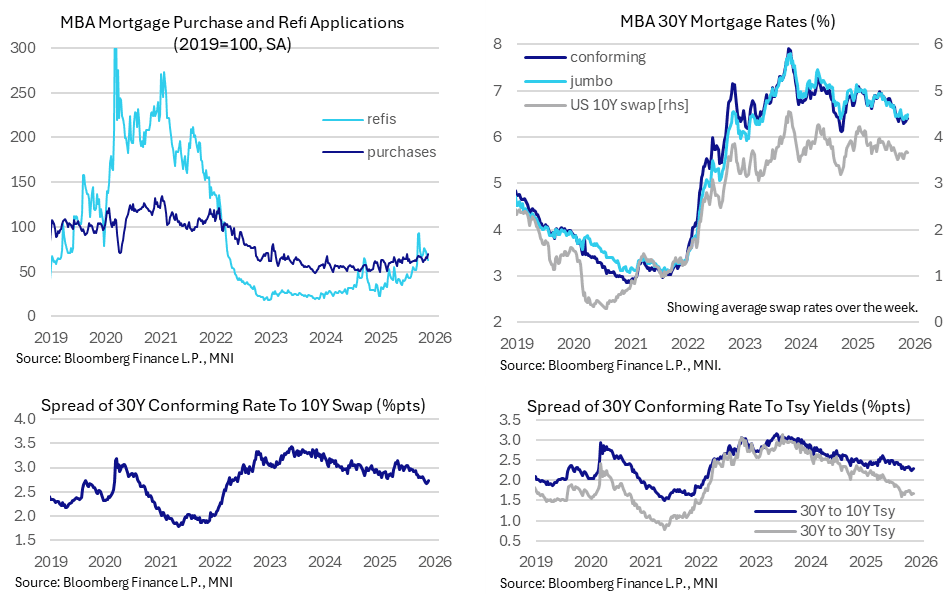

US TSYS: New Purchase Mortgage Applications Highest In Nearly Three Years

- MBA composite applications inched 0.2% (sa) higher in the week to Nov 21 after a -5.2% drop the week prior.

- The details are more interesting, with new purchase applications rising 7.6% for its sharpest increase since early July to take the level of applications to their highest since Jan 2023.

- On the flipside, refi applications fell another -5.7% after -7.3% to more than reverse strength in the second half of October on lower mortgage rates, leaving them at their lowest since early September.

- Putting these moves into context though, composite applications are at 66% of 2019 levels, new purchases still only at 70% and refis at 63%.

- The 30Y conforming mortgage rate increased 3bp for a third consecutive week, now at 6.40% having recently bottomed at 6.30% in late October.

- It looks to have followed previous increases in 10Y swap rates with a lag, which sees swap spreads tighten a little further although they’re still on the low side by recent standards.

- Specifically, the spread to 10Y swap rates increased 4bp to 273bp having recently troughed at 267bp for its lowest since Apr 2022, but is still below the average 285bp in Q1 and a rough range of 300 +/-5bp for some months after reciprocal tariff announcements in April prompted some additional caution in lending standards.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: US Dollar Tilts Lower Amid Optimism for Risk

- As equities broadly consolidate their surge higher to start the week, the USD is trading on the back foot, with the likes of EUR and GBP rising to session highs in recent minutes, playing catch up to the AUD, which continues to outperform on the session.

- For EURUSD, although signs appear nascent, the pair has found support below the 1.1600 handle and a positive close today would be the fourth consecutive winning session. As noted above, markets will continue to monitor key support at 1.1542. JP Morgan hav noted that a close above 1.1710 would bolster their long bias conviction. In the crosses, EURCHF has bounced around 50 pips from the key medium-term support around 0.9210.

- GBPUSD has returned to 1.3350, however the string of losing session last week keeps a bearish threat present. EURGBP has been consolidating back above 0.8700, but will need a break above 0.8769 to confirm a resumption of the uptrend.

- Greenback price action has allowed USDJPY to fade further, after the overnight high practically matched the key resistance point at 153.27. The weaker dollar index sees spot gold off its worst levels, despite remaining down 1.9% on the session.

