MNI ASIA OPEN: Little Change Latest Beige Book, Jobless Stable

EXECUTIVE SUMMARY

- MNI FED: Economic Activity Little Changed In Latest Beige Book

- MNI UK FISCAL: OBR Apologises; Chancellor Cutting Fiscal Rules Eval To Yearly

- MNI US: Democrats Could Win 'Redistricting War' If SCOTUS Declines To Restore TX Map

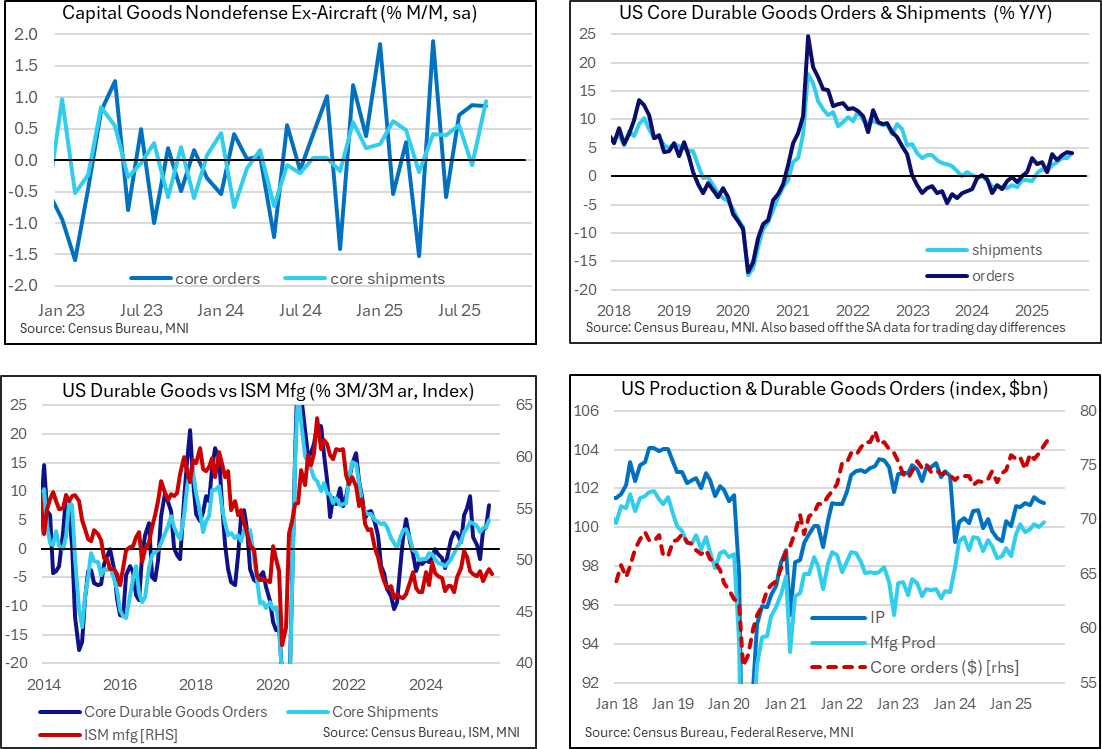

- MNI US DATA: Core Durables Goods Orders Chalk Up A Robust Q3

- MNI US DATA: Jobless Claims Data Don’t Suggest Any Further Rise In The U/E Rate

US

MNI FED: Economic Activity Little Changed In Latest Beige Book

The latest Fed Beige Book (link): "Economic activity was little changed since the previous report, according to most of the twelve Federal Reserve Districts, though two Districts noted a modest decline and one reported modest growth."

- Labor: “Employment declined slightly over the current period with around half of Districts noting weaker labor demand. Despite an uptick in layoff announcements, more Districts reported contacts limiting headcounts using hiring freezes, replacement-only hiring, and attrition than through layoffs.”

- That compares to “Employment was flat overall, as both hiring and layoffs increased modestly.”

- Inflation: “Prices rose moderately during the reporting period. Input cost pressures were widespread in manufacturing and retail, largely reflecting tariff-induced increases. Some Districts noted rising costs for insurance, utilities, technology, and health care. The extent of passthrough of higher input costs to customers varied, and depended upon demand, competitive pressures, price sensitivity of consumers, and pushback from clients. There were multiple reports of margin compression or firms facing financial strain stemming from tariffs. Prices declined for certain materials, which firms attributed to sluggish demand, deferred tariff implementation, or reduced tariff rates. Looking ahead, contacts largely anticipate upward cost pressures to persist but plans to raise prices in the near term were mixed.”

