SNB: Tschudin Sees SNB Monetary Policy Having Desired Effects On Funding Markets

SNB governing board member Petra Tschudin strikes a content tone at the SNB's money market event in Geneva in her speech about "Bank funding costs: latest developments from a monetary policy perspective". She concludes that the SNB's monetary policy continues to have the desired effects on funding markets. Key excerpts and charts below:

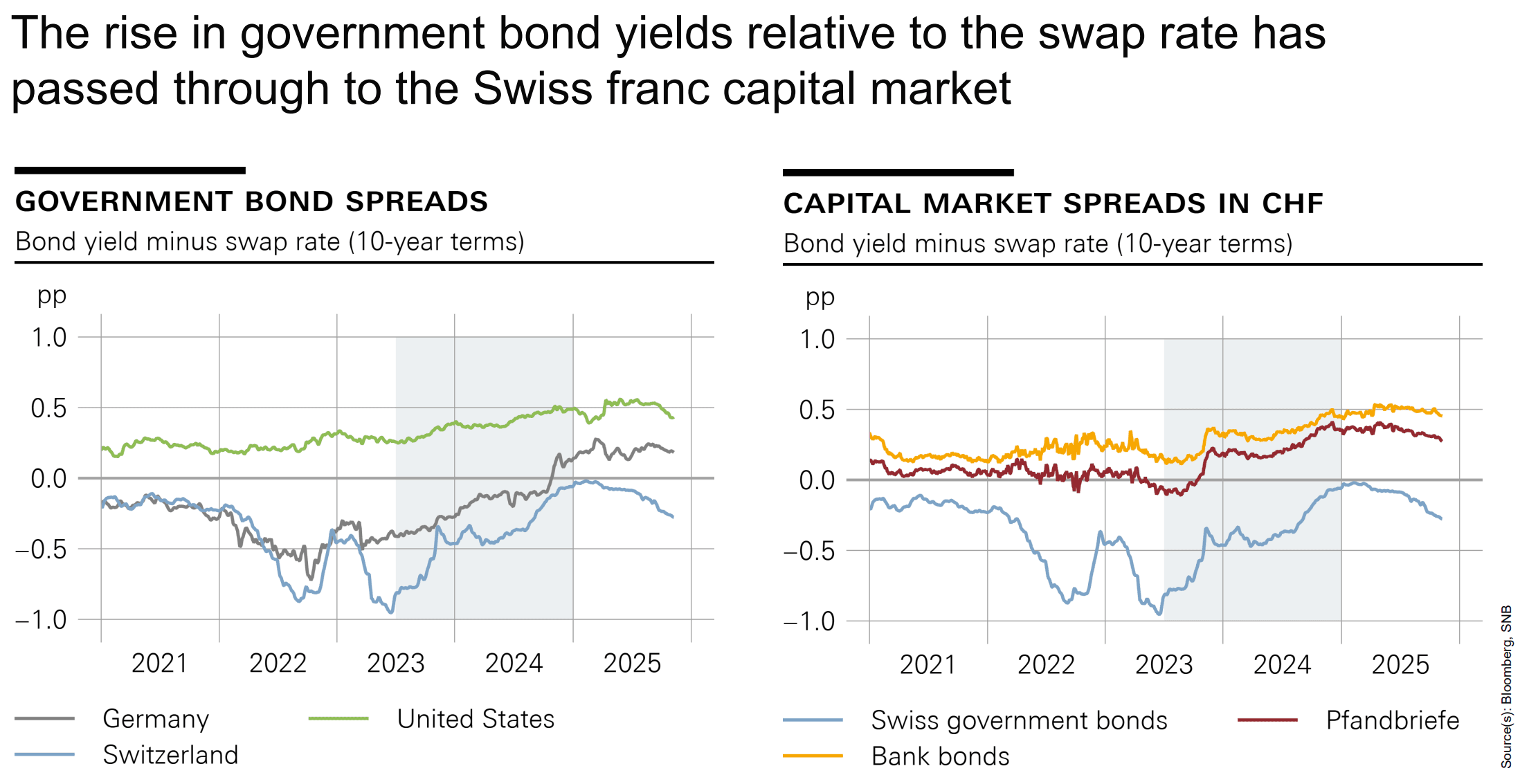

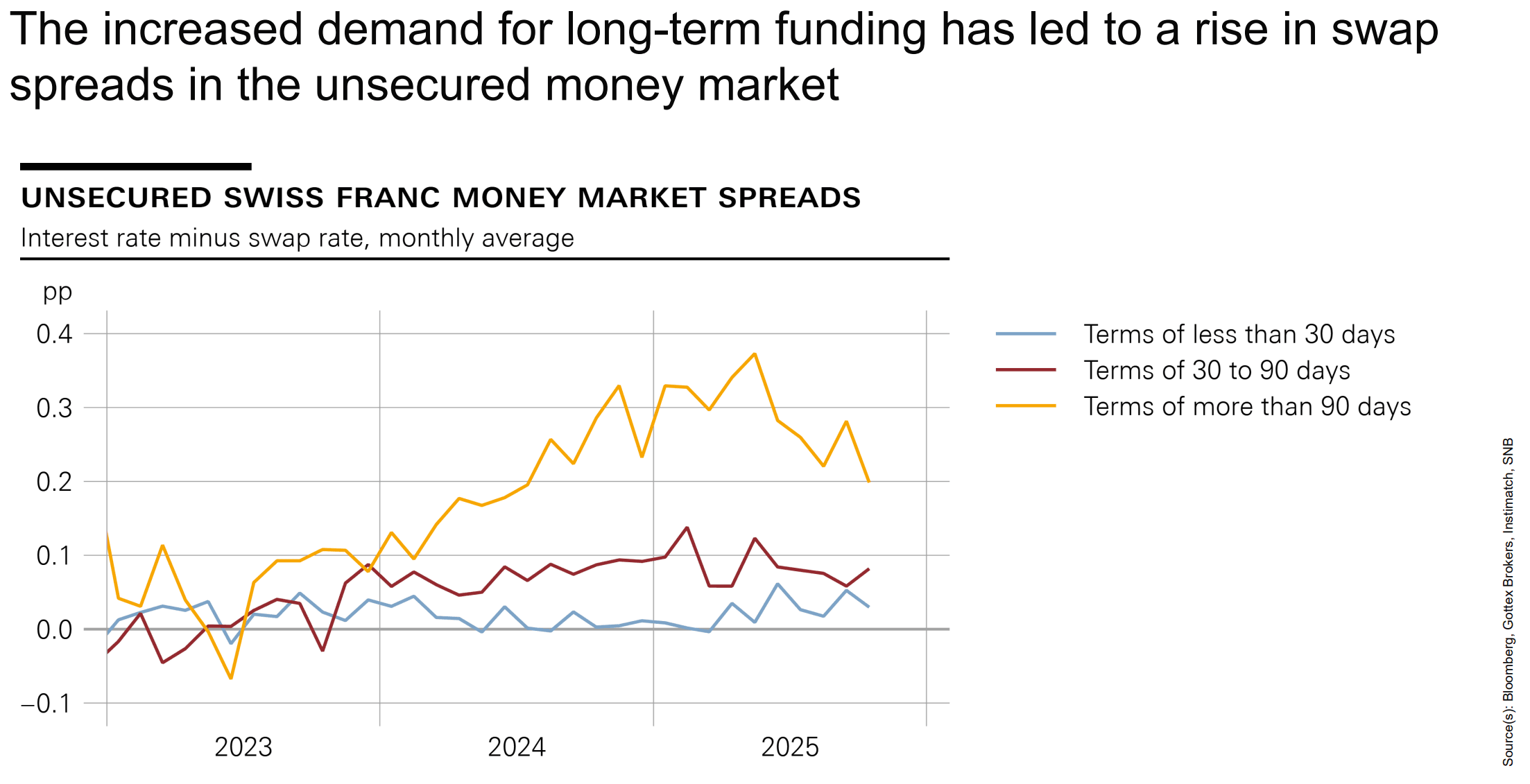

- "We observe that the interest rates at which banks secure funding in the financial market have fallen less sharply than the general level of interest rates. This means that bank funding costs in the financial market have increased relatively speaking, which can affect the pricing and granting of loans."

