ASIA STOCKS: New Highs For KOSPI : BOJ on Hold : JCI Back Above Key Level

As President Trump and Xi met in Korea, equity futures rose on hopes that easing trade tensions could be supportive of global growth going forward. South Korea announced a trade deal today that would result in $150bn of Korean investment in US shipbuilding, with a further $200 bn potential to follow. Korea agreed to buy significant amounts of US oil and gas which gave the KOSPI a further kick towards a new all time high. Elsewhere stocks in Japan were led by their tech sector following overnight positive news from Alphabet and Nvidia whilst the BOJ failed to surprise markets, keeping rates at 0.50%.

- The NIKKEI hit new highs of 51,561 on tech and BOJ hold and is up +0.50% today.

- The Hang Seng led China's major bourses with gains of 0.55% to 26,487, consolidating above the 20-day EMA of 26,175 whilst other major bourses were mixed

- The TAIEX only had limited follow on from the Tech sector new overnight, gaining just +0.22% despite up strongly to hit new highs.

- The KOSPI was buoyed by the trade deal and the uncertainty that it removed and rose +0.23% to another new high. The KOSPI is up now 19% over the last month, challenging valuations relative to bonds.

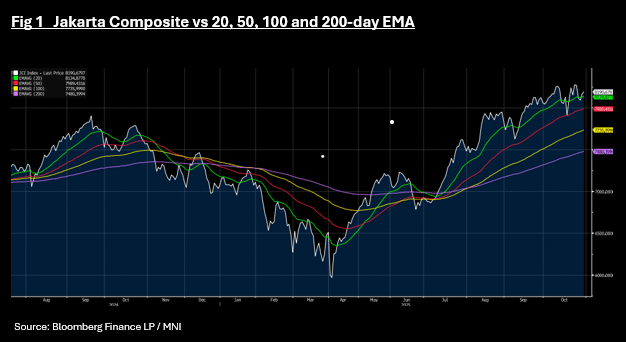

- The Jakarta Comp has now delivered two days of gains, to trade back above the 20-day EMA after dipping below as the NIFTY 50 opens having closed yesterday at a new high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

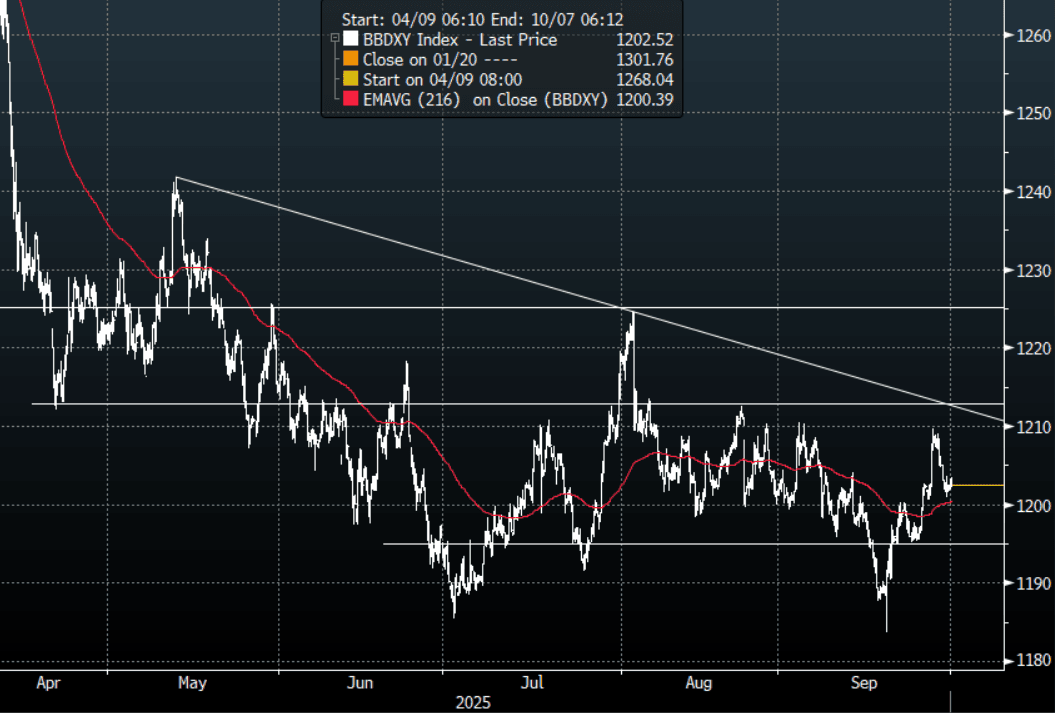

FOREX: Asia FX Wrap - BBDXY Holds Above 1200 For Now

The BBDXY has had a range of 1201.91 - 1203.39 in the Asia-Pac session; it is currently trading around 1202, +0.02%. The USD finally found some support back towards the 1200 area after being heavily sold on the looming shutdown. First support back towards the 1200 area and then 1195. Quarter-end for Asset managers likely to see some more USD selling to rebalance portfolios. I thought it would be a tough ask to see any big directional moves this week until the market gets a look at the Payroll number. With this data now at risk the ADP could take on a lot more relevance this week.