- That compares to "Prices rose moderately on average, as certain cost pressures increased. [...] Most contacts expected to face at least modest further cost pressures moving forward, and some were concerned about a possible acceleration of prices in 2026."

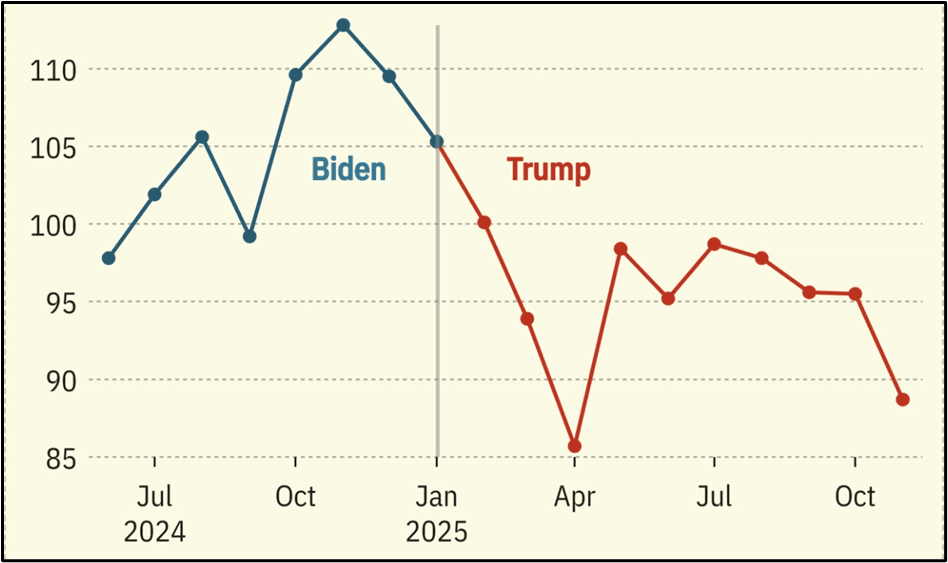

MNI US: Consumer Confidence Falls In November, Trump Problems w/Economy Mount

Semafor reports, “US consumer confidence declined more than expected in November, according to the Conference Board, while retail sales growth slowed in September.”

- The Conference Board said, "Declining confidence could pose political problems for Trump and Republicans in Congress, as the dimmer views of the economy were seen among all political affiliations and were particularly sharp among independents."Semafor notes that the data suggests the "economy is heading into the all-important holiday season buffeted by a cooling labor market, continued inflationary pressures and signs consumers were easing their pace of spending and searching for bargains,” The Wall Street Journal wrote. American consumers plan to spend less this Black Friday, according to a Deloitte survey. They’re likely to spend more on the usual Thanksgiving staples, according to The Associated Press, as tariffs hit canned goods.”

Figure 1: US Consumer Confidence Index - Source: Semafor, Conference Board

NEWS

MNI US: Democrats Could Win 'Redistricting War' If SCOTUS Declines To Restore TX Map

The Supreme Court is expected to announce a ruling any day now on a GOP-drafted congressional map that could net the party up to five new House seats in 2026. A SCOTUS decision to overturn a lower court block on the map is likely before the Dec. 8 filing deadline for candidates in Texas. Axios notes, “An anticipated ruling would mark the high court's first word on the redistricting wars that have defined the 2026 cycle. It wouldn't be the last: Lawsuits are anticipated from California to North Carolina...”

MNI UK FISCAL: OBR Apologises; Chancellor Cutting Fiscal Rules Eval To Yearly

OBR posts on its website: "A link to our Economic and fiscal outlook document went live on our website too early this morning. It has been removed. We apologise for this technical error and have initiated an investigation into how this happened. We will be reporting to our Oversight Board, the Treasury, and the Commons Treasury Committee on how this happened, and we will make sure this does not happen again. Our Economic and fiscal outlook and supporting documents will be released when the Chancellor has finished her speech."

Bloomberg: Pentagon Cited Alibaba on China Military Aid in Oct. 7 Letter - The Pentagon concluded that Alibaba Group Holding Ltd., Baidu Inc. and BYD Co. should be added to a list of companies that aid the Chinese military, according to a letter to Congress sent roughly three weeks before Donald Trump and Xi Jinping agreed to a broad trade truce.

