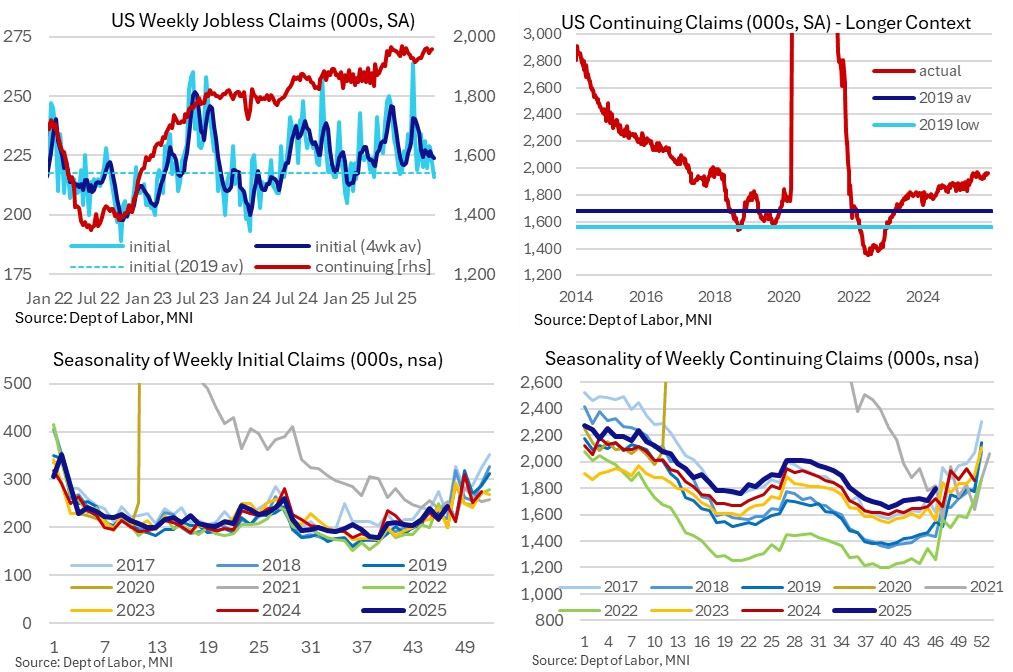

US DATA: Jobless Claims Data Don’t Suggest Any Further Rise In The U/E Rate

Latest weekly jobless claims data suggest lower layoffs than recent payrolls reference periods although re-hiring conditions remain subdued. It might see only limited improvement on net for the u/e rate since September’s surprise increase to 4.44%, a factor likely behind NY Fed Williams’ uncharacteristic steer to another “near term” cut last week. Recall that the November u/e rate will be published on Dec 16, after the Dec 9-10 FOMC meeting, and won’t retrospectively include one for October.

- Initial jobless claims were lower than expected at 216k (sa, cons 225k) in the week to Nov 22 after a downward revised 220k (initial 222k).

- That 220k covers the payrolls reference period and compares favorably to the 231k in Oct, 232k in Sep and 234k in Aug.

- The four-week average inched 1k lower to 224k, having plateaued in a 224-227k range since early October after easing from a recent high of 241k in September on Texas fraud grounds. Initial claims in the 220k region are still historically low.

- Continuing claims meanwhile were roughly as expected at 1960k (sa, cons 1963k) in the week to Nov 15 after a downward revised 1953k (initial 1974k).

- History suggests we’re likely to see another downward revision to this 1960k reading, likely leaving it below the 1957k matching the payrolls reference period for Oct, above the 1916k in Sept and possibly close to the 1944k from back in Aug.

- We focus on these payrolls reference periods particularly closely this time as it marks an important reference point for FOMC members trying to get a sense of latest unemployment rate clues. The next payrolls reports are due to come after the Dec 9-10 FOMC decision, with the committee going into the meeting after last week’s 0.12bp rise in the u/e rate to 4.44% back in September.

- Taken together, there isn’t yet any sign of the sharp rise in layoff announcements in the Challenger report for October filtering through to actual claims data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