- EUR/USD - Asian range 1.1712 - 1.1732, Asia is currently trading 1.1720. The pair has drifted back above 1.1700, I suspect sellers could reemerge above 1.1750 initially. The deeper correction looks to have been put on hold for now as the focus turns toward the jobs numbers, just not sure which one.

- GBP/USD - Asian range 1.3421 - 1.3438, Asia is currently dealing around 1.3435. The pair could not break through its support around the 1.3300 area, price has bounced back into the range. The market should be looking for bounces to fade initially, first sell zone back towards the 1.3500 area.

- USD/CNH - Asian range 7.1246 - 7.1324, the USD/CNY fix printed 7.1055, Asia is currently dealing around 7.1310. The pair stalled toward 7.1500 and collapsed lower again very easily. The area just below 7.1000 has proved to be well supported recently so maybe we consolidate 7.09-7.16 for now.

- Cross asset : SPX -0.05%, Gold $3865, US 10-Year 4.14%, BBDXY 1202, Crude Oil $63.05

- Data/Events : Spain Current Account Balance, Germany Retail Sales/Unemployment Change/CPI, France Consumer Spending/CPI, Italy PPI/CPI/Industrial Sales

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Drifts Back Toward 0.5800

The NZD/USD had a range of 0.5774 - 0.5794 in the Asia-Pac session, going into the London open trading around 0.5790, +0.20%. The USD can’t find any friends and a potential shutdown has brought out all the bears again. The NZD broke through its pivotal 0.5800 support last week and has kept the pair under pressure trading heavily even with the USD falling. The first sell zone would be between the 0.5850/0.5900 area.

- MNI AU - NZ Business Activity Remained Soft But Price/Cost Components Up: ANZ business confidence for September was little changed at 49.6 while the activity outlook rose to 43.4 from 38.7. Past own activity rose 4 points to +5 signalling that growth is improving from Q2’s sharp contraction but remains lacklustre. Inflation expectations rose 0.1pp to 2.7% with a net 46% expecting to increase prices over the coming 3 months (+3pp) and an increase in costs. Employment compared to a year ago improved marginally but remained negative at -10.9, in line with other data signalling that the labour market is weak. The RBNZ is expected to ease at both its October and November meetings and monthly data pointing to continued soft growth are in line with this.

- "FONTERRA SEASON TO DATE NZ MILK COLLECTION RISES 3.2% Y/Y, FONTERRA AUG. NZ MILK COLLECTION RISES 2% Y/Y :FSF NZ" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5785(NZD1b), 0.5860(NZD332m), 0.5875(NZD372m). Upcoming Close Strikes : none - BBG

- CFTC Data of last week shows Asset Managers continuing to rebuild their short positions in the NZD, -18421(Last -11933). The Leveraged community don’t seem as convinced and reduced their own shorts, -2850(Last -5327).

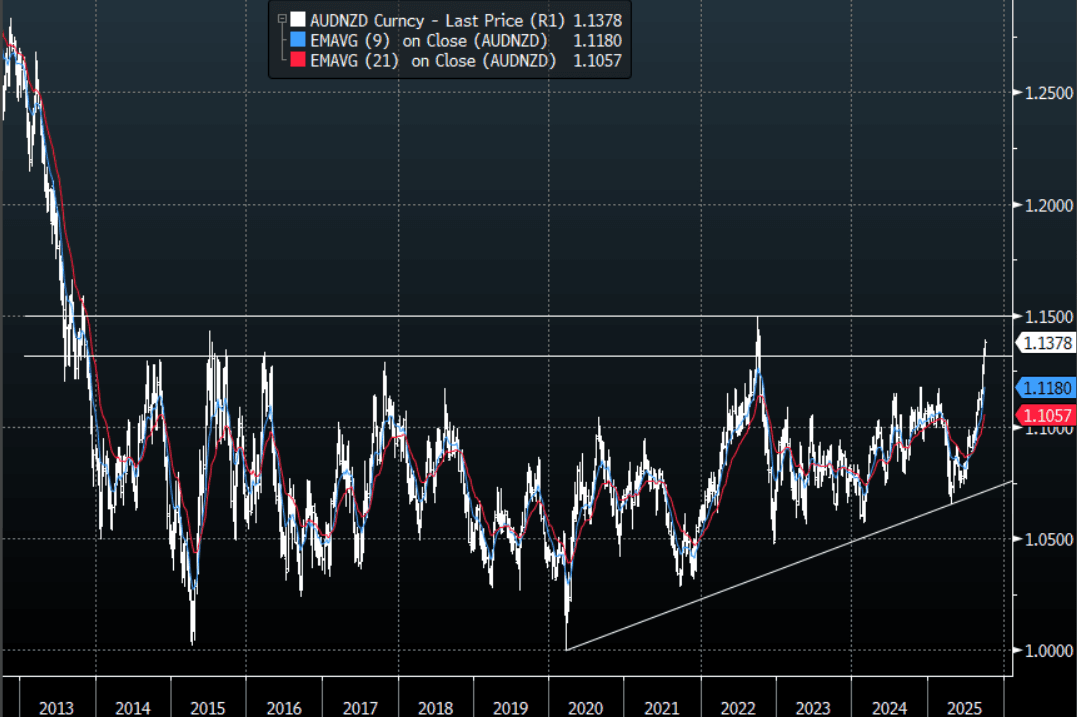

- AUD/NZD range for the session has been 1.1371 - 1.1392, currently trading around 1.1380. The Cross has broken above the multiple highs around the 1.1200 area and has accelerated up towards 1.1400. I would think this 1.1400/1.1500 would initially be met with sellers and expect some work to be done up here before another extension higher.

