MNI ASIA OPEN: Payrolls Rise, Stocks at Four Week Highs

EXECUTIVE SUMMARY

- MNI TARIFFS: China Considering Fentanyl Deal To Kickstart Trade Talks With US - WSJ

- MNI US: Trump's FY2026 Budget Draws Pushback From GOP Defence Hawks

- MNI US-JAPAN: Ishiba Will 'Not Accept' Auto Tariffs, But Won't 'Rush To Conclusion'

- MNI US DATA: Hours Worked Paint A Less Negative Picture

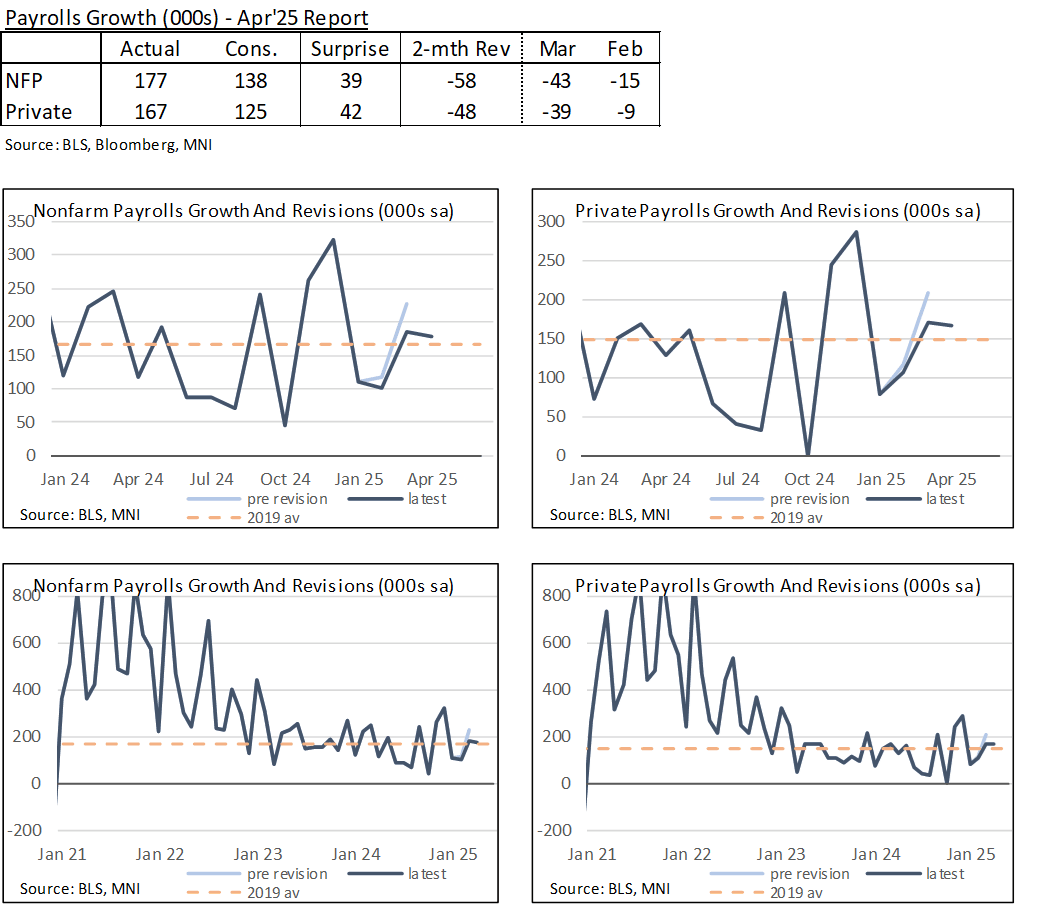

- MNI US DATA: Beat For Payrolls Countered By Two-Month Revisions

US

MNI US: Trump Policy Advisor Miller Top Candidate For Nat Sec Advisor - Axios

Axios reporting that US President Donald Trump's top policy advisor, Stephen Miller, is "garnering buzz" as the top candidate to replace ousted Mike Waltz as National Security Advisor. Secretary of State Marco Rubio is currently serving in the role temporarily.

