BOJ: On Hold With A 7-2 Vote, Commentary Suggests High Bar For Dec Hike

The BoJ left rates on hold as expected. Once again there were two dissenters, board members Takata and Tamura voted in favor of a rate hike but this viewpoint is not shared by the majority of the board, leaving the decision to hold rates steady at a 7-2 vote. There had been a focus point prior to the meeting that we may see another board member join the dissenting camp, but this hasn't materialized. This coupled with little change in the forecast projections, has left BoJ hawks with little to focus on. In turn, USD/JPY has bounced (back above 153.00, but still sub bull trigger at 153.27), while JGB futures are up from earlier lows and local stocks are firmer (NKY 225 up 0.60%).

- The forecast projections only saw minor adjustments, with core, ex energy, CPI nudged up to 2.0% for the 2026 financial year, from 1.9% prior. The 2025 and 2027 projections at 2.8% and 2.0% were unchanged respectively. The core CPI projects were all steady 2.8% for 2025 financial year and 1.8% for next and 2.0% for 2027.

- On growth, the current financial year projection was nudged up to 0.7% from 0.6%, while 2026 was unchanged at 0.7% and 2027 is at 1%.

- The central bank also noted inflation is likely to decelerate sub 2% in the first half of the 2026 financial year and that underlying inflation is likely to remain sluggish. On growth it said the economic risk balance for the next financial year is on the downside. This reflects likely slower offshore growth and the impact of trade policies.

- Still, it expects the price trend to be in line with the inflation target in the 2nd half of the outlook (no change on this point) and retains its bias to raise rates if the outlook is realized.

- This backdrop suggests the bar is quite high for the core board viewpoint to shift to a hike by the Dec meeting.

- We now await Ueda' press conference in a few hours (3:30pm local time).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

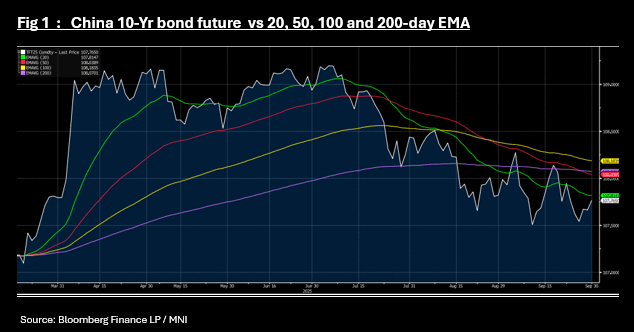

CHINA: Bond Futures Rise in Morning Trade

- After doing very little Monday, bond futures have started Tuesday off with a rally.

- The 10-Yr is up +0.10 at 107.76 and is near to the 20-day EMA of 107.81

- The 2-Yr future is up +0.01 at 102.35 and is near the 20-day EMA of 102.36.

- The 10-Yr government bond is at 1.88%

JGBS: Bull-Flattener Holding At Lunch, BOJ SOO: No Clear Hint For Oct Hike

At the Tokyo lunch break, JGB futures are stronger, +9 compared to settlement levels.

- MNI - Bank of Japan board members were split over whether to raise the policy rate at the September 18-19 meeting, with some calling for more data and others pushing for an increase, the summary of opinions released Tuesday showed. The disclosures gave no clear signal of an October move, with most members aside from Naoki Tamura and Hajime Takata - who dissented and proposed a hike - seeing little urgency.

- MNI - Japan's industrial output fell 1.2% m/m in August, marking a second straight decline after July's 1.2% drop, as stronger automobile production was offset by weakness in electrical machinery and information and communications equipment, data from the Ministry of Economy, Trade and Industry showed Tuesday.

- Industrial output is a key indicator for BOJ economists tracking the pace of Japan's modest recovery as it reflects both external and domestic demand.

- Cash US tsys are slightly cheaper, with a steepening bias, in today's Asia-Pac session after yesterday's bull-flattener.

- Cash JGBs have bull-flattened across benchmarks, with yields flat to 3bps richer. The benchmark 10-year yield is 1.2bps lower at 1.631% versus the cycle high of 1.670%.

- Swap rates are little changed.

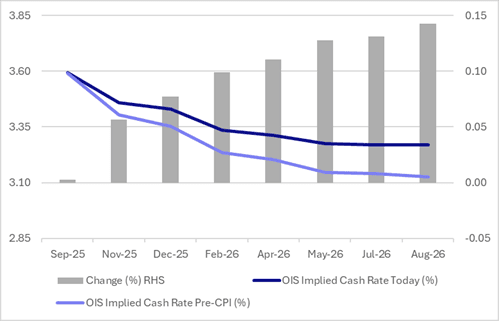

STIR: RBA Dated OIS Sharply Firmer Than August CPI Levels

Ahead of today’s RBA policy decision, RBA-dated OIS pricing is sharply firmer across 2026 meetings versus last Wednesday’s CPI levels.

- The headline August CPI print was 3.0%y/y, against a 2.9% market consensus and 2.8% July outcome. The trimmed mean was 2.6% y/y, after printing 2.7% in July.

- The Q3 CPI print is out on Oct 29, with the RBA outcome on Nov 4.

- A 25bp rate cut today is given a 3% probability, with a cumulative 17bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Today Vs. Pre-CPI

Source: Bloomberg Finance LP / MNI