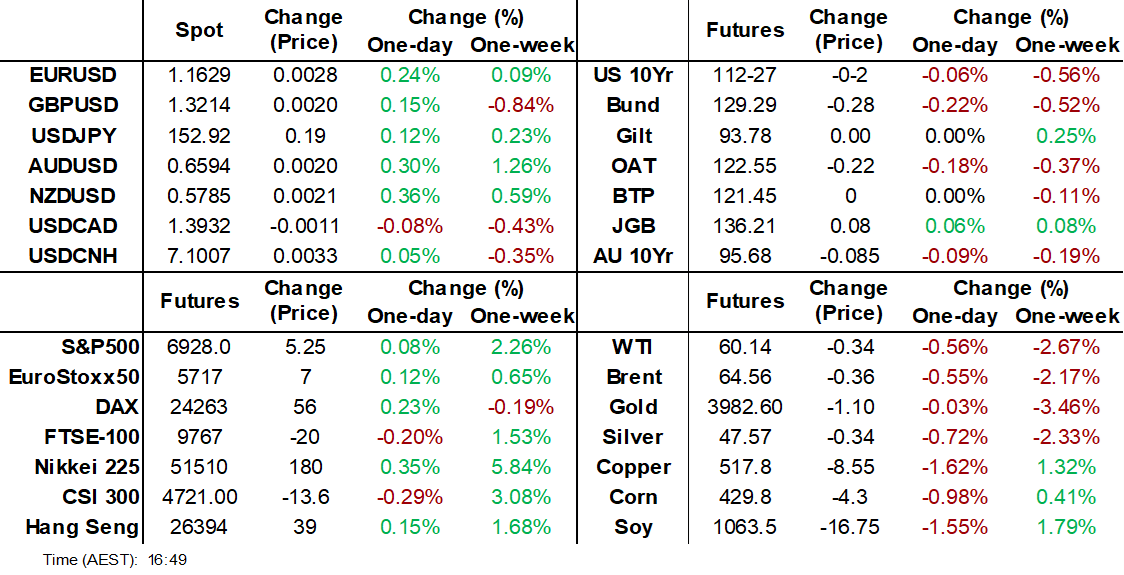

EUROPEAN MARKETS ANALYSIS: Constructive Trump-Xi Talks

- President Trump heralded the meeting with President Xi as 12 out of 10 with China agreeing to pause its rare earth licensing regime for at least a year and the US halving fentanyl tariffs immediately.

- US equity futures are currently higher post the news, with many of Asia's major currencies weaker.

- US treasury futures trended sideways today, after last night's dramatic shift and will look ahead to tonight's trading session to see if there is further follow on.

- Later the Fed’s Bowman gives pre-recorded remarks and Logan speaks at a bank funding conference. The ECB decision is expected to be a hold. Euro area Q3 GDP, EC October survey and German preliminary CPI print.

MARKETS

US TSYS: Could a Stronger GDP See Yields Higher Again? (amended)

- US treasury futures trended sideways today, after last night's dramatic shift and will look ahead to tonight's trading session to see if there is further follow on. The 10-Yr bond future was around 112-18+ by late afternoon in the trading day in Asia, up marginally from the US close of 112-25

Bonds rallied back with yields down 1-2bps in what appears to be profit taking. In what was a relatively outsized move overnight in yields, it was unsurprising to see a modest bounce back today.

- The US 2-Yr is -1.8bps lower at 3.582%

- The US 5-Yr is down -1.9bps at 3.694%

- The US 10-Yr has recovered a little, down -1.9bps at 4.06%

- The US 30-Yr is at 4.614% down -1.2bps on the day.

It remains to be seen whether the bond market will continue to sell of in US time overnight. The auction schedule is predominantly bills and unlikely to drive the direction for bonds.