- Axios: "Miller already is the administration's Homeland Security adviser, and is an aggressive defender of the administration's legal push for immediate deportations of unauthorized immigrants without court hearings. One White House source told Axios via text that Miller has made the Homeland Security Council run "like clockwork," and that it's "infinitely more effective than the NSC [National Security Council] with a tiny fraction" of the staff."

MNI US: Trump's FY2026 Budget Draws Pushback From GOP Defence Hawks

Reuters carrying comments from senior White House Office of Management and Budget officials on President Donald Trump’s ‘skinny’ budget resolution for Fiscal Year 2026 that was released today. The officials note the budget's focus on spending reductions: “White House proposes FY2026 $1.7 trillion budget, down 7.6% from previous year." The officials add that the “proposed FY2026 budget includes lowest non-defense spending since 2000.”

NEWS

MNI TARIFFS: CEA's Miran-Surprised If Tariffs Don't Change; Will Be Deal w/China

Speaking to Bloomberg TV, Chair of the White House Council of Economic Advisers Stephen Miran says that he would be "surprised if tariffs don't change in a few weeks". He adds that [President Donald] "Trump has been clear, there will be a deal with China". The comments chime with those from an earlier interview given to MNI by Miran, published on 1 May.

MNI TARIFFS: China Considering Fentanyl Deal To Kickstart Trade Talks With US - WSJ

The Wall Street Journal reports that "Beijing is considering ways to address the Trump administration’s gripes over China’s role in the fentanyl trade... potentially offering an off-ramp from hostilities to allow for trade talks to start." The Journal notes that "discussions remain fluid" and China "would like to see some softening of stance from President Trump". According to the report, "Chinese leader Xi Jinping’s security czar, Wang Xiaohong, in recent days has been inquiring about what the Trump team wants China to do when it comes to the [precursor] chemical ingredients used to make fentanyl..."

MNI US-JAPAN: Ishiba Will 'Not Accept' Auto Tariffs, But Won't 'Rush To Conclusion'

Speaking to FNN, Japanese PM Shigeru Ishiba says "We absolutely will not accept tariffs like those on automobiles. Reducing the trade deficit is something that should be done. We will do what we can to reduce it, but we must not do so at the expense of Japanese jobs." Adds that he would "absolutely not" impose additional tariffs on automobiles, and his gov't does not want to do anything that could "undermine the national interest" by rushing negotiations with the US.

US TSYS

MNI US TSYS: Rates Retreat, Sentiment Improved Though Trade Risk Remains

- Treasuries look to finish near late Friday session lows after trading firmer on the open, higher than expected Nonfarm payrolls at 177k (sa, cons 138k) of which private contributed 167k (sa, cons 125k) triggered the early reversal.

- However, two-month revisions of -58k offset the 39k beat for nonfarm payrolls, with a similar story for private (a 42k surprise vs -48k two-month revision).

- Stocks are back near four week highs - pre-"Liberation Day" levels as hopes of some trade deal being made improved sentiment.

- The Wall Street Journal reports that "Beijing is considering ways to address the Trump administration’s gripes over China’s role in the fentanyl trade... potentially offering an off-ramp from hostilities to allow for trade talks to start." The Journal notes that "discussions remain fluid" and China "would like to see some softening of stance from President Trump".

- Currently, the Jun'25 10Y contract trades -20 at 111-07.5 vs 111-02 low -- initial technical support (50-dma) followed by 110-16.5/109-08 (Low Apr 22 / 11 and the bear trigger). Curves bear flattened, 2s10s -3.480 at 48.002, 5s30s -4.911 at 86.807.

OVERNIGHT DATA

MNI US DATA: Beat For Payrolls Countered By Two-Month Revisions

- Nonfarm payrolls were higher than expected at 177k (sa, cons 138k) of which private contributed 167k (sa, cons 125k).

- However, two-month revisions of -58k offset the 39k beat for nonfarm payrolls, with a similar story for private (a 42k surprise vs -48k two-month revision).

- Downward revisions were concentrated in March.

