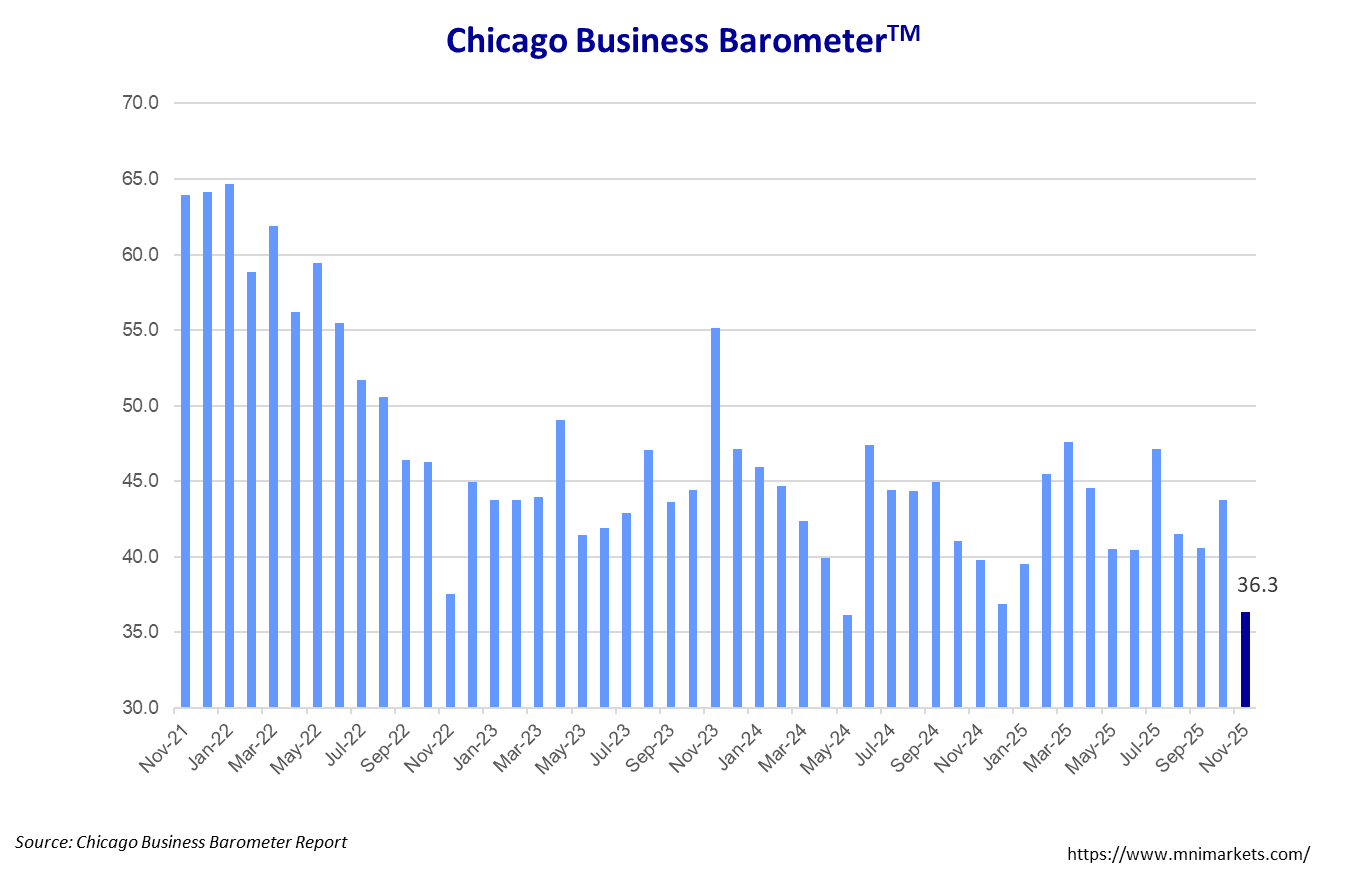

US DATA: Chicago Business Barometer™ - Fell To 36.3 In November

Nov-26 14:45

The Chicago Business Barometer™, produced with MNI, fell 7.5 points to 36.3 in November. The index is below 40 for the first time since January, and has remained below 50 for twenty-four consecutive months.

- The decrease was driven by declines in Order Backlogs, New Orders, Production and Employment. An increase in Supplier Deliveries provided a small offset

- Order Backlogs slipped 21.5 points, now at its lowest level since March 2009 and below 30 for the first time since June this year.

- New Orders dropped 12.0 points, the largest one-month fall since September 2023. The index is now at its lowest level since December 2024.

- Production slowed 4.7 points, more than reversing October’s rise. The index has remained below 50 for 21 of the last 23 months.

- Supplier Deliveries grew 7.4 points to the highest level since last December. No respondents reported faster Supplier Deliveries in November.

- Employment softened 4.5 points to the lowest level since May 2009. No respondents reported larger employment levels in November.

- Inventories declined 9.8 points, almost fully unwinding October’s increase.