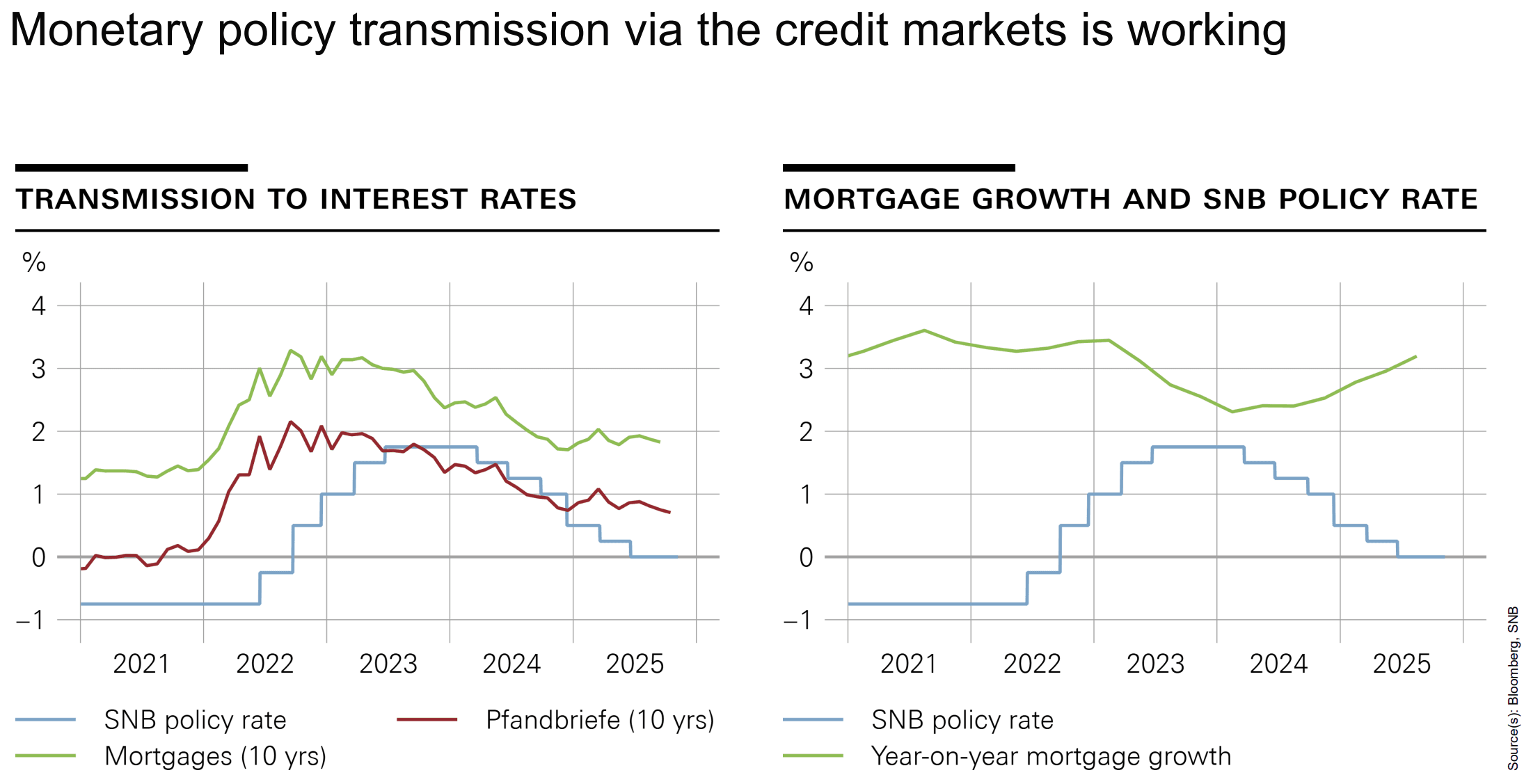

- However, "credit growth in Switzerland has remained robust overall. The volume of mortgage lending, which makes up over 85% of total credit volume, is currently growing at a rate of around 3%. This development is in line with our model forecasts."