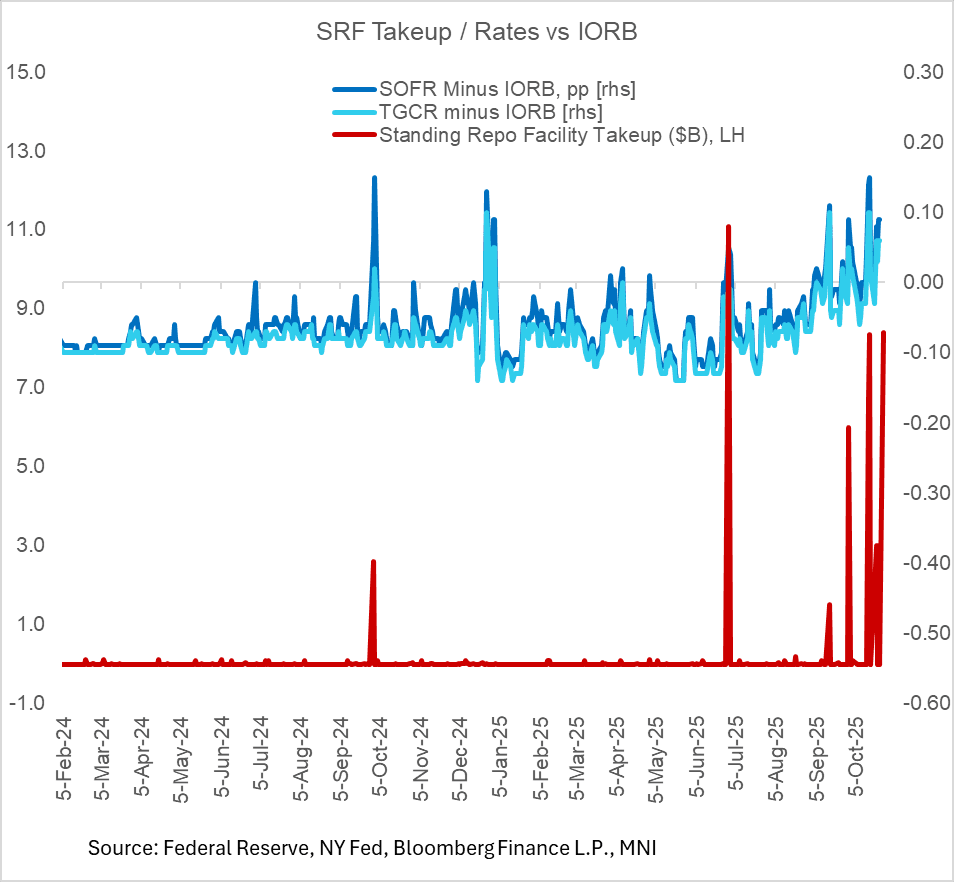

US TSYS/OVERNIGHT REPO: Post-June High In Standing Repo Facility Takeup (1/2)

Takeup of the Fed's Standing Repo facility hit a fresh post-June high of $8.4B this morning. This continues the recent uptick in takeup of Fed liquidity provision around non-month/quarter end pressure periods, and today's activity will only bolster conviction that the Fed will end QT at its meeting this week as hinted by Chair Powell this month - MNI's FOMC Meeting preview is here, in PDF

- As we note in the preview, takeup of the standing repo facility (which was made permanent in 2021) will have been thought of by the FOMC as a positive development in the evolution of the Fed's reserve management, allowing among other things for a smaller balance sheet than would otherwise be the case. And these are still low levels of takeup, relative to both historical SRF takeup in stress periods, and in terms of overall repo market transactions.

- But with pressures in funding markets increasingly evident, we think there will be little opposition to ending QT immediately.

- Among the many signals suggesting reserves are moving from a state of "abundant" to "ample", the triparty general collateral repo (TGCR) rate continues to publish solidly above the rate of interest paid on reserve balances (IORB). We take note of the evolution in these rates since ex-SOMA manager and current Dallas Fed Pres Logan's comments last year on the topic: "One sign liquidity remains in abundant supply, and not merely ample, is that money market rates continue to generally run well below IORB. The tri-party general collateral rate (TGCR) on repos secured by Treasury securities has been averaging 8 basis points below IORB. Because reserves and Treasury repos are both essentially risk-free overnight assets – and reserves are, if anything, more liquid – the spread of IORB over TGCR indicates reserves remain in relatively excess supply compared with other liquid assets".

- In contrast, in the last 4 sessions, TGCR has averaged 5bp above IORB. Similar has been seen in SOFR - IORB.

MNI EXCLUSIVE: Former Atlanta Fed President discusses the Fed outlook

Former Atlanta Fed President Dennis Lockhart discusses the Fed outlook.-- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

US: MNI POLITICAL RISK - Bessent Spikes Optimism For US-China Thaw

Download Full Report Here

- President Donald Trump will meet Japanese Prime Minister Sanae Takaichi for a bilateral meeting today, on his two-day stopover in Tokyo between the ASEAN and APEC summits.

- Treasury Secretary Scott Bessent expressed confidence that Trump and Chinese President Xi Jinping will sign a deal to extend the tariff truce and keep rare earths flowing when they meet on Thursday.

- Commerce Secretary Howard Lutnick said Japan's USD$550 billion investment will focus on energy, electricity, and national security.

- Trump secured “Agreements on Reciprocal Trade” with Malaysia and Cambodia and reached framework agreements with Thailand and Vietnam. US and Brazilian trade negotiators are expected to meet today.

- Markets are braced for a 'big tech' earnings and the FOMC's rate decision. Bessent has whittled Fed Chair candidates down to five, with NEC Director Kevin Hassett the bookmakers' favourite.

- The US government shutdown is expected to extend until at least mid-November, with Republicans and Democrats dug in on their respective positions.

- Senate Minority Leader Chuck Schumer (D-NY) will force votes this week on three bills relating to tariffs.

- Ukrainian President Volodymyr Zelenskyy still wants long-range missiles, despite Trump's oil sanctions.

- Trump is imposing an addtional 10% tariff on Canadian exports in response to a television ad.

- Trump’s USD$40 billion bet on Argentine President Javier Milei appears to have paid off.

- Senate Democrats will force a vote to block military strikes on Venezuela

- Poll of the Day: A new fault line in American politics may be emerging.

Full Article: US DAILY BRIEF