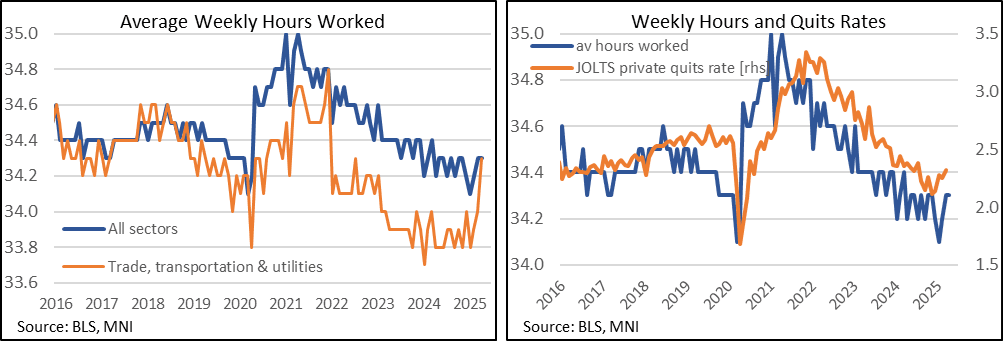

MNI US DATA: Hours Worked Paint A Less Negative Picture

- One thing that is worth emphasizing in the April payrolls report is the beat for average weekly hours worked, to 34.3 (cons 34.2) from an upward revised 34.3 in March (initial 34.2) for a second monthly upward revision.

- It has left a reversal from 34.1 in Jan (joint lowest with Mar 2020 otherwise lows since 2010 in GFC recovery) on particularly adverse weather before 34.2 in Feb and then two months at 34.3.

- These are still low historically (pre-pandemic range primarily 34.4-34.5 but with a few 34.3 and 34.6 readings) but it tentatively sees a second month without signs of companies further tamping down on costs via hours offered.

- One sector particularly of note here is the broad “trade, transportation and utilities” category which has seen a 0.5hr increase to 34.3hrs since January, 0.3 of which came in April. There have been large increases for most of the categories within it such as wholesale trade, retail trade and transportation & warehousing.

- As noted earlier, transportation & warehousing saw a strong uptick in payrolls growth in April. The combination suggests little sign of immediate adverse impacts from tariffs, with likely the opposite as tariff front-running has seen surge in imports and inventories. It's an area that will we watched closely ahead.

- Back to hours worked more broadly, the move off recent, likely weather-induced, lows for hours worked also follows a bottoming in quits rates in Nov-Dec 2024.

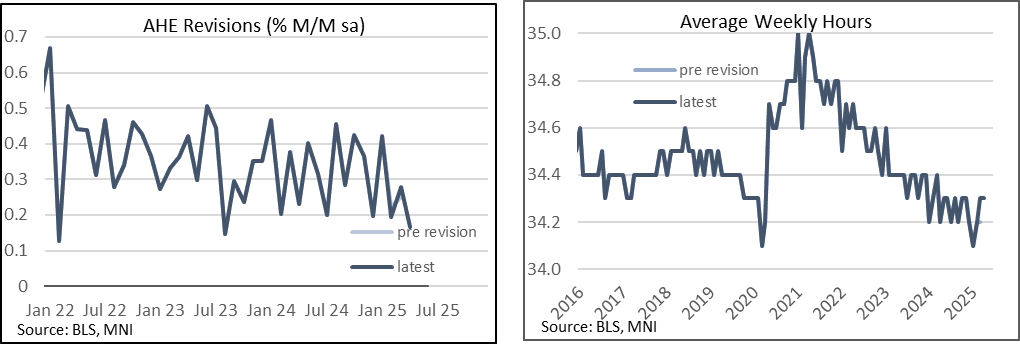

MNI US DATA: AHE Misses But Surprise Rise In Hours Worked More Than Compensate

- AHE sees a 'low' 0.2% M/M to add to the miss to consensus of 0.3% M/M, but the non-supervisory measure firmed after a weaker March. Further, the weakness in overall AHE should be more than offset by surprisingly firm weekly hours worked, beating expectations along with a second monthly upward revision. Unrounded AHE figures:

Total AHE:

- M/M (SA): 0.167% in Apr from 0.279% in Mar (initial 0.251%) and 0.195% in Feb (initial 0.223%)

- Y/Y (SA): 3.77% in Apr from 3.836% in Mar

AHE Non-Supervisory:

- M/M (SA): 0.323% in Apr from 0.162% in Mar (initial 0.162%) and 0.357% in Feb (initial 0.357%)

- Y/Y (SA): 4.054% in Apr from 3.893% in Mar

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 604.14 points (1.48%) at 41358.39

S&P E-Mini Future up 94.5 points (1.68%) at 5717.75

Nasdaq up 284.6 points (1.6%) at 17995.42

US 10-Yr yield is up 9.5 bps at 4.3122%

US Jun 10-Yr futures are down 20/32 at 111-7.5

EURUSD up 0.0016 (0.14%) at 1.1306

USDJPY down 0.42 (-0.29%) at 144.97

WTI Crude Oil (front-month) down $1.01 (-1.7%) at $58.20

Gold is down $11.12 (-0.34%) at $3228.19

European bourses closing levels:

EuroStoxx 50 up 124.97 points (2.42%) at 5285.19

FTSE 100 up 99.55 points (1.17%) at 8596.35

German DAX up 589.67 points (2.62%) at 23086.65

French CAC 40 up 176.61 points (2.33%) at 7770.48

US TREASURY FUTURES CLOSE

3M10Y +8.064, -0.53 (L: -13.11 / H: 0.964)

2Y10Y -3.48, 48.002 (L: 45.801 / H: 53.051)

2Y30Y -6.233, 95.775 (L: 94.45 / H: 103.748)

5Y30Y -4.911, 86.807 (L: 85.34 / H: 92.527)

Current futures levels:

Jun 2-Yr futures down 8.25/32 at 103-20.875 (L: 103-20 / H: 103-29.75)

Jun 5-Yr futures down 16.25/32 at 108-13 (L: 108-09.75 / H: 109-00.25)

Jun 10-Yr futures down 20/32 at 111-7.5 (L: 111-02 / H: 112-01.5)

Jun 30-Yr futures down 28/32 at 115-0 (L: 114-24 / H: 116-14)

Jun Ultra futures down 1-01/32 at 119-0 (L: 118-24 / H: 120-27)

MNI US 10YR FUTURE TECHS: (M5) Sold Hard Off Highs

- RES 4: 113-22 1.382 proj of the Apr 11 - 16 - 22 price swing

- RES 3: 113-04 76.4% retracement of the Apr 7 - 11 bear leg

- RES 2: 112-20+ Intraday high

- RES 1: 112-17+ 1.0% 10-dma envelope

- PRICE: 111-07+ @ 1515 BST May 2

- SUP 1: 111-02 50-dma

- SUP 2: 110-16+/109-08 Low Apr 22 / 11 and the bear trigger

- SUP 3: 108-26+ 76.4% retracement of the Jan 13 - Apr 7 bull cycle

- SUP 4: 108-21 Low Feb 19

Treasury futures took another leg lower Friday on the back of a firmer NFP print. This sees prices comfortably through the first real support at the 20-day EMA, below which 110-16+ marks the Apr 22 low and next notable downside level. Recent gains resulted in a break of 111-25, 50.0% of the Apr 7 - 11 bear leg. However, the lack of follow through here shows the bullish S/T trend signal may be under threat. The bear trigger remains 109-08, the Apr 11 low.

SOFR FUTURES CLOSE

Jun 25 -0.075 at 95.810

Sep 25 -0.120 at 96.160

Dec 25 -0.135 at 96.450

Mar 26 -0.160 at 96.635

Red Pack (Jun 26-Mar 27) -0.16 to -0.135

Green Pack (Jun 27-Mar 28) -0.125 to -0.105

Blue Pack (Jun 28-Mar 29) -0.10 to -0.075

Gold Pack (Jun 29-Mar 30) -0.07 to -0.05

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (-0.02), volume: $2.789T

- Broad General Collateral Rate (BGCR): 4.35% (-0.02), volume: $1.084T

- Tri-Party General Collateral Rate (TCR): 4.35% (-0.02), volume: $1.044T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $107B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $247B

FED Reverse Repo Operation

RRP usage slips to $147.882B this afternoon from $157.353B yesterday. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B. The number of counterparties at 35.