Most likely catalyst for tonight would be data with initial jobless claims and GDP QoQ originally expected, GDP is expected to moderate to 3.0% from 3.8% but appears unlikely that it will be released. The likelihood is that positioning in treasuries is more balanced after last night's move. Should however GDP not moderate as much as forecasts, it could push on the market further sending yields higher.

US-CHINA: Trump Claims "Amazing Meeting" With Xi

- President Trump heralded the meeting with President Xi as 12 out of 10 with China agreeing to pause its rare earth licensing regime for at least a year and the US halving fentanyl tariffs immediately.

- The President indicated that the framework mapped out by US and Chinese officials in Malaysia over last weekend was largely agreed.

- The trade deal sees China resume soybean imports from the US, a key sticking point previously.

- Additionally the leaders agreed to remove shipping tariffs and fees on trade, and work together on Ukraine. Trump is hoping that China will ramp up investments in the US, with details to follow.

- “We do not always see eye-to-eye with each other, and it is normal for the two leading economies of the world to have frictions now and then,” Xi said. “And in the face of wind, waves and challenges, you and I, at the helm of Chinese relations, should stay the right course and ensure the steady sailing forward of the giant ship of China-US relations.” (per BBG)

- The deal is likely to be viewed as not a comprehensive trade deal but potentially sets the scene for further discussions.

- US equity futures are currently modestly lower post the news, with many of Asia's major currencies weaker. China's major bourses had been mixed earlier but have mostly turned moderately positive whilst the KOSPI's early gains faded along with the NIKKEI. US bonds haven't reacted, in line with prior trends. Oil is trending lower as prior comments from Trump on China buying Russian oil appear not to have been raised.

JGBS: Futures Outperforming On BoJ Hold, US-JP 10yr Re-Widens

JGB futures are holding higher post the lunch time break as markets digest the BOJ on hold outcome. This meeting delivered little for BoJ hawks, with the vote to hold rates maintained at 7-2, while forecast changes were modest. All in all it suggested a high bar for the core board viewpoint to shift to a hike by Dec. JGB futures were last 136.18, +.05 versus settlement levels. recent lows rested under 135.80, while this week's high was above 136.30. We are still under important support though (137.30).

- Cash JGB yields have shifted lower, although moves aren't large. Still, this leaves us underperforming the recent Tsy shifts. The US-JP 10yr government bond yield differential is back close to +242bps (against recent lows of +230bps).

- The 10yr JGB is back to 1.65%, backing away once again from a 1.70% upside test. The 30yr was around 3.05%, so on track to close under 100-day EMA support.

- The 2/30s curve is little changed at +211.5bps.

- Note tomorrow we get Sep jobless rate figures, as well as Tokyo CPI. Before then we get Ueda's press conference in a little over an hour.

BOJ: On Hold With A 7-2 Vote, Commentary Suggests High Bar For Dec Hike

The BoJ left rates on hold as expected. Once again there were two dissenters, board members Takata and Tamura voted in favor of a rate hike but this viewpoint is not shared by the majority of the board, leaving the decision to hold rates steady at a 7-2 vote. There had been a focus point prior to the meeting that we may see another board member join the dissenting camp, but this hasn't materialized. This coupled with little change in the forecast projections, has left BoJ hawks with little to focus on. In turn, USD/JPY has bounced (back above 153.00, but still sub bull trigger at 153.27), while JGB futures are up from earlier lows and local stocks are firmer (NKY 225 up 0.60%).

- The forecast projections only saw minor adjustments, with core, ex energy, CPI nudged up to 2.0% for the 2026 financial year, from 1.9% prior. The 2025 and 2027 projections at 2.8% and 2.0% were unchanged respectively. The core CPI projects were all steady 2.8% for 2025 financial year and 1.8% for next and 2.0% for 2027.

- On growth, the current financial year projection was nudged up to 0.7% from 0.6%, while 2026 was unchanged at 0.7% and 2027 is at 1%.

