US: Democrats Could Win 'Redistricting War' If SCOTUS Declines To Restore TX Map

The Supreme Court is expected to announce a ruling any day now on a GOP-drafted congressional map that could net the party up to five new House seats in 2026. A SCOTUS decision to overturn a lower court block on the map is likely before the Dec. 8 filing deadline for candidates in Texas.

- Axios notes, “An anticipated ruling would mark the high court's first word on the redistricting wars that have defined the 2026 cycle. It wouldn't be the last: Lawsuits are anticipated from California to North Carolina...”

- Meanwhile, Punchbowl reports, “Indiana State Senate President Pro Tempore Rodric Bray said he’d bring the chamber back into session Dec. 8 to ‘make a final decision that week on any redistricting proposal sent from the House... The Indiana House will likely pass the redistricting proposal. Bray seems to realize he can’t ignore it. There will be tremendous pressure on Indiana Senate Republicans to pass the map.”

- Trump, who has engaged in a major pressure campaign against Indiana Senate Republicans who blocked redistricting, wrote on Truth Social, “I am glad to hear the Indiana House is stepping up to do the right thing.”

- The Cook Political Report writes that if Democrats’ redistricting push in Virginia succeeds, they could erase or overtake Republican gains in red states. Semafor notes, “It’s far from certain that Democrats will redraw the Virginia congressional map in time for 2026... But the prospect raises the stakes for Republicans [in Texas].”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

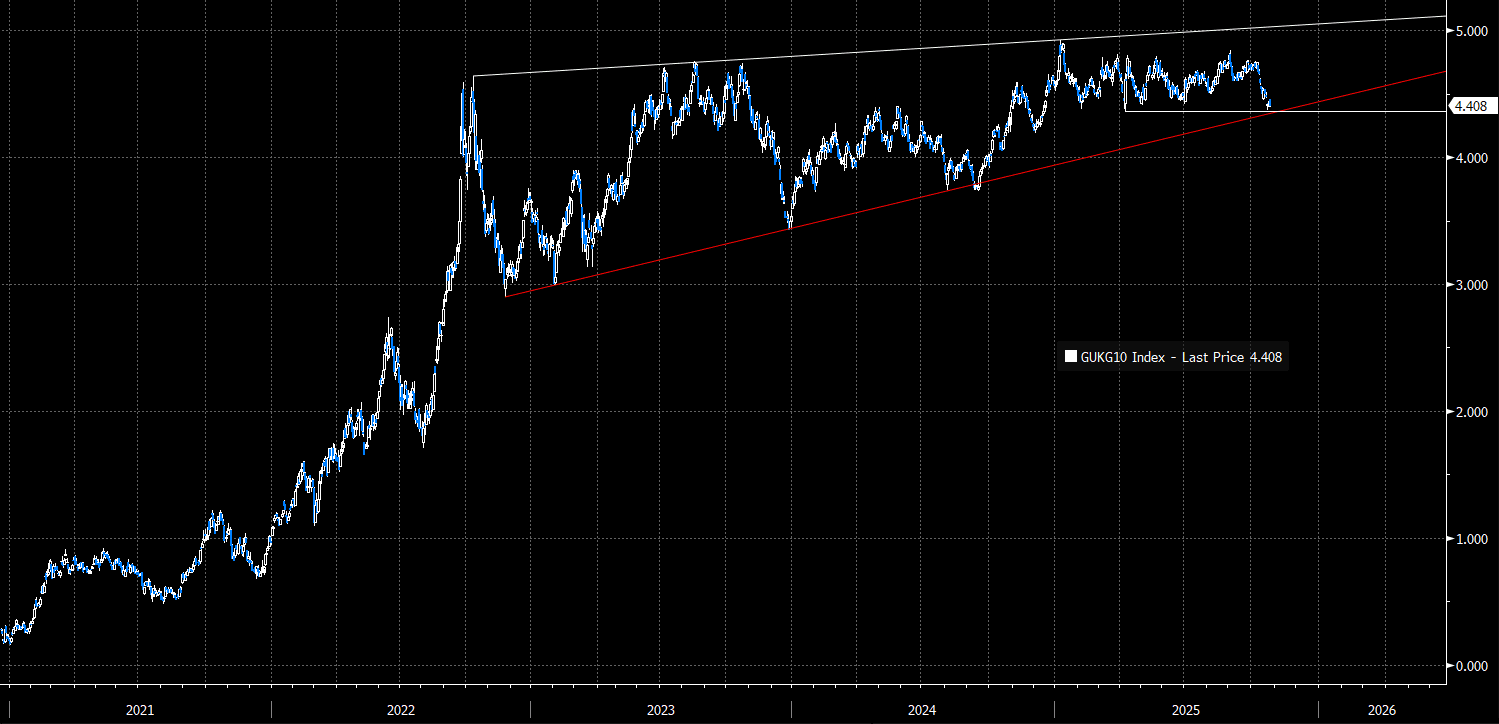

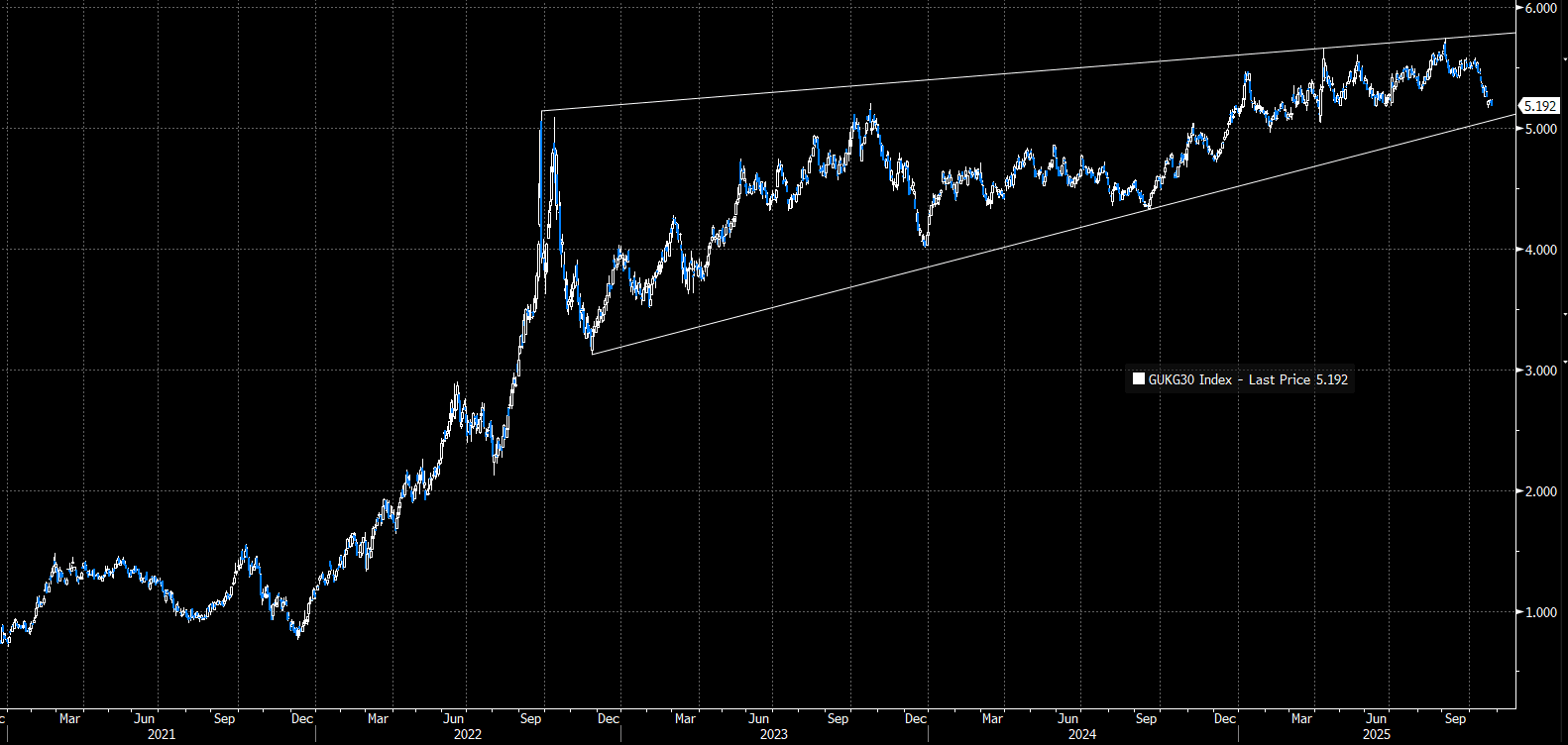

GILTS: Trendline Supports In 10- and 30-year Gilt Yields Still Intact

Despite last week’s pullback on softer-than-expected domestic inflation data, key trendline supports in 10- and 30-year Gilt yields remain intact. Both markets are still characterised by a rising wedge formation, underscoring a bullish (i.e. higher yield) trend.

- This week’s domestic data calendar is relatively light, leaving Gilts to be dictated by fiscal headlines and global developments. Gilts historically trade with a high beta to USTs, so spillover from this week’s Fed decision and the Trump/Xi meeting will be watched closely.

- 10-year yields reached a low of 4.369% on Wednesday, leaving the April 7 low of 4.363% unchallenged. The April 7 low resides close to trendline support drawn from the November 2022 low (4.344% today). Interaction with these levels will be key in the coming weeks. Our technical analyst notes that while the rising wedge formation is in favour of higher yields for now, it tends to occur at the final stages of a mature trend and thus highlights the risk of a reversal

- 30-year yields are hovering around 5.20%, down from ~5.50% at the start of this month. Trendline support drawn from the November low is seen at 5.07%.

- Goldman Sachs write that “with the budget likely to reinforce disinflationary dynamics, we think there will be ongoing relief for long-end risk premium in the Gilt curve - this was evident in the market reaction to the latest inflation miss, which outperformed the usual historical beta to inflation surprises”

Figure 1: 10-year Gilt Yields (Source Bloomberg Finance L.P)

Figure 2: 30-year Gilt Yields (Source Bloomberg Finance L.P)

SOFR OPTIONS: BLOCKs: Several Dec'25 Call Spds

- Block, 8,000 SFRZ5 96.50/96.56 call spds, 0.50 ref 96.36 at 0839:15ET

- Block, 8,000 SFRZ5 96.50/96.62 call spds, 0.50 ref 96.36 (adding to some 20k in pit) at 0839:15ET

- Block, 8,000 SFRZ5 96.43/96.50 call spds, 0.75 ref 96.36 at 0839:09ET

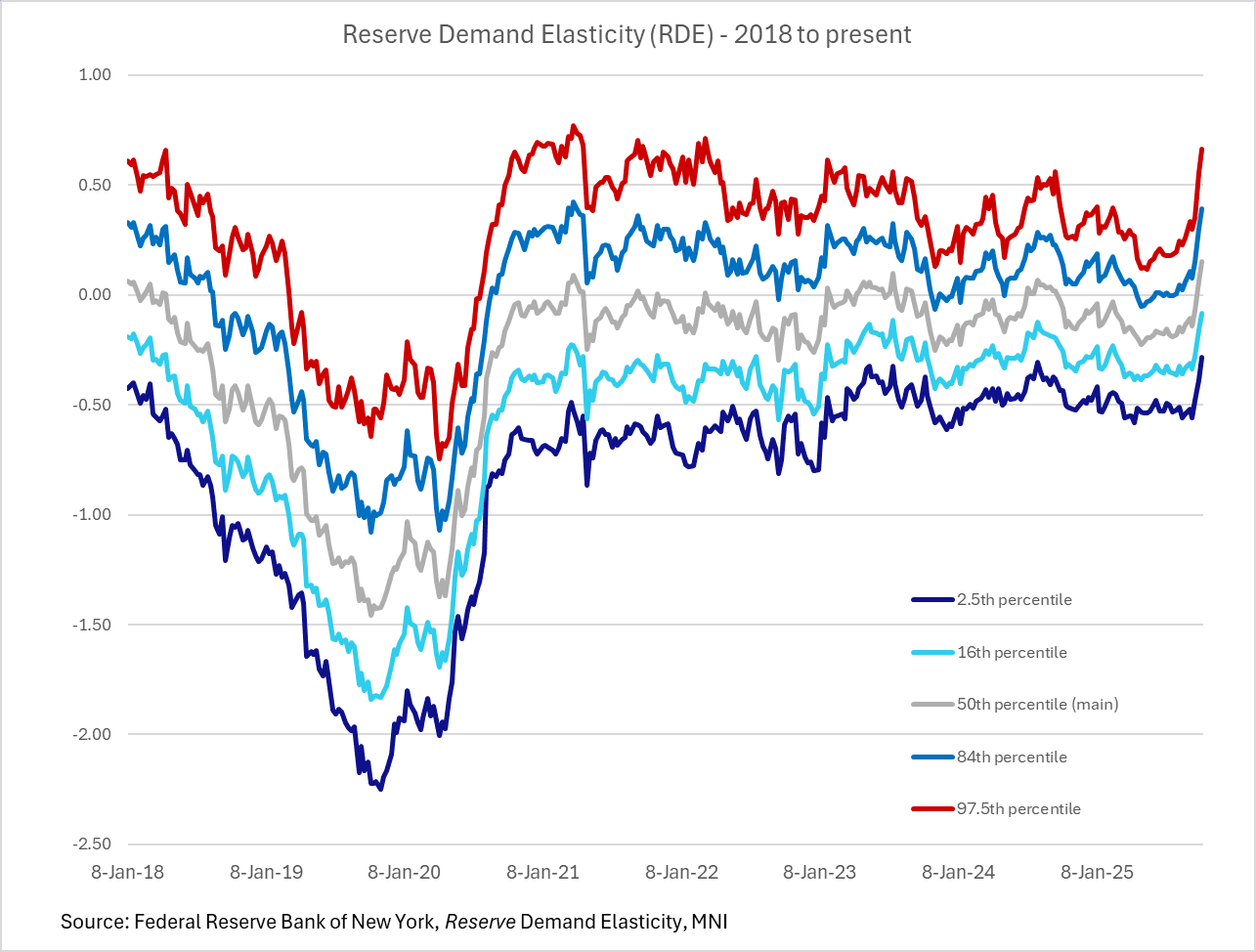

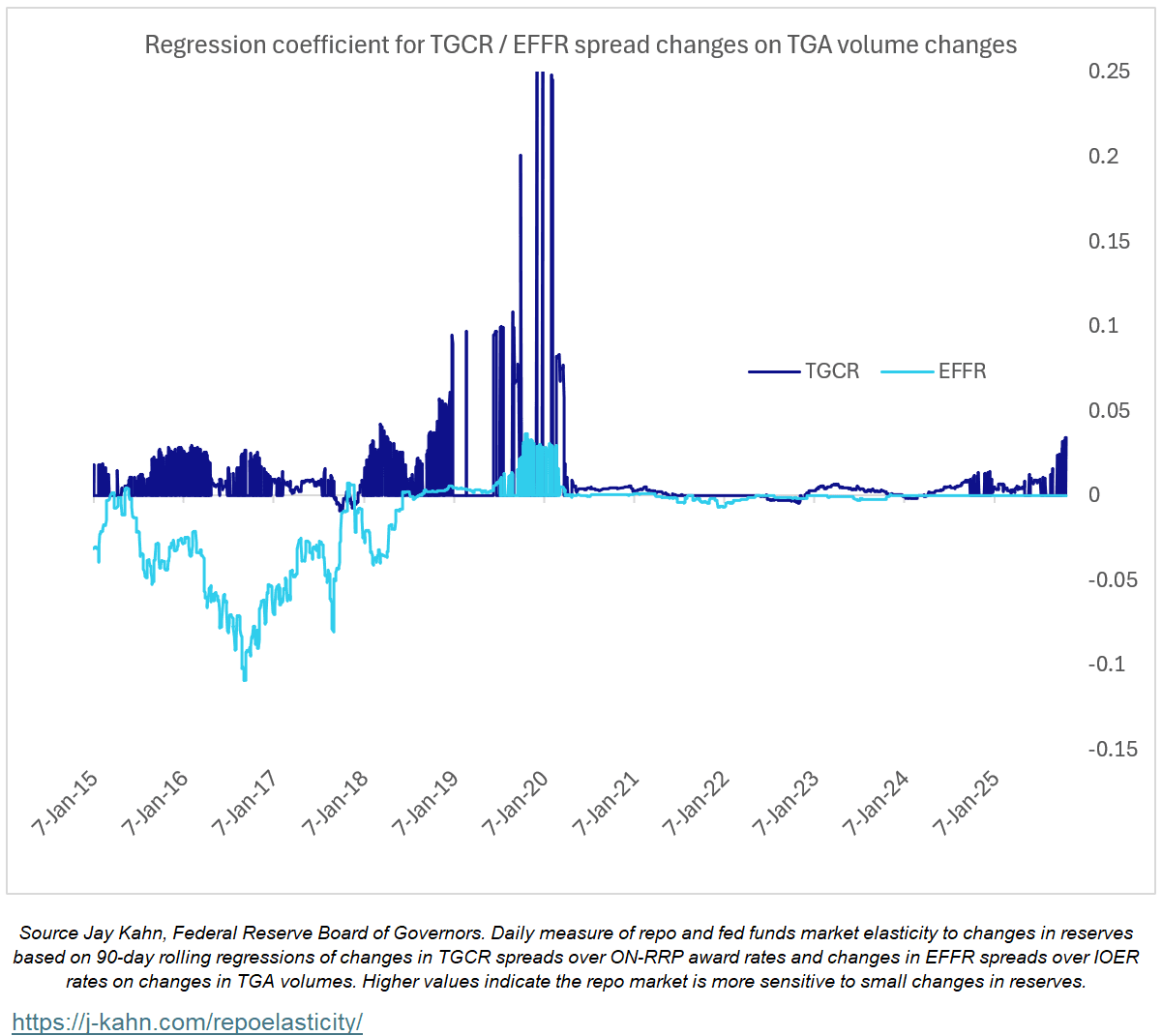

US TSYS/OVERNIGHT REPO: QT Set To End As Reserve Fall Elevates Pressures (2/2)

Outside of repo rates/spreads there are various measures of reserve elasticity that increasingly point to less-than-abundant reserves (note reserves + overnight reverse repo takeup fell last week to a fresh post-November 2020 low $2.93T vs over $3.6T as recently as June, the drop reflecting the buildup in the Treasury’s cash accounts at the Fed after the lifting of the debt limit).

- Such measures include the NY Fed's closely-watched calculation of reserve demand elasticity which has suggested that while the elasticity of the federal funds rate to reserve changes is very small, it was picking up - even up to latest data of Oct 10 before the latest repo market pressures.

- We also point to other measures with more up-to-date metrics such as one calculated on TGCR and EFFR elasticity to Treasury General Account volumes by Fed Board economist Jay Kahn which is showing increasing repo market sensitivity vs changes in reserves, a sign of rising scarcity/reducing abundance in reserves. This has continued to hit new post-2020 highs as of the latest calculation on Oct 23 (The intuition in using elasticity to the TGA, per the NY Fed paper upon which this calculation is based: "Increases in the TGA balance mechanically and exogenously reduce reserves, placing more pressure on banks' buffers. As reserves become less abundant and dealers rely more on MMFs for repo lending, this elasticity is expected to increase.")

- Again while these metrics aren't in hazardous territory, indeed compared to 2019 levels when the Fed had to restart asset purchases, they appear to be clearly trending in that direction.

- Against this backdrop we think it is likely that the Fed this week will announce an end to QT effective November 1, with maturing/prepaid MBS being reinvested back into Treasuries (and a chance they're reinvested back into bills). It may decide to announce a later end to QT, perhaps Dec 1. That's a distinction without much of a difference, though for a Fed that's already leaning into "risk management" rate cuts, it would stand to reason they would end QT earlier rather than later, with the only benefit of waiting perhaps another $20B taken off the balance sheet.

- If anything the Fed may decide this week to take actions consistent with a more rather than less cautious stance on liquidity conditions: we've seen speculation that the Fed could for example announce the restarting of temporary open market operations.