- "Following our policy rate cuts, both funding and lending rates fell markedly, despite rising relative to swap rates. This shows that monetary policy transmission via the credit markets is working. Credit growth has accelerated as a result. Our monetary policy easing is thus having the intended effect."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Bear Threat Remains Present

- RES 4: 1.3789 High Jul 1 and key resistance

- RES 3: 1.3726 High Sep 17

- RES 2: 1.3661 High Sep 18

- RES 1: 1.3433/3527 20-day EMA / High Oct 1 and a pivot level

- PRICE: 1.3313 @ 17:06 BST Oct 14

- SUP 1: 1.3262 Low Oct 10

- SUP 2: 1.3254 Low Aug 4

- SUP 3: 1.3142 Low Aug 1 and a key support

- SUP 4: 1.3041 Low Apr 14

A short-term bear condition in GBPUSD remains intact and price continues to trade closer to last week’s low print - even with the late Tuesday rally. The pair has breached a key short-term support at 1.3333, the Sep 3 low. The break signals scope for a deeper retracement. A clear break of 1.3280 (pierced), a Fibonacci retracement, would open key support at 1.3142, the Aug 1 low. Initial resistance to watch is unchanged at 1.3433, the 20-day EMA.

FED: Powell Keeps October Cut On Track, Notes Jobs Vs Activity Divergence (1/2)

In what is among the very last major FOMC communications before the pre-meeting blackout period begins Friday night, Chair Powell's commentary Tuesday largely maintains the status quo in terms of signalling another 25bp rate cut at the end of October.

- In his written remarks, he says "based on the data that we do have, it is fair to say that the outlook for employment and inflation does not appear to have changed much since our September meeting four weeks ago" when of course they cut rates 25bp eyeing "Rising downside risks to employment". Though in a slightly less dovish note, "data available prior to the shutdown, however, show that growth in economic activity may be on a somewhat firmer trajectory than expected."

- In Q&A, Powell repeats his September commentary that "there really isn't a risk free path" with some danger of inflation persistence but "the labor market has demonstrated pretty significant downside risks as payroll jobs have declined in both the supply and demand for for labor has declined quite sharply".

- On the risks of easing: "if we move too quickly, then we may leave the inflation job unfinished and have to come back later and finish it. And if we move too slowly, there may be unnecessary, painful losses in the employment market."

- He echoes other speakers including Gov Waller last week in saying that the activity and labor market data aren't necessarily telling the same story, and future policy could depend on how that discrepancy plays out: "Even even subsequent to the September SEP, we've seen economic activity data which are surprising to the upside... you do have a bit of a tension there between the labor market data that we see very low levels of job creation. And yet people are spending. So economic activity is strong. And... we're going to have to see how that plays out.... if economic activity were stronger, then that would tend to support labor market activities in hiring. And so we'll have to see how that works out."

- Commenting on nonfarm payroll "breakeven" growth, Powell notes that a figure "I'm not going to try to give you a pinpoint number, but... the standard error around these things is, you know, 50,000 plus or minus, something like that... I think the range of plausible numbers... probably does go below zero... it's clearly come down a great deal."

- He points to the Beveridge Curve to suggest that "further declines in job openings might very well start to show up in unemployment."

US: FED Reverse Repo Operation

RRP usage resumes, usage slips to new low of $3.516B (lowest level since early April 2021) with 7 counterparties from $4,124B last Friday. Compares to this year's high usage of $460.731B on June 30.