- The central bank also noted inflation is likely to decelerate sub 2% in the first half of the 2026 financial year and that underlying inflation is likely to remain sluggish. On growth it said the economic risk balance for the next financial year is on the downside. This reflects likely slower offshore growth and the impact of trade policies.

- Still, it expects the price trend to be in line with the inflation target in the 2nd half of the outlook (no change on this point) and retains its bias to raise rates if the outlook is realized.

- This backdrop suggests the bar is quite high for the core board viewpoint to shift to a hike by the Dec meeting.

- We now await Ueda' press conference in a few hours (3:30pm local time).

JAPAN DATA: Offshore Investors Pile Back Into Local Stocks, Multiple Supports

The main standout from Japan's offshore weekly investment flow data (for the week ending Oct 24) was the continued inflows from offshore investors into local stocks. In the last 4 weeks we have seen cumulative net inflows of nearly ¥6.5trln. This comes as onshore equities continue to rally, the NKY comfortably breaking above 50000. Sentiment is being boosted by broader global gains, with tech/AI optimism still strong, while the new Takaichi regime is also expected to be pro-growth. Higher USD/JPY levels have also likely helped exporter names. The return of offshore inflows has more than offset the outflows we saw from late Aug to late Sep.

- Elsewhere, flow trends were negative for offshore buying of local bonds, for the second straight week. The cumulative flow backdrop for this space has been close to flat in recent months though.

- Japan investors sold offshore bonds for the second straight week. Indeed, we have seen net selling four out of the last five weeks for this segment. Still, cumulative net buying is still positive going back to late Aug/early Sep. Global bond returns have stabilized in recent weeks and dipped post Wednesday's hawkish Fed 25bps cut.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Oct 24 | Prior Week |

| Foreign Buying Japan Stocks | 1344.2 | 752.6 |

| Foreign Buying Japan Bonds | -253.5 | -25.5 |

| Japan Buying Foreign Bonds | -351.4 | -664.4 |

| Japan Buying Foreign Stocks | -62.1 | -288.1 |

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Holding Weaker But Up From Lows, 3yr Yield Back Around Cash Rate

Aussie bond futures are holding losses, but are away from session lows. Some support likely emerging from the drift in US Tsy futures. JGB futures are also higher post the on hold BoJ outcome (which gave few hints around hike timing). Broader risk focus is on the Trump-Xi meeting, which has just concluded. Trump is making positive comments around the outcome of the meeting, although broader risk appetite is still skittish.

- 3y futures were last 96.38, off 5bps and around late Sep/earlier Oct lows. Session lows were at 96.335. 10yr futures were last 95.69, -7.5bps, (against session lows of 95.645).

- Like the NZGB space, ACGB yields are away from earlier highs. We are still 3-7bps higher, led by the back end. The 3yr yield is back around 3.60%, so in line with the RBA cash rate. Earlier highs were through this level (near 3.64%).

- The AU-US 10yr spread is holding higher, last +23bps. Upside focus will remain on recent highs beyond +30bps.

- RBA pricing has little easing risks priced into year end, while a full cut is not priced until August next year.

- Tomorrow is Q3 PPI, along with Sep private sector credit.

NZGBS: Yields Higher But off Best Levels, 2/10s Back Under +150bps

NZGB yields are holding firmer, but are away from session highs. We are around 2.5-4.5bps higher, with the belly of the curve leading in yield terms. Moving off session highs may have been helped by a slightly weaker US Tsy lead so far today, although Tsy yield losses are not much beyond 1bps at this stage. The 2yr is around 2.60%, so not breaking above 20-day EMA resistance yet. The 10yr is around 4.08%, but did get beyond 4.14% earlier. The 2/10s curve is off earlier highs, last +148bps, after printing +152bps earlier.

- The 2yr swap rate, which has arguably led the firmer yield tone in NZ, is off nearly 4bps to 2.42%. We are still some distance from recent lows near 2.25%.

- On the data front today, ANZ business confidence rose to its highest since February at 58.1 in October. The RBNZ cut rates 50bp to 2.5% on 8 October with more signalled, but ANZ doesn’t believe it boosted sentiment. However, interest-sensitive sectors are outperforming. The activity outlook was more subdued but still rose 1.2 points to 44.6. Inflation expectations ticked higher but pricing intentions were lower. The RBNZ is likely to cut rates again on 26 November and the ANZ survey confirmed that while the recovery continued it remains soft and uneven.

- Nov easing is priced around 90% for a 25bps cut by the market so away from recent extremes of beyond 100%. 2026 implied rate levels have edged up, but this is likely spill over from the Fed overnight.

- Tomorrow, we get the Oct ANZ consumer confidence print.

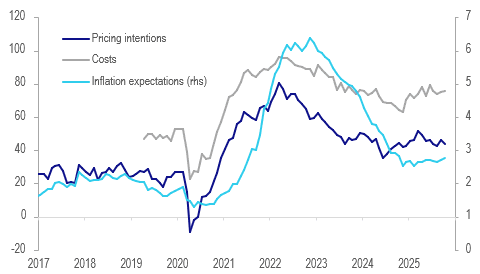

NEW ZEALAND: Recovery Continues But Soft & Uneven, Further Easing Likely

ANZ business confidence rose to its highest since February at 58.1 in October. The RBNZ cut rates 50bp to 2.5% on 8 October with more signalled, but ANZ doesn’t believe it boosted sentiment. However, interest-sensitive sectors are outperforming. The activity outlook was more subdued but still rose 1.2 points to 44.6. Inflation expectations ticked higher but pricing intentions were lower. The RBNZ is likely to cut rates again on 26 November and the ANZ survey confirmed that while the recovery continued it remains soft and uneven.

NZ ANZ business survey

Source: MNI - Market News/LSEG

- Inflation expectations printed at 2.75% after 2.7% but pricing intentions fell 2 points to 43.9, around the Q3 average. Costs remain elevated at 75.8 and 3-mth ahead expectations stable at 2.4%. Wage expectations a year ahead rose to 2.6% from 2.4%.

- While activity compared to a year ago, a good GDP indicator, was steady at 4.6, retail rose sharply reflecting RBNZ easing feeding through to lower household interest payments.

- In terms of the labour market, employment compared to a year ago improved slightly to -10 from -10.9 but services shifted positive to +1 and its employment intentions were robust at +18. Overall intentions eased 1.4 points to 15.0. Filled jobs suggest that the labour market stabilised in Q3. The official data are out 5 November.

- There was a 4 point pickup in investment intentions to +21.6 driven by the services sector (+28), while construction continues to underperform (+4). Construction sentiment though is picking up with residential up 15 points to 36.6 and commercial +1.5 to 33.3.

- Export intentions continue to trend higher after the May low with agriculture positive.

NZ ANZ business price/cost components

Source: MNI - Market News/LSEG

FOREX: USD/JPY Off Post BoJ Highs, A$ & NZD Still Higher

The USD is weaker, but holding recent ranges. The BBDXY off around 0.15% to be near 1212. USD/JPY has been volatile rising above the 153.00 post the dovish on hold BoJ. The central bank meeting outcome contained little for hawks (7-2 vote to hold rate, while forecast changes were minimal). We got to highs of 153.14 (leaving the bull trigger in the pair at 153.27 intact). We were last near 152.70, little changed for the session, as risk sentiment has softened a touch post the Trump-XI meeting. Trump has spoke about broad agreement on a lot of issues (including lowering tariffs related to fentanyl) but we are yet to hear from the China side. Trump also stated that a comprehensive statement would be released later. US equity futures have slipped back into the red. US Tsy yields are down a touch.

