JAPAN DATA: Offshore Investors Pile Back Into Local Stocks, Multiple Supports

The main standout from Japan's offshore weekly investment flow data (for the week ending Oct 24) was the continued inflows from offshore investors into local stocks. In the last 4 weeks we have seen cumulative net inflows of nearly ¥6.5trln. This comes as onshore equities continue to rally, the NKY comfortably breaking above 50000. Sentiment is being boosted by broader global gains, with tech/AI optimism still strong, while the new Takaichi regime is also expected to be pro-growth. Higher USD/JPY levels have also likely helped exporter names. The return of offshore inflows has more than offset the outflows we saw from late Aug to late Sep.

- Elsewhere, flow trends were negative for offshore buying of local bonds, for the second straight week. The cumulative flow backdrop for this space has been close to flat in recent months though.

- Japan investors sold offshore bonds for the second straight week. Indeed, we have seen net selling four out of the last five weeks for this segment. Still, cumulative net buying is still positive going back to late Aug/early Sep. Global bond returns have stabilized in recent weeks and dipped post Wednesday's hawkish Fed 25bps cut.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Oct 24 | Prior Week |

| Foreign Buying Japan Stocks | 1344.2 | 752.6 |

| Foreign Buying Japan Bonds | -253.5 | -25.5 |

| Japan Buying Foreign Bonds | -351.4 | -664.4 |

| Japan Buying Foreign Stocks | -62.1 | -288.1 |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LNG: Gas Within Recent Ranges As Supplies Solid

European natural gas fell 2.1% to EUR 32.00 on Monday but is still up 1.2% in September and remains in the range that it has traded in this month (31.36/33.44) given uncertainties around the Russian outlook. It reached a high of EUR 32.43 before falling to EUR 31.95. Storage refilling ahead of the heating season has continued with it reaching 82.5% full. This and softer demand from China have kept gas prices subdued.

- Europe is looking to bring forward its plans to end Russian gas consumption by a year to end 2026. While pipeline flows are minimal, imports of Russian LNG have increased. With the war in Ukraine continuing, further sanctions seem likely with President Zelenskyy stating they could be announced this week.

- There have been minimal supply disruptions with Gulf gas rigs so far avoiding storms and Norwegian output returning as expected after scheduled maintenance.

- US gas rose 1.8% to $3.275 on Monday to be down 1.7% in September. It reached a monthly low of $3.055 on 23 September and has trended higher since then. There are forecasts for warmer weather in early October and thus expectations of increased cooling demand. NatGasWeather also said that there could be increased demand for LNG output.

- US lower-48 gas production was up 6.5% y/y on Monday while demand rose 4.6% y/y. Estimated flows to LNG export facilities rose 8.8% w/w, according to BNEF gas data.

- Kpler data is indicating that China’s LNG imports fell more than 20% y/y in September. However, it continues to take shipments from Russia’s sanctioned Arctic LNG 2 facility.

US STOCKS: S&P - Stalls Back Towards All-Time Highs

The S&P(ESZ5) overnight range was 6696.25 - 6736.00, SPX closed +0.26%, Asia is currently trading around 6708. The stock market stalled just ahead of its all-time highs as the market started to ask why a shutdown was good for equities ? This morning US futures have opened slightly lower on our open, E-minis(S&P) -0.10%, NQZ5 -0.10%. The stock market continues to look way overdone and is in what is supposed to be a difficult seasonal period, the last 2 weeks of September in particular. In saying that, if that was the extent of the pullback last week it was very shallow ! The market is clearly still in an uptrend and dips continue to be supported for now.

- Daily Chartbook on X: "Traditional measures show U.S. equity valuations are above average. Where they settle will depend on how the economic transformation underway plays out. We believe AI-led productivity gains could boost earnings growth." - @BlackRock

- Bloomberg - “S&P 500 Has a Proven Record of Resisting the Drag of Shutdowns. In past instances of either an actual or threatened shutdown, the S&P 500 did get hit momentarily. Yet any impact tends to be short-lived and has hardly stopped the index from eventually reaching all-time highs.”

- Unusual whales on X: “Global equities are likely to extend a rally into the year end given a resilient US economy, supportive valuations and a dovish pivot from the Fed, per Goldman Sachs.”

- Lance Roberts on X: “Returns in Q4 tend to be the strongest of the year. With professionals underweight, the return of buybacks, and strong momentum, a push higher into year-end will not be surprising.”

