GILTS: Gilts Bull Flatten As Reeves Passes Short-Term Fiscal Hurdle

Nov-26 14:58

The rally stalls before gilt futures can re-test session highs.

- Overall, market reaction to the Budget points to Chancellor Reeves meeting the short-term bar for fiscal credibility,

- Zooming out, questions surrounding overoptimistic OBR growth forecasts and whether or not Labour will go ahead with pension tax reforms in an election year remain evident.

- Support and resistance in futures remains located at 90.53 & 91.92, which effectively bookend today’s range.

- Yields 3-8bp lower, curve flatter.

- 2s registered fresh ’25 lows during the initial bid that followed the early release of the OBR’s Budget-related documentation but failed to retest those fresh ’25 lows on the second-round rally in gilts.

- 20+-Year yields registered fresh session lows during the second-round bid alongside the reduction in long end bucket issuance in the DMO’s gilt remit.

- Long end swap spreads now outperform, with the 30-Year spread within 0.5bp of ’25 closing highs, more than countering the recent narrowing that was driven by an increase in fiscal and political risk premia.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Midmorning Adds: 5Y Midcurve Put Condor, 10Y Spds

Oct-27 14:30

- 20,000 wk5 FV 108.75/109/109.25/109.5 put condors (exp 10/31)

- 7,646 TYH6 107.5/109/110.5 put flys ref 113-03

- 2,000 TYF5/TYG5 112 put spds, 13 ref 113-03

- 2,000 USZ5 118/119/120/121 call condors, 118-09

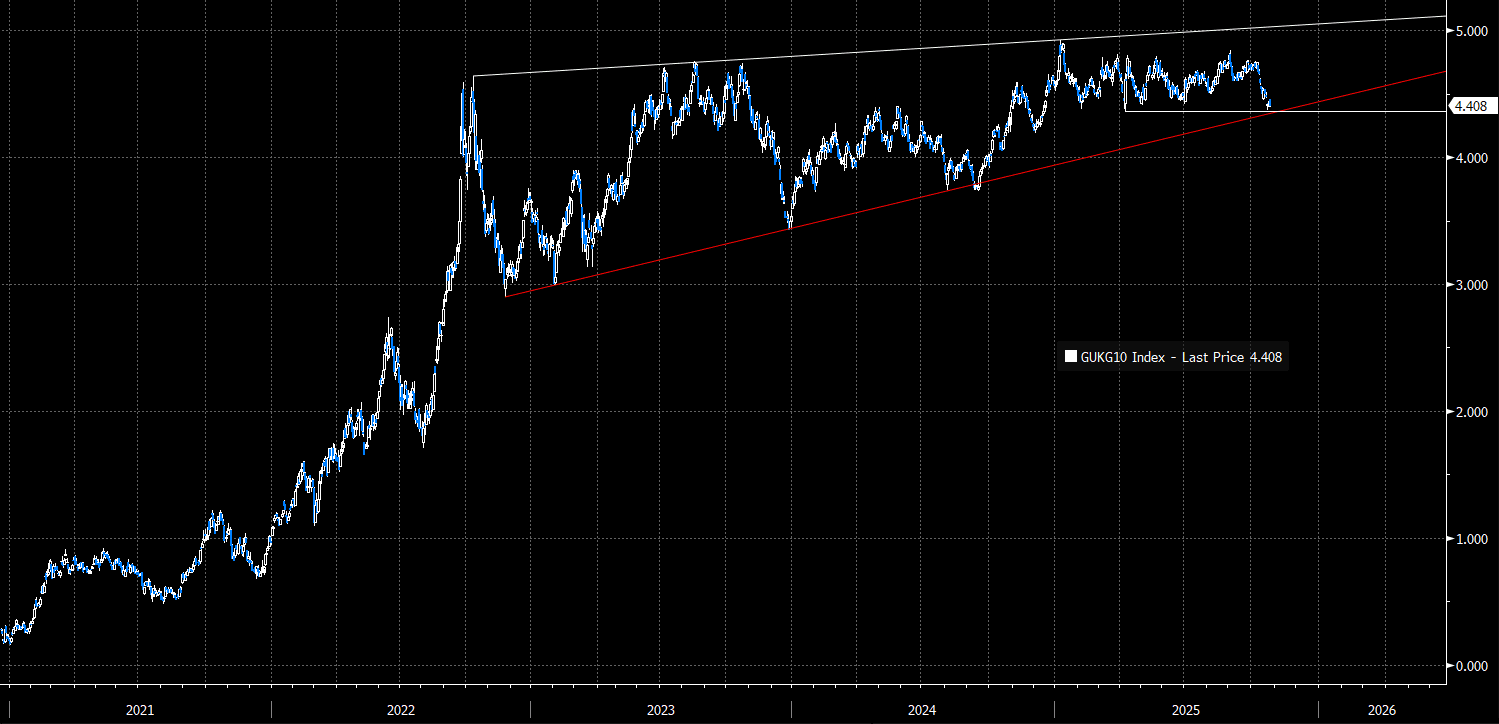

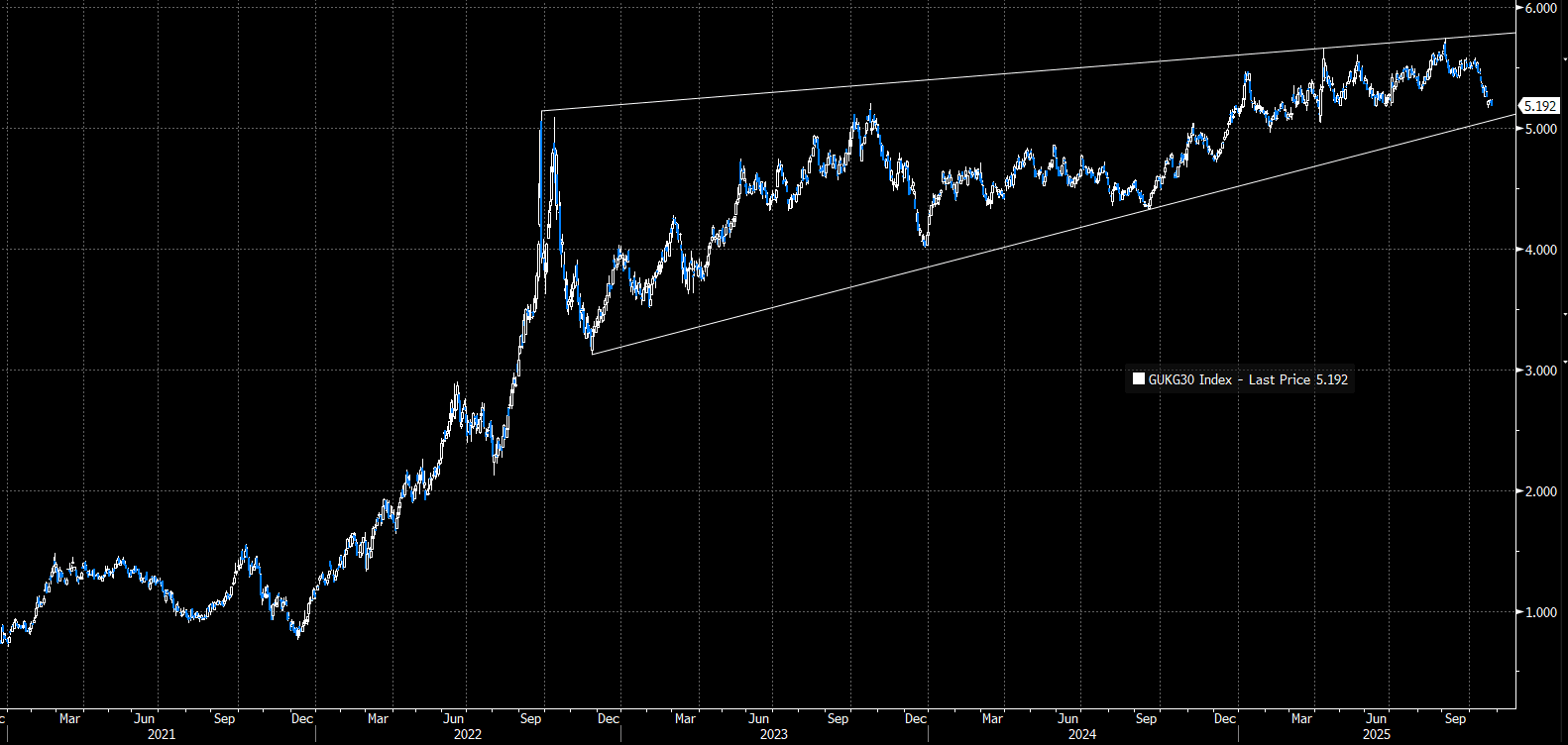

GILTS: Trendline Supports In 10- and 30-year Gilt Yields Still Intact

Oct-27 14:28

Despite last week’s pullback on softer-than-expected domestic inflation data, key trendline supports in 10- and 30-year Gilt yields remain intact. Both markets are still characterised by a rising wedge formation, underscoring a bullish (i.e. higher yield) trend.

- This week’s domestic data calendar is relatively light, leaving Gilts to be dictated by fiscal headlines and global developments. Gilts historically trade with a high beta to USTs, so spillover from this week’s Fed decision and the Trump/Xi meeting will be watched closely.

- 10-year yields reached a low of 4.369% on Wednesday, leaving the April 7 low of 4.363% unchallenged. The April 7 low resides close to trendline support drawn from the November 2022 low (4.344% today). Interaction with these levels will be key in the coming weeks. Our technical analyst notes that while the rising wedge formation is in favour of higher yields for now, it tends to occur at the final stages of a mature trend and thus highlights the risk of a reversal

- 30-year yields are hovering around 5.20%, down from ~5.50% at the start of this month. Trendline support drawn from the November low is seen at 5.07%.

- Goldman Sachs write that “with the budget likely to reinforce disinflationary dynamics, we think there will be ongoing relief for long-end risk premium in the Gilt curve - this was evident in the market reaction to the latest inflation miss, which outperformed the usual historical beta to inflation surprises”

Figure 1: 10-year Gilt Yields (Source Bloomberg Finance L.P)

Figure 2: 30-year Gilt Yields (Source Bloomberg Finance L.P)

SOFR OPTIONS: BLOCKs: Several Dec'25 Call Spds

Oct-27 14:04

- Block, 8,000 SFRZ5 96.50/96.56 call spds, 0.50 ref 96.36 at 0839:15ET

- Block, 8,000 SFRZ5 96.50/96.62 call spds, 0.50 ref 96.36 (adding to some 20k in pit) at 0839:15ET

- Block, 8,000 SFRZ5 96.43/96.50 call spds, 0.75 ref 96.36 at 0839:09ET