDIA dropped near 3.5%) undermined headline index performance, which dragged AUD, NZD and other growth proxy currencies off highs, while favouring haven FX including JPY and CHF.

- Meanwhile, Gold saw renewed gains early Thursday, putting prices at the highest since the October 21 pullback. While prices have faded, a positive close today would be the 7th consecutive higher daily close. Only partial pricing for a Dec Fed cut opens up potential for a dovish turn in rates should incoming data surprise to the downside, which should prove positive for gold prices.

- Focus Friday shifts to the potential publication of advisories and schedules for the still-missing US economic releases. With the government still in the process of reopening, we expect September NFP to be released imminently, and in it's full format, however the October release that follows may be lacking key data on the unemployment rate - a message affirmed by White House Advisor Kevin Hassett today.

- Chinese retail sales and industrial production data are due Friday, with speeches also due from ECB's Escriva, Vujcic, Elderson & Lane, while Fed's Schmid, Logan & Bostic (who announced his retirement this week) round things off in the US.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

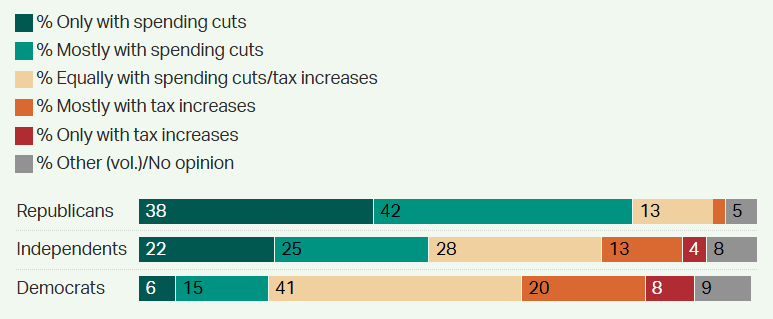

US: Partisan Fiscal Preferences In Elecorate Could Prolong Govt Shutdown

A new survey from Gallup has found, “Partisans’ preferences for reducing the federal budget deficit have differed sharply in the past and continue to today. Democrats have historically been most likely to prefer equal spending cuts and tax increases, and a 41% plurality of Democrats now favor that approach...

- “Conversely, the broad majority of Republicans continue to favor spending cuts, either exclusively (38%) or mostly (42%). Independents’ preferences are currently roughly in line with the national average, as they have been in prior readings.”

- Gallup concludes, “Americans’ desire to rein in government spending, paired with their reluctance to reduce major entitlement programs or raise broad-based taxes, mirrors the same clash of views preventing lawmakers from reaching a budget agreement.

- “Republicans are focused on spending cuts, and Democrats lean toward a combination of spending cuts and tax increases. The fiscal gridlock now driving the government shutdown reflects not only partisan differences in Congress but also a divided public that offers little clear guidance for bipartisan compromise, something that Americans want.”

Figure 1: Partisans' Preference for Reducing Federal Budget Deficit

Source: Gallup

FED: Powell Eyeing Incoming Inflation Data, "Alternative" Jobs Numbers (2/2)

Powell in Q&A discusses what data the FOMC is looking at amid the federal gov't shutdown, pointing out that you can for example "add up" state jobless claims reports "and get a pretty decent estimate", and ADP payrolls.

- "I will say generally the alternative data that we look at is better used as a supplement for the underlying governmental data, which is the gold standard. And it won't be as effective as the main course as it would have been as a supplement.... in the employment space, there's some pretty good substitutes, less so in the inflation space and and in the economic activity space."

- On missing federal government data, Powell suggests that "we're going to make our decisions according to the FOMC schedule, but I think it will be a lot better once we start getting, for example, the September employment report is going to be very important report, and we're not on track to have that, there would still be time for us to get that. We will get, of course, the September inflation, the CPI and PPI reports. So that's a positive. But, you know, we don't comment on fiscal matters, but from our standpoint, we'll start to miss that data, and particularly the October data. If this goes on for a while, they won't be collecting it, and it could become

more challenging" - Further to his speech commentary on the balance sheet, Powell says on what they're watching for when considering ending QT: "So we have a we have a nice spider chart and five main indicators, one of which is repo levels. And I think overall what they're showing is that we're still at ... abundant reserves... a little bit above ample reserves. So but we're beginning to see ... a little bit of tightening in money market conditions, particularly repo rates have moved up.... the pace of runoff is now very, very slow. So we're going to be watching all those factors very carefully. And we're not so far away now. But there's a ways to go."

- Asked if the Fed would look at any specific action on MBS to address mortgage rates or housing affordability, Powell says the Fed doesn't target housing prices.

BONDS: EGBs-GILTS CASH CLOSE: Gilts And OATs Outperform On Local Developments

Gilts and OATs were standout performers in an eventful session Tuesday.

- Core FI saw an early bid amid renewed deterioration in Sino-U.S. trade relations.

- The tone was helped with data coming in on the soft side early too: the UK labour market report included disappointments on the wage growth, vacancies and LFS fronts (MNI's review of the data here), spurring a deepening of BOE cut pricing. Meanwhile, the German ZEW survey readings underperformed across both expectations and current conditions.

- In the session's key development, OAT spreads to Bund tightened sharply on prospects for early elections to be avoided, after French PM Lecornu pledged among other matters to suspend the 2023 pension reforms to 2028. OAT gains extended into the cash close with 10Y yields hitting 2 month lows as the Socialists said they will not vote for a no confidence motion in the government.

- On the day, Gilts outperformed Bunds with both the German and UK curves closing bull flatter.

- OATs outperformed in the periphery/semi-core space, with 10Y spreads to Bund falling below 80bp.

- After the cash close we await commentary from various French political leaders who are expected to weigh in on the Lecornu speech.

- Wednesday's calendar includes Eurozone industrial data, with multiple ECB and BOE speakers including Ramsden, Breeden, and Villeroy.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.9bps at 1.935%, 5-Yr is down 1.5bps at 2.202%, 10-Yr is down 2.6bps at 2.61%, and 30-Yr is down 3.2bps at 3.192%.

- UK: The 2-Yr yield is down 4.9bps at 3.901%, 5-Yr is down 6.3bps at 4.038%, 10-Yr is down 6.8bps at 4.59%, and 30-Yr is down 6.9bps at 5.394%.

- Italian BTP spread down 1.5bps at 78.3bps / French OAT down 4bps at 79.8bps