PIPELINE - No new corporate bond issuance Friday after May kicked off with $9.75B Thursday

MNI BONDS: EGBs-GILTS CASH CLOSE: Week Ends With Risk-On Yield Rise

Bund and Gilt yields rose to finish the week, with periphery/semi-core EGB spreads tightening in a largely risk-on session.

- EGBs opened weaker, catching up in the return to cash trade from Thursday's holiday. Gilts were on the front foot early however, with no particular catalyst (there was some political intrigue with the Reform UK party's strong local and byelection performance but this wasn't seen as a market-mover).

- Bunds saw relatively muted reaction to stronger-than-expected Eurozone flash April core HICP print and upward revisions to April manufacturing PMIs.

- The main driver in the session was the US April Employment Report which was more solid than had been anticipated, driving Treasury yields higher and dragging Bunds and Gilts in the same direction. With a risk-on tone pervading as equities gained, core yields closed on the highs.

- The German curve bear steepened, with the UK's leaning bear flatter through the 10Y segment. For the week, both curves steepened: Germany's bear steeper (2s +4.3bp, 10s +6.4bp), with the UK's twist steepening (2Y -0.2bp, 10Y +6.4bp).

- Periphery/semi-core EGB spreads fell, reflecting the risk-on backdrop.

- Recal that Monday is a UK market holiday. Next week sees the BOE decision (a 25bp cut is fully priced)

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 7.6bps at 1.762%, 5-Yr is up 9.5bps at 2.08%, 10-Yr is up 8.9bps at 2.533%, and 30-Yr is up 8.9bps at 2.971%.

- UK: The 2-Yr yield is up 3.5bps at 3.856%, 5-Yr is up 3.4bps at 3.977%, 10-Yr is up 2.7bps at 4.508%, and 30-Yr is up 4.3bps at 5.303%.

- Italian BTP spread down 1.7bps at 110.3bps / French OAT down 1.5bps at 71.4bps

MNI FOREX: AUDUSD Rises Above 0.6450 Amid Surging Equities/Softer Greenback

- Prior to the US employment report, the greenback traded weaker against all others, with the USD Index reversing off yesterday's recovery high at 100.375. Trade negotiations remain a focus for markets - with deals between the US and Japan/India seen as particularly advanced. Furthermore, a greater sense of optimism regarding China/US discussions is reflected by the 0.8% for the Chinese Yuan.

- A higher-than-expected NFP print was offset by lower revisions which sparked some short-term volatility. USDJPY snapped higher to 145.00 before then steadily reversing south to print fresh session lows below the 144.00 mark. Equities like the print however, as the lack of major deterioration in the US labour market boosts global sentiment prompting USDJPY to rally the best part of 100 pips into the close to ~144.70.

- This sentiment has bolstered the likes of AUD, NZD and the Scandies which are the best performers in G10. For AUDUSD specifically, fresh yearly highs above 0.6450 have been printed as the pair currently stands 1% high on the session. The underlying trend remains bullish, and spot has recently breached a key resistance at 0.6409, the Dec 9 ‘24 high. The initial target of 0.6471 (Dec 9 high) has been met, which places the focus on 0.6528 (Nov 29 high) next.

- There has been less enthusiasm for the Euro, and despite a post data surge to 1.1380, we are back closer to the 1.1300 mark ahead of the close, down around half a percent on the week. An additional mention to USDCHF, which continues to respect the prior breakdown point of 0.8333 as pivot resistance ahead of Swiss CPI on Monday.

- The US ISM services PMI will also garner attention Monday, where UK and Japan are both out for national holidays.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/05/2025 | 0630/0830 | *** | CPI | |

| 05/05/2025 | 0700/0300 | * | Turkey CPI | |

| 05/05/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 05/05/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 05/05/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 05/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 05/05/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 06/05/2025 | 0130/1130 | * | Building Approvals | |

| 06/05/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 06/05/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI |