OIL: Crude Dips As Trump-Xi Meeting Ends With No Announcement

Oil has been range trading during today’s APAC session as it waits for news following the meeting between Presidents Trump and Xi, which has ended. The lack of news at this point has driven prices lower. The market is also on hold ahead of Sunday’s OPEC meeting which is likely to see another 137kbd increase in the output target as it unwinds previous curbs but it is coming at a time of already elevated supply.

- WTI is down 0.5% to $60.19/bbl but has traded today between $60.05 and $60.45. It was around $60.40 before it was announced that Trump had boarded Air Force One. Brent is 0.3% lower (December contract) at $64.76, after reaching $64.96, but off the day’s trough at $64.51. The USD index is down 0.1%.

- Uncertainty is high for oil with the Fed outlook unclear given dissenters and lack of data, ongoing trade tensions, elevated supply and sanctions. Trump said that he may discuss China’s Russian oil purchases with Xi when they met today.

- Later the Fed’s Bowman gives pre-recorded remarks and Logan speaks at a bank funding conference. The ECB decision is expected to be on hold. Euro area Q3 GDP, EC October survey, German preliminary CPI & September unemployment print.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Continues To Rally As US Debt Ceiling Remains Unresolved

Gold has continued to rally during Tuesday’s APAC trading as the US currently appears no closer to a resolution to the debt ceiling impasse. The yellow metal made another new record high at $3867.25/oz today. It is currently up 0.8% to $3863.0 supported by safe-have flows while the US dollar and yields are little changed.

- The next level to watch is round number resistance at $3900.

- US President Trump met with party leaders to try and reach a deal to lift the debt ceiling but it ended without agreement. Apparently departments are looking at furloughing staff rather than redundancies if there is a government shutdown. US data could also be delayed, which would include Friday’s key September payrolls, which is expected to be subdued.

- Silver is 0.2% higher at $47.02 after reaching $47.122 earlier. Market tightness has boosted it over the month.

- Equities are mixed with the S&P e-mini flat, TAIEX up 1.3%, CSI 300 +0.2% but Hang Seng down 0.1%. Oil prices have continued to fall with WTI -0.6% to $63.07/bbl. Copper is up 0.3%.

- Later the Fed’s Jefferson, Collins, Goolsbee, Logan, ECB’s Lagarde, Elderson, Machado, Cipollone and BoE’s Mann, Lombardelli and Breeden speak. US July housing data, August JOLTS job openings, September MNI Chicago PMI and Conference Board consumer confidence as well as German August retail sales, unemployment and preliminary German/Italian September CPIs are released.

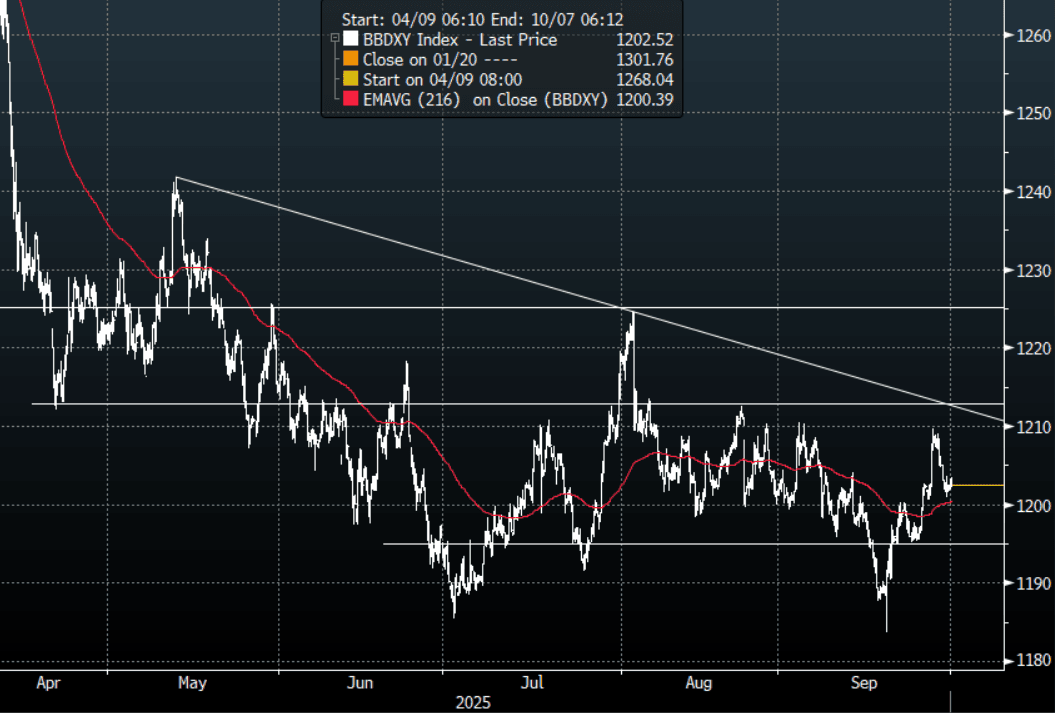

FOREX: Asia FX Wrap - BBDXY Holds Above 1200 For Now

The BBDXY has had a range of 1201.91 - 1203.39 in the Asia-Pac session; it is currently trading around 1202, +0.02%. The USD finally found some support back towards the 1200 area after being heavily sold on the looming shutdown. First support back towards the 1200 area and then 1195. Quarter-end for Asset managers likely to see some more USD selling to rebalance portfolios. I thought it would be a tough ask to see any big directional moves this week until the market gets a look at the Payroll number. With this data now at risk the ADP could take on a lot more relevance this week.

- EUR/USD - Asian range 1.1712 - 1.1732, Asia is currently trading 1.1720. The pair has drifted back above 1.1700, I suspect sellers could reemerge above 1.1750 initially. The deeper correction looks to have been put on hold for now as the focus turns toward the jobs numbers, just not sure which one.

- GBP/USD - Asian range 1.3421 - 1.3438, Asia is currently dealing around 1.3435. The pair could not break through its support around the 1.3300 area, price has bounced back into the range. The market should be looking for bounces to fade initially, first sell zone back towards the 1.3500 area.

- USD/CNH - Asian range 7.1246 - 7.1324, the USD/CNY fix printed 7.1055, Asia is currently dealing around 7.1310. The pair stalled toward 7.1500 and collapsed lower again very easily. The area just below 7.1000 has proved to be well supported recently so maybe we consolidate 7.09-7.16 for now.

- Cross asset : SPX -0.05%, Gold $3865, US 10-Year 4.14%, BBDXY 1202, Crude Oil $63.05

- Data/Events : Spain Current Account Balance, Germany Retail Sales/Unemployment Change/CPI, France Consumer Spending/CPI, Italy PPI/CPI/Industrial Sales

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Drifts Back Toward 0.5800

The NZD/USD had a range of 0.5774 - 0.5794 in the Asia-Pac session, going into the London open trading around 0.5790, +0.20%. The USD can’t find any friends and a potential shutdown has brought out all the bears again. The NZD broke through its pivotal 0.5800 support last week and has kept the pair under pressure trading heavily even with the USD falling. The first sell zone would be between the 0.5850/0.5900 area.

- MNI AU - NZ Business Activity Remained Soft But Price/Cost Components Up: ANZ business confidence for September was little changed at 49.6 while the activity outlook rose to 43.4 from 38.7. Past own activity rose 4 points to +5 signalling that growth is improving from Q2’s sharp contraction but remains lacklustre. Inflation expectations rose 0.1pp to 2.7% with a net 46% expecting to increase prices over the coming 3 months (+3pp) and an increase in costs. Employment compared to a year ago improved marginally but remained negative at -10.9, in line with other data signalling that the labour market is weak. The RBNZ is expected to ease at both its October and November meetings and monthly data pointing to continued soft growth are in line with this.

- "FONTERRA SEASON TO DATE NZ MILK COLLECTION RISES 3.2% Y/Y, FONTERRA AUG. NZ MILK COLLECTION RISES 2% Y/Y :FSF NZ" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5785(NZD1b), 0.5860(NZD332m), 0.5875(NZD372m). Upcoming Close Strikes : none - BBG

- CFTC Data of last week shows Asset Managers continuing to rebuild their short positions in the NZD, -18421(Last -11933). The Leveraged community don’t seem as convinced and reduced their own shorts, -2850(Last -5327).

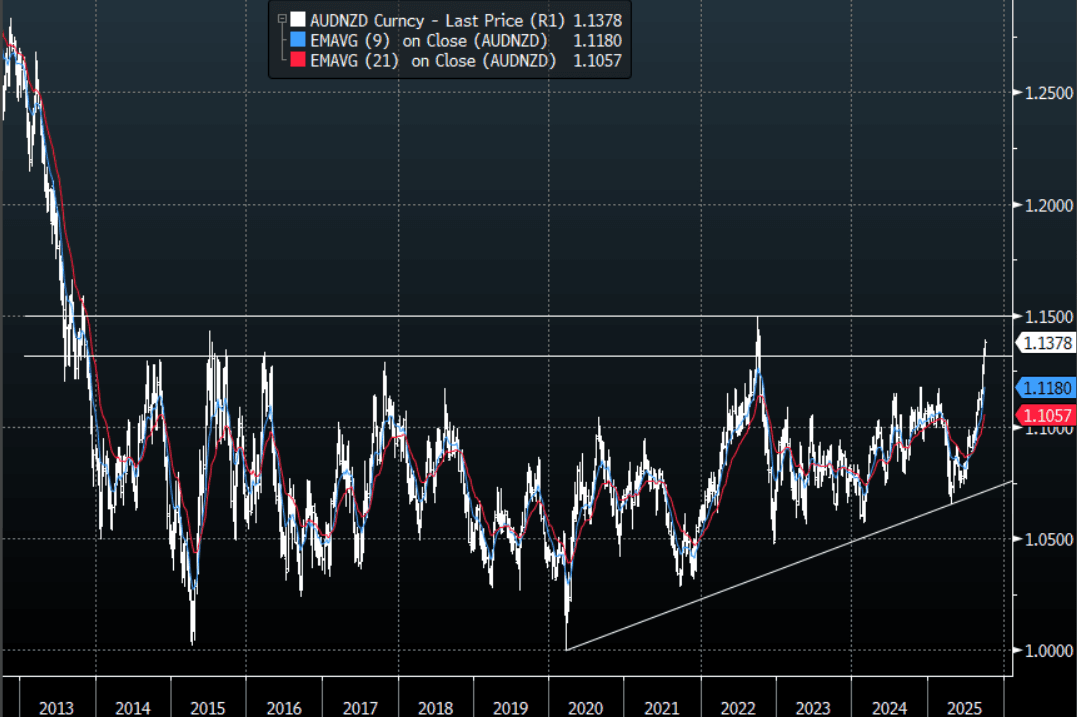

- AUD/NZD range for the session has been 1.1371 - 1.1392, currently trading around 1.1380. The Cross has broken above the multiple highs around the 1.1200 area and has accelerated up towards 1.1400. I would think this 1.1400/1.1500 would initially be met with sellers and expect some work to be done up here before another extension higher.

Fig 1: AUD/NZD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P