- AUD and NZD are holding gains, but remain within recent ranges. AUDUSD is up 0.3% to 0.6592 approaching 0.6600 again but reaching a high just short at 0.6593. NZDUSD is also 0.3% higher at 0.5779 following an intraday high of 0.5780. This means that AUDNZD is steady oscillating around 1.1405.

- Later the Fed’s Bowman gives pre-recorded remarks and Logan speaks at a bank funding conference. The ECB decision is expected to be on hold. Euro area Q3 GDP, EC October survey, German preliminary CPI & September unemployment print.

ASIA STOCKS: New Highs For KOSPI : BOJ on Hold : JCI Back Above Key Level

As President Trump and Xi met in Korea, equity futures rose on hopes that easing trade tensions could be supportive of global growth going forward. South Korea announced a trade deal today that would result in $150bn of Korean investment in US shipbuilding, with a further $200 bn potential to follow. Korea agreed to buy significant amounts of US oil and gas which gave the KOSPI a further kick towards a new all time high. Elsewhere stocks in Japan were led by their tech sector following overnight positive news from Alphabet and Nvidia whilst the BOJ failed to surprise markets, keeping rates at 0.50%.

- The NIKKEI hit new highs of 51,561 on tech and BOJ hold and is up +0.50% today.

- The Hang Seng led China's major bourses with gains of 0.55% to 26,487, consolidating above the 20-day EMA of 26,175 whilst other major bourses were mixed

- The TAIEX only had limited follow on from the Tech sector new overnight, gaining just +0.22% despite up strongly to hit new highs.

- The KOSPI was buoyed by the trade deal and the uncertainty that it removed and rose +0.23% to another new high. The KOSPI is up now 19% over the last month, challenging valuations relative to bonds.

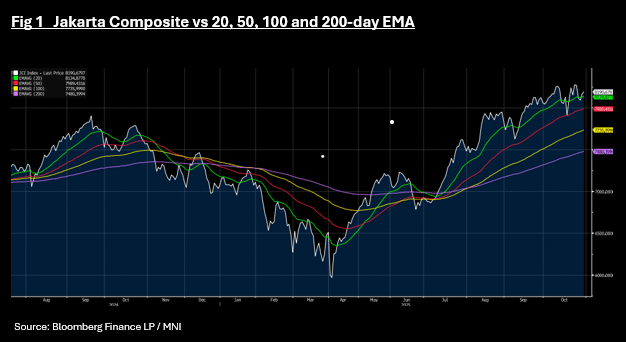

- The Jakarta Comp has now delivered two days of gains, to trade back above the 20-day EMA after dipping below as the NIFTY 50 opens having closed yesterday at a new high.

OIL: Crude Dips As Trump-Xi Meeting Ends With No Announcement

Oil has been range trading during today’s APAC session as it waits for news following the meeting between Presidents Trump and Xi, which has ended. The lack of news at this point has driven prices lower. The market is also on hold ahead of Sunday’s OPEC meeting which is likely to see another 137kbd increase in the output target as it unwinds previous curbs but it is coming at a time of already elevated supply.

- WTI is down 0.5% to $60.19/bbl but has traded today between $60.05 and $60.45. It was around $60.40 before it was announced that Trump had boarded Air Force One. Brent is 0.3% lower (December contract) at $64.76, after reaching $64.96, but off the day’s trough at $64.51. The USD index is down 0.1%.

- Uncertainty is high for oil with the Fed outlook unclear given dissenters and lack of data, ongoing trade tensions, elevated supply and sanctions. Trump said that he may discuss China’s Russian oil purchases with Xi when they met today.

- Later the Fed’s Bowman gives pre-recorded remarks and Logan speaks at a bank funding conference. The ECB decision is expected to be on hold. Euro area Q3 GDP, EC October survey, German preliminary CPI & September unemployment print.