US TSYS: Early SOFR/Treasury Option Roundup: Leaning Toward Puts

SOFR/Treasury options flow leaning toward downside puts outright & spread, modest overall volumes on day 27 of the US gov shutdown. Underlying futures modestly lower/off lows ahead two bill and Tsy coupon auctions today. Projected rate cut pricing vs. late Friday levels (*): Oct'25 steady at -24.2bp, Dec'25 at -49.4bp (-50.2bp), Jan'26 at -62.2bp (-63.7bp), Mar'26 at -73.5bp (-75.8bp).

- SOFR Options

- 6,600 SFRZ5 96.50/96.62 call spds ref 96.36

- 9,000 SFRZ5 96.25/96.37/96.50 put trees, 7.5

- -2,000 0QX5 96.25/96.75/96.87 put flys, 1.5 vs. 96.97/0.08%

- 2,500 0QX5 96.75 puts, 0.25 ref 97.005

- +2,200 SFRX5 96.50/96.56 call spds, 0.25 ref 96.36

- Treasury Options

- 16,900 Friday wkly 10Y/TYZ5 113 put spd

- 2,000 TUF6 104/104.25/104.38/104.5 put condors ref 104-14.75

- +1,250 TYZ5 114 straddles, 119 vs. 113-06/0.43%

- +1,500 TYZ5 112 calls, 126 vs. 113-09/0.87%

- +2,500 TYZ5 112.5 puts, 15 vs. 113-09/0.28%

- -1,200 TYZ5 113.25 straddles, 106-107 vs. 113-05.5/0.05%

- over -8,000 wk5 TY 113 puts, 10-11, (exp 10/31)

- -5,000 USZ5 116/118 put spds, 46 vs 117-28/0.28%

- -2,700 TUG6 104.5 straddles, 34-33

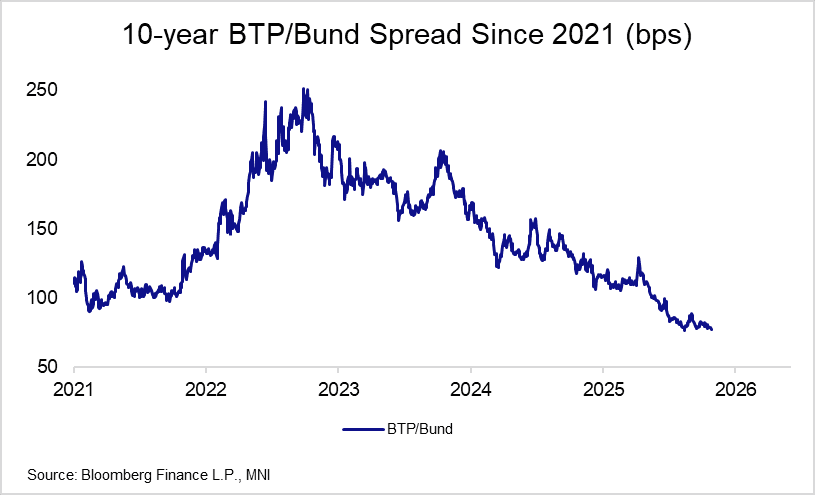

EGBS: /VOL: BTP/Bund Spread Eyeing Year-to-date Closing Low; Q3 Flash GDP Thurs

Improved risk sentiment and a pullback in EUR rates volatility has allowed the 10-year BTP/Bund spread to narrow to its lowest since mid-August. Confirmation of a US/China trade deal on Thursday could open the door for a test of the ~76.7bps year-to-date closing low seen on August 13. However, a push towards the 70bp figure may require stronger domestic activity signals, keeping focus on Thursday's flash Q3 GDP report (current consensus 0.1% Q/Q vs -0.1% prior).

- We have previously flagged that the biggest risk to Italian fiscal consolidation is not on the primary balance side, but on the country's subdued medium-term growth trajectory.

- The BTP/Bund spread is 1.5bps narrower at 77.5bps at typing, with benchmark Italian yields 0.5-1.5bps lower across the curve.

- EUR 3m10y swaption vol is ~1bp lower at 53.5bps, down from ~57bps on October 13. Goldman Sachs believe "the probability of a vol spike in Europe seems contained, given the decline in inflation, improved growth outlook and sufficient policy space to buffer eventual shocks". However, they note that "low valuations have lowered the bar for realized vol to outperform implied vol in Europe".