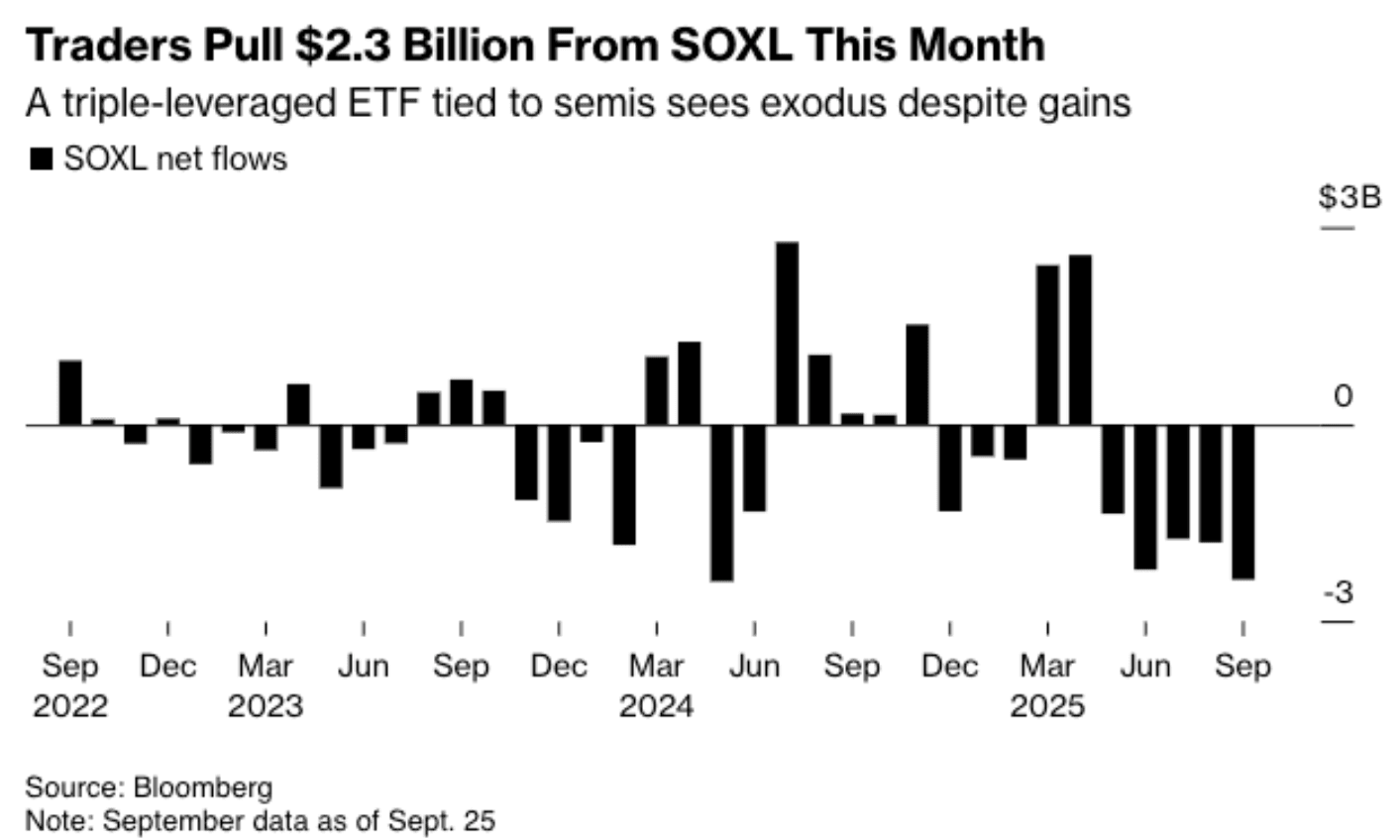

- Daily Chartbook on X: "Retail investors — often dismissed as the 'dumb money,' late to act and quick to overreact — have repeatedly been ahead of the curve this cycle ... Their current retreat from the market’s frothiest corners may again be a signal worth heeding." - @isabelletanlee @VildanaHajric. See Graph Below

Fig 1: Retail Taking Profit

Source: MNI - Market News/@dailychartbook/Bloomberg Finance L.P

US TSYS: Cash Open

TYZ5 is trading 112-17, up 0-00+ from its close.

- The US 2-year yield opens around 3.619%.

- The US 10-year yield opens around 4.141%.

- 10-Year yields drifted lower as the market prices in a US shutdown, I suspect buyers continue to be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week and if not then the ADP starts to take on a lot more relevance.

- MNI BRIEF: Fed's Williams-Making Meeting By Meeting Decisions. New York Fed President John Williams said Monday he is making monetary policy decisions on a meeting-by-meeting basis, adding that this month's rate cut made sense given rising risks to employment, and leaves monetary policy at still-restrictive levels.

- MNI US DATA: Dallas Fed Survey Unexpectedly Weakens As Respondents Cite Weak Demand. The Dallas Fed's Texas Manufacturing Outlook Survey printed on the weak side in September, with the headline general business activity index of -8.7 below the expected -1.0. That meant that the index unexpectedly deteriorated from the prior -1.8, the 2nd consecutive retracement after briefly hitting a 6-month high in July. The activity index suffered along with a combination of weak subindices: a decline in employment (lowest since April) and new orders suggesting contraction in demand with shipments also retreating, overall with "most pointing to notably slower growth than in August" per the report.

- Data/Events: FHFA House Price Index, S&P Cotality CS 20-City, MNI Chicago PMI, JOLTS Job Openings, Conf. Board Consumer Confidence, Dallas Fed Services Activity