- Prices Paid rose 5.8 points to the highest level in four months.

- The survey ran from November 1 to November 18.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Midmorning Adds: 5Y Midcurve Put Condor, 10Y Spds

Oct-27 14:30

- 20,000 wk5 FV 108.75/109/109.25/109.5 put condors (exp 10/31)

- 7,646 TYH6 107.5/109/110.5 put flys ref 113-03

- 2,000 TYF5/TYG5 112 put spds, 13 ref 113-03

- 2,000 USZ5 118/119/120/121 call condors, 118-09

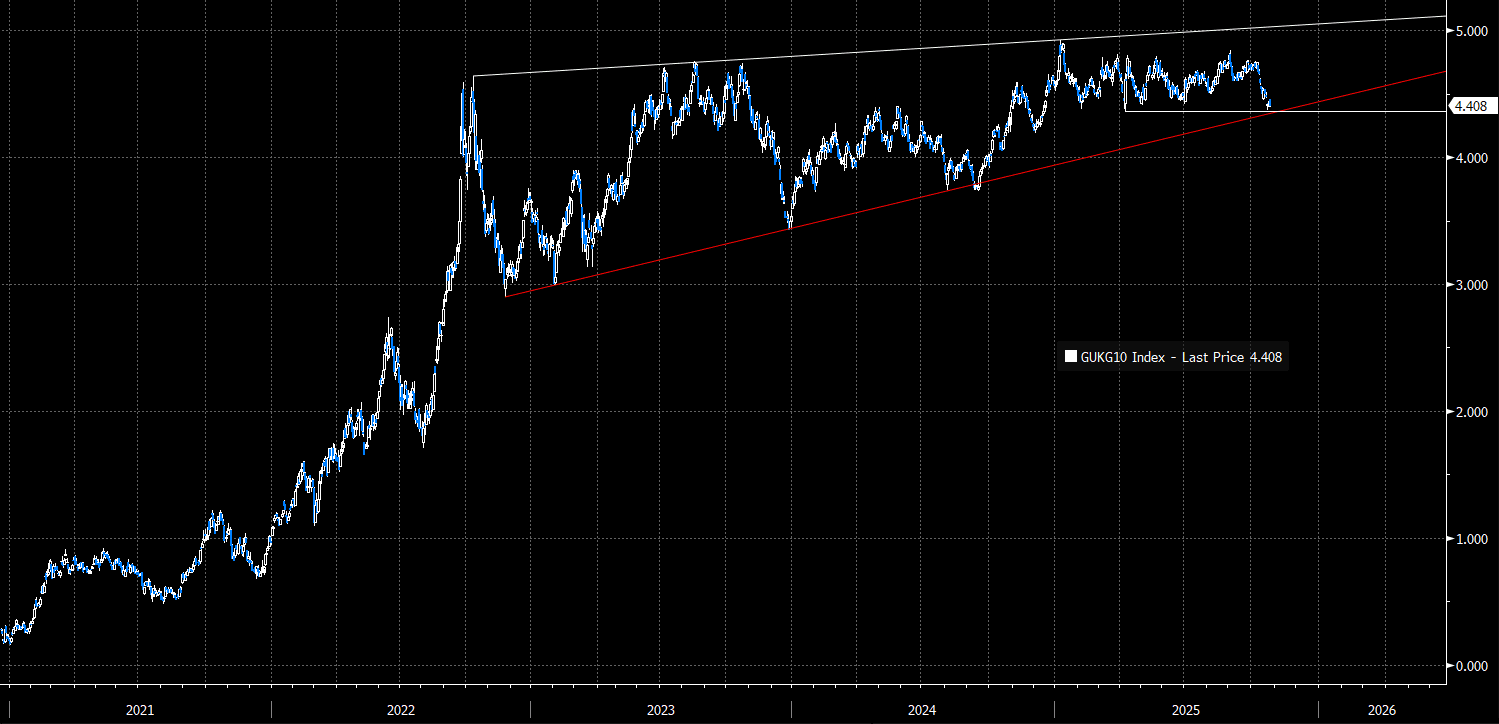

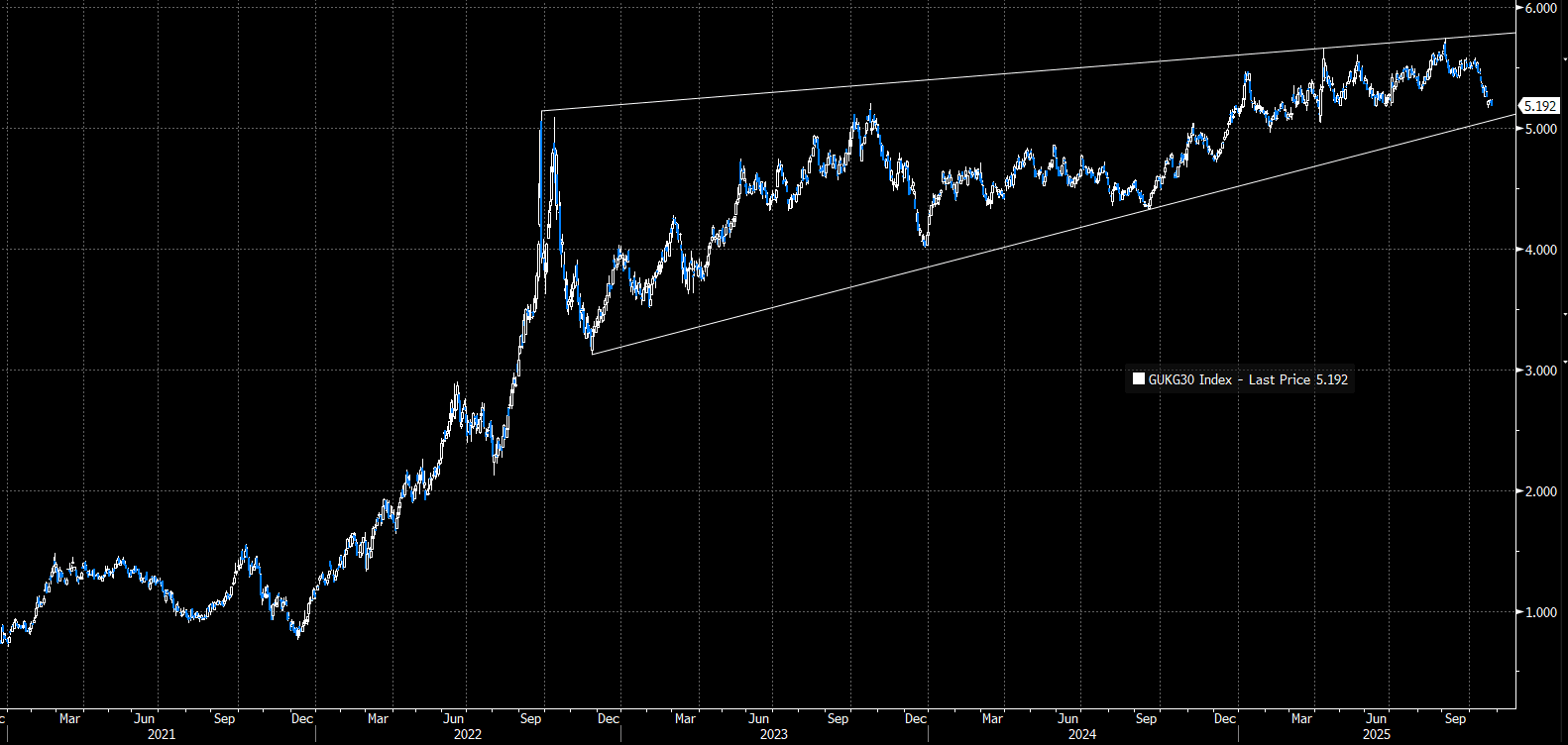

GILTS: Trendline Supports In 10- and 30-year Gilt Yields Still Intact

Oct-27 14:28

Despite last week’s pullback on softer-than-expected domestic inflation data, key trendline supports in 10- and 30-year Gilt yields remain intact. Both markets are still characterised by a rising wedge formation, underscoring a bullish (i.e. higher yield) trend.

- This week’s domestic data calendar is relatively light, leaving Gilts to be dictated by fiscal headlines and global developments. Gilts historically trade with a high beta to USTs, so spillover from this week’s Fed decision and the Trump/Xi meeting will be watched closely.