US TSYS

MNI US TSYS: Well Off Early Lows Ahead Thanksgiving Holiday, Short Friday Month End

- Treasuries look to finish mixed - well off early session lows, curves flatter with the short end underperforming. Treasuries extend lows early Wednesday - earlier than expected UK OBR economic forecast got the ball rolling - growth forecasts cut.

- Second round of selling just prior to the Chicago PMI release, drawing mild buying after the lower than expected barometer decline of 7.5 points to 36.3 in November. The index is below 40 for the first time since January, and has remained below 50 for twenty-four consecutive months.

- Nascent month end selling and/or portfolio rebalance at play, stocks dipped as well before staging broad based rally into midday. Currently the TYH6 contract trades steady at 113-19 vs 113-08.5 low. Initial support below at 112-30, the 20-day EMA. Support at the 50-day EMA, lies at 112-25.

- Otherwise, a bullish theme in Treasuries remains intact and Tuesday’s gains reinforce current conditions. The recent breach of the 112-31 level, an area of congestion since Nov 5, marks an important short-term bullish development. This exposes 113-29+, the Oct 17 high and a key resistance.

- Latest weekly jobless claims data suggest lower layoffs than recent payrolls reference periods although re-hiring conditions remain subdued. It might see only limited improvement on net for the u/e rate since September’s surprise increase to 4.44%, a factor likely behind NY Fed Williams’ uncharacteristic steer to another “near term” cut last week.

- Core durable goods orders were stronger than expected in preliminary September data, rising 0.9% M/M (sa, cons 0.3) after an upward revised 0.9% M/M in Aug (0.4) – all in nominal terms.

- The latest Fed Beige Book (link): "Economic activity was little changed since the previous report, according to most of the twelve Federal Reserve Districts, though two Districts noted a modest decline and one reported modest growth."

OVERNIGHT DATA

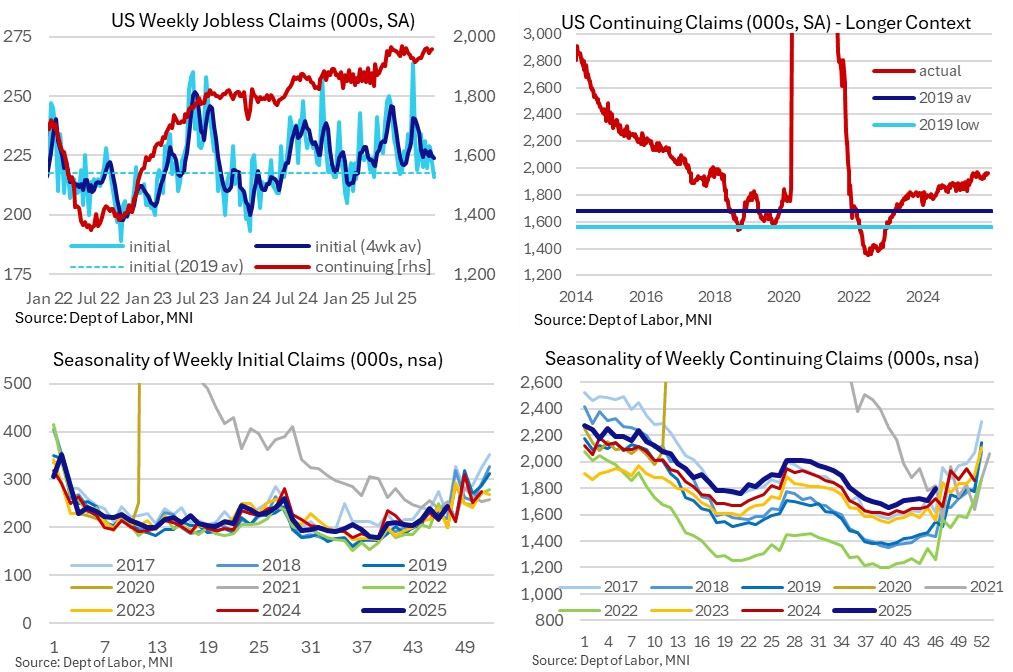

MNI US DATA: Jobless Claims Data Don’t Suggest Any Further Rise In The U/E Rate

Latest weekly jobless claims data suggest lower layoffs than recent payrolls reference periods although re-hiring conditions remain subdued. It might see only limited improvement on net for the u/e rate since September’s surprise increase to 4.44%, a factor likely behind NY Fed Williams’ uncharacteristic steer to another “near term” cut last week.

- Initial jobless claims were lower than expected at 216k (sa, cons 225k) in the week to Nov 22 after a downward revised 220k (initial 222k).

- Continuing claims meanwhile were roughly as expected at 1960k (sa, cons 1963k) in the week to Nov 15 after a downward revised 1953k (initial 1974k).

MNI US DATA: Chicago Business Barometer™ - Fell To 36.3 In November

The Chicago Business Barometer™, produced with MNI, fell 7.5 points to 36.3 in November. The index is below 40 for the first time since January, and has remained below 50 for twenty-four consecutive months. The decrease was driven by declines in Order Backlogs, New Orders, Production and Employment. An increase in Supplier Deliveries provided a small offset.

MNI US DATA: Core Durables Goods Orders Chalk Up A Robust Q3

Core durable goods orders continued a string of solid readings in recent months with the preliminary September readings, pointing to decent momentum for production into Q4. Core durable goods orders were stronger than expected in preliminary September data, rising 0.9% M/M (sa, cons 0.3) after an upward revised 0.9% M/M in Aug (0.4) – all in nominal terms.

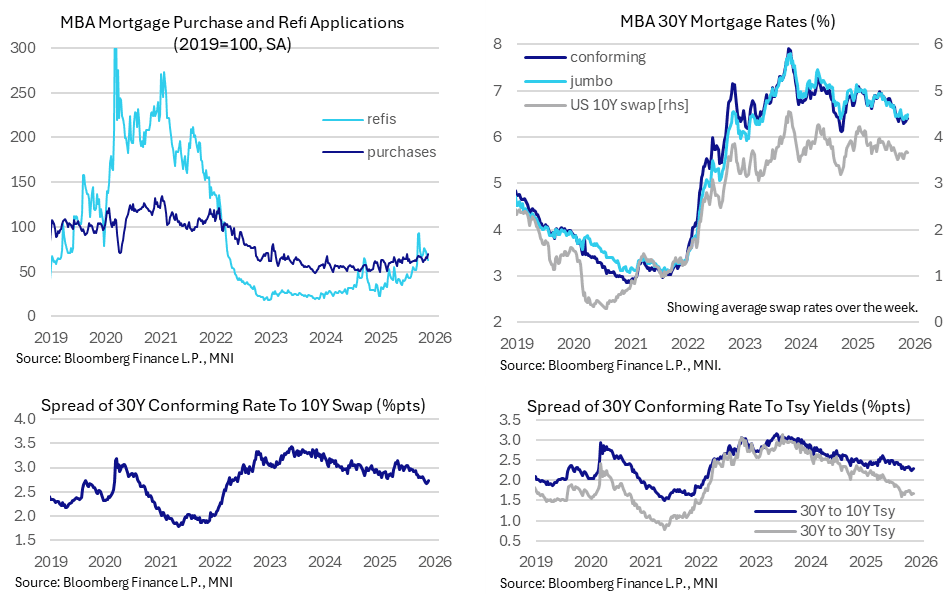

MNI US TSYS: New Purchase Mortgage Applications Highest In Nearly Three Years

- MBA composite applications inched 0.2% (sa) higher in the week to Nov 21 after a -5.2% drop the week prior.

- The details are more interesting, with new purchase applications rising 7.6% for its sharpest increase since early July to take the level of applications to their highest since Jan 2023.

- On the flipside, refi applications fell another -5.7% after -7.3% to more than reverse strength in the second half of October on lower mortgage rates, leaving them at their lowest since early September.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 314.67 points (0.67%) at 47427.12

S&P E-Mini Future up 50.5 points (0.74%) at 6831.75

Nasdaq up 189.1 points (0.8%) at 23214.69

US 10-Yr yield is down 0.6 bps at 3.9903%

US Dec 10-Yr futures are up 0.5/32 at 113-21

EURUSD up 0.0025 (0.22%) at 1.1595

USDJPY up 0.41 (0.26%) at 156.46

WTI Crude Oil (front-month) up $0.64 (1.1%) at $58.59

Gold is up $33.05 (0.8%) at $4163.65

European bourses closing levels:

EuroStoxx 50 up 81.67 points (1.47%) at 5655.58

FTSE 100 up 82.05 points (0.85%) at 9691.58

German DAX up 261.59 points (1.11%) at 23726.22

French CAC 40 up 70.63 points (0.88%) at 8096.43

US TREASURY FUTURES CLOSE

Curve update:

3M10Y -6.956, 14.186 (L: 13.995 / H: 20.874)

2Y10Y -2.212, 51.323 (L: 51.041 / H: 54.633)

2Y30Y -2.804, 116.047 (L: 115.599 / H: 120.173)

5Y30Y -1.519, 106.869 (L: 106.357 / H: 109.249)

Current futures levels:

Dec 2-Yr futures down 1.125/32 at 104-8.75 (L: 104-07.375 / H: 104-09.875)

Dec 5-Yr futures down 1.5/32 at 109-25.25 (L: 109-20 / H: 109-26.5)

Dec 10-Yr futures up 0.5/32 at 113-21 (L: 113-11 / H: 113-21.5)

Dec 30-Yr futures up 5/32 at 118-8 (L: 117-17 / H: 118-10)

Dec Ultra futures up 12/32 at 121-30 (L: 120-29 / H: 121-31)

MNI US 10YR FUTURE TECHS: (H6) Bull Cycle Exposes Key Resistance

- RES 4: 114-00 Round number resistance

- RES 3: 113-29+ High Oct 17 and a key resistance

- RES 2: 113-23 High Oct 23

- RES 1: 113-22+ High Nov 25

- PRICE: 113-17 @ 1340 ET Nov 26

- SUP 1: 113-08/112-30 Low Nov 25 / 20-day EMA

- SUP 2: 112-25 50-day EMA

- SUP 3: 112-10+ Low Nov 20

- SUP 4: 112-07 Low Nov 5 and a key support

A bullish theme in Treasuries remains intact and Tuesday’s gains reinforce current conditions. The recent breach of the 112-31 level, an area of congestion since Nov 5, marks an important short-term bullish development. This exposes 113-29+, the Oct 17 high and a key resistance. On the downside, initial support is at 112-30, the 20-day EMA. Support at the 50-day EMA, lies at 112-25.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 -0.003 at 96.263

Mar 26 -0.010 at 96.455

Jun 26 -0.015 at 96.715

Sep 26 -0.020 at 96.895

Red Pack (Dec 26-Sep 27) -0.025 to -0.02

Green Pack (Dec 27-Sep 28) -0.015 to -0.005

Blue Pack (Dec 28-Sep 29) -0.01 to -0.005

Gold Pack (Dec 29-Sep 30) -0.005 to steady

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.01% (+0.05), volume: $3.317T

- Broad General Collateral Rate (BGCR): 3.97% (+0.04), volume: $1.299T

- Tri-Party General Collateral Rate (TCR): 3.97% (+0.04), volume: $1.273T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.88% (+0.00), volume: $78B

- Daily Overnight Bank Funding Rate: 3.88% (+0.00), volume: $153B

FED Reverse Repo Operation

RRP usage at $2.217B with 6 counterparties this afternoon from $2.314B Tuesday. Compares to last Tuesday's $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

MNI Gilts Bull Flatten As Reeves Passes Short-Term Fiscal Hurdle

The rally stalls before gilt futures can re-test session highs.

- Overall, market reaction to the Budget points to Chancellor Reeves meeting the short-term bar for fiscal credibility,

- Zooming out, questions surrounding overoptimistic OBR growth forecasts and whether or not Labour will go ahead with pension tax reforms in an election year remain evident.

- Support and resistance in futures remains located at 90.53 & 91.92, which effectively bookend today’s range.

- Yields 3-8bp lower, curve flatter.

- 2s registered fresh ’25 lows during the initial bid that followed the early release of the OBR’s Budget-related documentation but failed to retest those fresh ’25 lows on the second-round rally in gilts.

- 20+-Year yields registered fresh session lows during the second-round bid alongside the reduction in long end bucket issuance in the DMO’s gilt remit.

- Long end swap spreads now outperform, with the 30-Year spread within 0.5bp of ’25 closing highs, more than countering the recent narrowing that was driven by an increase in fiscal and political risk premia.

MNI FOREX: NZD Remains Strongest in G10, Post-Budget Boost for GBP

- NZD remains the strongest G10 currency following the hawkish cut from the RBNZ, with two additional factors bolstering the NZDUSD recovery. First of all, the dollar leg has also been playing ball, with December Fed cut pricing now standing at ~80% helping the DXY to pull lower from the strong touted resistance between 100.40-50. Furthermore, the strong bounce for major equity benchmarks is keeping risk on the front foot ahead of the Thanksgiving holiday.

- As such, NZDUSD is through 20-day EMA resistance, which intersected at 0.5659. This signals scope for a stronger recovery to 0.5725, which represents both the 50-day and prior trendline support turned resistance. 0.5800 remains a key medium-term pivot.

- While some may point to the higher-than-expected headroom announced in the budget as assisting today’s strong GBP performance, subject to the credibility of the forecasts, we have noted that overall, the main surprise of today’s budget was in the delivery and the timing, rather than the measures announced.

- Therefore, the constructive price action for sterling may be more a result of further position unwinds and the firmer risk sentiment. General dollar weakness has certainly supported this dynamic for GBPUSD, which has extended gains to 0.5% as we approach the Thursday’s Thanksgiving holiday in the US. The pair has further distanced itself from the 20-day EMA, placing the next focus on the key 50-day average, intersecting at 1.3261.

- USDJPY has seen a relatively contained range through the US session, broadly consolidating a 0.25% advance on the session. USDJPY has been largely immune to the extension of general dollar weakness, as higher US yields and equities provide offsetting factors.

- The overnight dip to 155.65 was very well supported, as domestic fiscal uncertainties in Japan surrounding the proposed stimulus plans remain an ongoing headwind for the yen, alongside China/Japan tensions continuing to simmer in the background. The path of least resistance appears to remain higher for USDJPY, despite the verbal warnings on potential FX intervention.

THURSDAY-FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 27/11/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 27/11/2025 | 0800/0900 | ** | Economic Tendency Indicator | |

| 27/11/2025 | 0830/0930 | ECB Cipollone Remarks at Euro Cyber Resilience Board | ||

| 27/11/2025 | 0900/1000 | ** | M3 | |

| 27/11/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 27/11/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 27/11/2025 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 27/11/2025 | 1100/1200 | ECB de Guindos Remarks at CEDE Congress of Executives | ||

| 27/11/2025 | 1330/0830 | * | Current account | |

| 27/11/2025 | 1330/0830 | * | Payroll employment | |

| 27/11/2025 | 1630/1630 | BOE Greene Speech at Goodbody Conference | ||

| 28/11/2025 | 2330/0830 | ** | Tokyo CPI | |

| 28/11/2025 | 2330/0830 | * | Labor Force Survey | |

| 28/11/2025 | 2350/0850 | * | Retail Sales (p) | |

| 28/11/2025 | 2350/0850 | ** | Industrial Production | |

| 28/11/2025 | 0700/0800 | *** | GDP | |

| 28/11/2025 | 0700/0800 | ** | Retail Sales | |

| 28/11/2025 | 0700/0800 | ** | Import/Export Prices | |

| 28/11/2025 | 0700/0800 | ** | Retail Sales | |

| 28/11/2025 | 0745/0845 | *** | HICP (p) | |

| 28/11/2025 | 0745/0845 | ** | PPI | |

| 28/11/2025 | 0745/0845 | *** | GDP (f) | |

| 28/11/2025 | 0745/0845 | ** | Consumer Spending | |

| 28/11/2025 | 0745/0845 | Payrolls | ||

| 28/11/2025 | 0800/0900 | *** | HICP (p) | |

| 28/11/2025 | 0800/0900 | ** | KOF Economic Barometer | |

| 28/11/2025 | 0800/0900 | *** | GDP | |

| 28/11/2025 | 0855/0955 | ** | Unemployment | |

| 28/11/2025 | 0900/1000 | *** | GDP (f) | |

| 28/11/2025 | 0900/1000 | *** | Bavaria CPI | |

| 28/11/2025 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 28/11/2025 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 28/11/2025 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 28/11/2025 | 1000/1100 | *** | Italy Flash Inflation | |

| 28/11/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 28/11/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 28/11/2025 | 1330/0830 | *** | GDP - Canadian Economic Accounts | |

| 28/11/2025 | 1330/0830 | *** | Gross Domestic Product by Industry | |

| 28/11/2025 | 1330/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 28/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 28/11/2025 | 1600/1100 | Finance Dept monthly Fiscal Monitor (expected) |