Gold Range Trading On Uncertain Fed Outlook & Wait For US-China News

Gold prices reached $3966.52/oz earlier before falling to $3915.52 but are now 0.2% higher on the day at $3938. Its relatively narrow range reflects uncertainty over the Fed outlook with Chair Powell noting the variation in views. There were two dissenters this month with a vote for no change and one for a 50bp cut. The lack of data is also clouding the outlook. It has found support from a slightly lower US dollar and 2-year yield but stronger US equity futures are offsetting this.

- Presidents Xi and Trump have just met in South Korea with no announcements yet, which may be supporting bullion’s latest uptick.

- US Treasury Secretary Bessent said earlier this week that a draft US-China trade agreement had been reached. There have also been comments that China will increase its US soyabean imports. The hope is that a deal will avoid additional 100% US tariffs on 1 November and ease restrictions of China’s rare earth mineral exports needed for tech production.

- Silver has been in a narrow range today. It is down 0.1% to $47.53 off the intraday low of $47.269. It reached $47.970 earlier in the session. Both gold and silver remain in overbought territory.

- Later the Fed’s Bowman gives pre-recorded remarks and Logan speaks at a bank funding conference. The ECB decision is expected to be on hold. Euro area Q3 GDP, EC October survey, German preliminary CPI & September unemployment print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 30/10/2025 | 0630/0730 | *** | GDP (p) | |

| 30/10/2025 | 0630/0730 | ** | Consumer Spending | |

| 30/10/2025 | 0700/0800 | ** | Retail Sales | |

| 30/10/2025 | 0800/0900 | *** | HICP (p) | |

| 30/10/2025 | 0800/0900 | ** | KOF Economic Barometer | |

| 30/10/2025 | 0800/0900 | ** | Economic Tendency Indicator | |

| 30/10/2025 | 0855/0955 | ** | Unemployment | |

| 30/10/2025 | 0900/1000 | *** | GDP (p) | |

| 30/10/2025 | 0900/1000 | *** | GDP (p) | |

| 30/10/2025 | 0900/1000 | *** | Bavaria CPI | |

| 30/10/2025 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 30/10/2025 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 30/10/2025 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 30/10/2025 | 1000/1100 | ** | EZ Unemployment | |

| 30/10/2025 | 1000/1100 | *** | EZ GDP 1st (Prelim Flash) | |

| 30/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 30/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 30/10/2025 | 1230/0830 | * | Payroll employment | |

| 30/10/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/10/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/10/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 30/10/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 30/10/2025 | 1315/1415 | *** | ECB Deposit Rate | |

| 30/10/2025 | 1315/1415 | *** | ECB Main Refi Rate | |

| 30/10/2025 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 30/10/2025 | 1345/1445 | ECB Press Conference | ||

| 30/10/2025 | 1355/0955 | Fed's Michelle Bowman | ||

| 30/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 30/10/2025 | 1515/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 30/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 30/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 31/10/2025 | 2330/0830 | ** | Tokyo CPI | |

| 31/10/2025 | 2330/0830 | * | Labor Force Survey | |

| 31/10/2025 | 2350/0850 | * | Retail Sales (p) | |

| 31/10/2025 | 2350/0850 | ** | Industrial Production | |

| 31/10/2025 | 0030/1130 | * | Producer price index q/q | |

| 31/10/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/10/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 31/10/2025 | 0700/0800 | ** | Import/Export Prices | |

| 31/10/2025 | 0700/0800 | ** | Retail Sales | |

| 31/10/2025 | 0730/0830 | ** | Retail Sales | |

| 31/10/2025 | 0745/0845 | *** | HICP (p) | |

| 31/10/2025 | 0745/0845 | ** | PPI | |

| 31/10/2025 | 0930/0930 | Blue Book / Pink Book | ||

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1000/1100 | *** | Italy Flash Inflation | |

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/10/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/10/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/10/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/10/2025 | 1330/0930 | Dallas Fed's Lorie Logan | ||

| 31/10/2025 | 1342/0942 | *** | MNI Chicago PMI |