- 10-year yields reached a low of 4.369% on Wednesday, leaving the April 7 low of 4.363% unchallenged. The April 7 low resides close to trendline support drawn from the November 2022 low (4.344% today). Interaction with these levels will be key in the coming weeks. Our technical analyst notes that while the rising wedge formation is in favour of higher yields for now, it tends to occur at the final stages of a mature trend and thus highlights the risk of a reversal

- 30-year yields are hovering around 5.20%, down from ~5.50% at the start of this month. Trendline support drawn from the November low is seen at 5.07%.

- Goldman Sachs write that “with the budget likely to reinforce disinflationary dynamics, we think there will be ongoing relief for long-end risk premium in the Gilt curve - this was evident in the market reaction to the latest inflation miss, which outperformed the usual historical beta to inflation surprises”

Figure 1: 10-year Gilt Yields (Source Bloomberg Finance L.P)

Figure 2: 30-year Gilt Yields (Source Bloomberg Finance L.P)

SOFR OPTIONS: BLOCKs: Several Dec'25 Call Spds

Oct-27 14:04

- Block, 8,000 SFRZ5 96.50/96.56 call spds, 0.50 ref 96.36 at 0839:15ET

- Block, 8,000 SFRZ5 96.50/96.62 call spds, 0.50 ref 96.36 (adding to some 20k in pit) at 0839:15ET

- Block, 8,000 SFRZ5 96.43/96.50 call spds, 0.75 ref 96.36 at 0839:09ET