Fig 1: AUD/NZD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

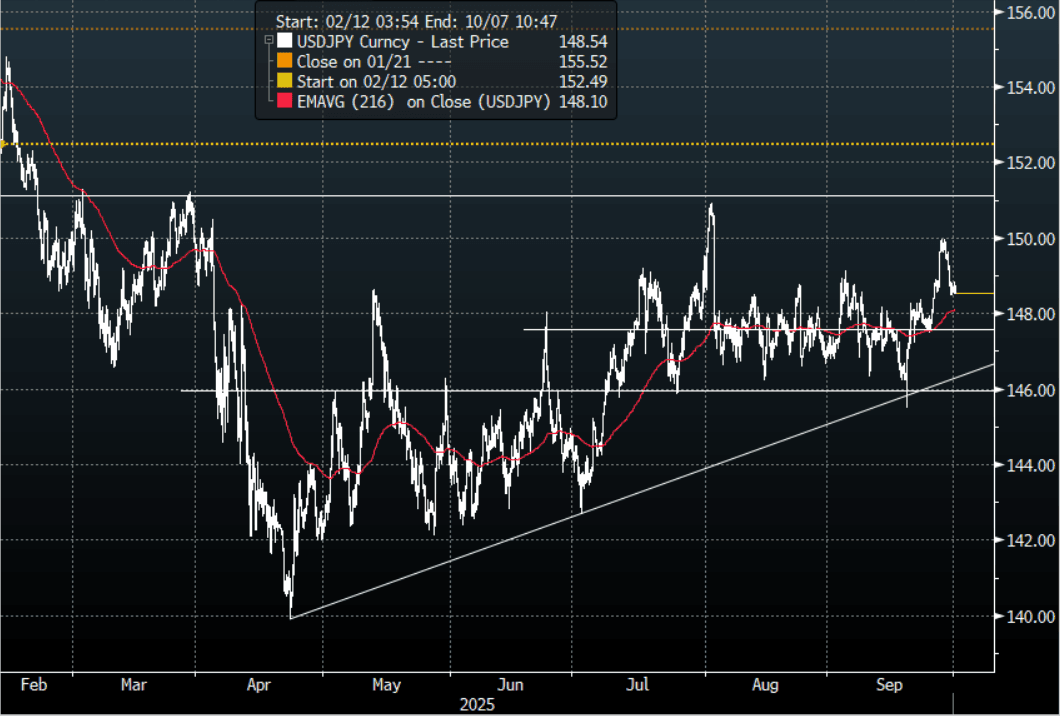

JPY: Asia Wrap - USD/JPY Holds Above 148.50 For Now

The USD/JPY range has been 148.50 - 148.84 in the Asia-Pac session, it is currently trading around 148.55, -0.05%. The USD has no friends as the sellers are quick to return on a potential US shutdown. Hawkish comments from the BOJ’s Noguchi yesterday gave USD/JPY an extra nudge lower, putting in a sharp rejection of the 150.00 area. The Payrolls data this week was to be critical so should we not get it due to a shutdown the ADP print could take on larger significance. Some demand has returned around 148.50 stalling the momentum lower, next support is back towards the 147.50/148.00 area.

- MNI: BOJ Opinions: Board Split Over Rate Hike, Inflation. Bank of Japan board members were split over whether to raise the policy rate at the September 18-19 meeting, with some calling for more data and others pushing for an increase, the summary of opinions released Tuesday showed.

- MNI: Japan Aug Factory Output Posts 2nd Straight Drop. Japan’s industrial output fell 1.2% m/m in August, marking a second straight decline after July’s 1.2% drop, as stronger automobile production was offset by weakness in electrical machinery and information and communications equipment, data from the Ministry of Economy, Trade and Industry showed Tuesday.

- "KATO: GOVT WILL AIM FOR BOTH FISCAL HEALTH, ECONOMIC RECOVERY, KOIZUMI CAN COUNTER MULTIPLE CHALLENGES INCL. INFLATION.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 148.00($876m). Upcoming Close Strikes : 146.00($1.14b Oct 3), 146.50($1.09b Oct 1) - BBG.

- CFTC data shows last week asset managers increased their JPY longs slightly +79262( Last +71162), leveraged funds though again used the dip to add to their short position as the support held, -634171(Last -58811). The diverging views amongst investors continue to build.

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P