BONDS: NZGBS: Yields Higher But off Best Levels, 2/10s Back Under +150bps

NZGB yields are holding firmer, but are away from session highs. We are around 2.5-4.5bps higher, with the belly of the curve leading in yield terms. Moving off session highs may have been helped by a slightly weaker US Tsy lead so far today, although Tsy yield losses are not much beyond 1bps at this stage. The 2yr is around 2.60%, so not breaking above 20-day EMA resistance yet. The 10yr is around 4.08%, but did get beyond 4.14% earlier. The 2/10s curve is off earlier highs, last +148bps, after printing +152bps earlier.

- The 2yr swap rate, which has arguably led the firmer yield tone in NZ, is off nearly 4bps to 2.42%. We are still some distance from recent lows near 2.25%.

- On the data front today, ANZ business confidence rose to its highest since February at 58.1 in October. The RBNZ cut rates 50bp to 2.5% on 8 October with more signalled, but ANZ doesn’t believe it boosted sentiment. However, interest-sensitive sectors are outperforming. The activity outlook was more subdued but still rose 1.2 points to 44.6. Inflation expectations ticked higher but pricing intentions were lower. The RBNZ is likely to cut rates again on 26 November and the ANZ survey confirmed that while the recovery continued it remains soft and uneven.

- Nov easing is priced around 90% for a 25bps cut by the market so away from recent extremes of beyond 100%. 2026 implied rate levels have edged up, but this is likely spill over from the Fed overnight.

- Tomorrow, we get the Oct ANZ consumer confidence print.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: RBNZ To Eye 2% OCR Level - Ex Assistant Governor

A former RBNZ Assistant Governor shares his OCR outlook.

On MNI Policy MainWire now, for more details please contact sales@marketnews.com

US TSYS: Yields Relatively Unchanged In A Very Quiet session

The TYZ5 range has been 112-16 to 112-17+ during the Asia-Pacific session. It last changed hands at 112-17, up 0-00+ from the previous close.

- The US 2-year yield is trading 3.619%.

- The US 10-year yield is trading around 4.139%.

- 10-Year yields drifted lower as the market prices in a US shutdown, I suspect buyers continue to be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week and if not then the ADP starts to take on a lot more relevance.

- Bloomberg - "JD Vance said he believes the US government is heading for a shutdown, blaming Democrats for refusing to approve a short-term spending bill. Donald Trump and top congressional leaders failed to reach an agreement in a meeting before the Oct. 1 deadline."

- MacroEdge on X: “Government shutdown odds surge as Vance leaves meeting saying ‘we’re headed to a shutdown’ & GOP lacks votes to pass funding bill.” See Polymarket Odds Below.

- “Markets aren’t rushing to reduce risk exposure, having seen plenty of US shutdown threats before, Vishnu Varathan, head of macro research for Mizuho Securities, writes in a note” - BBG

Data/Events: FHFA House Price Index, S&P Cotality CS 20-City, MNI Chicago PMI, JOLTS Job Openings, Conf. Board Consumer Confidence, Dallas Fed Services Activity

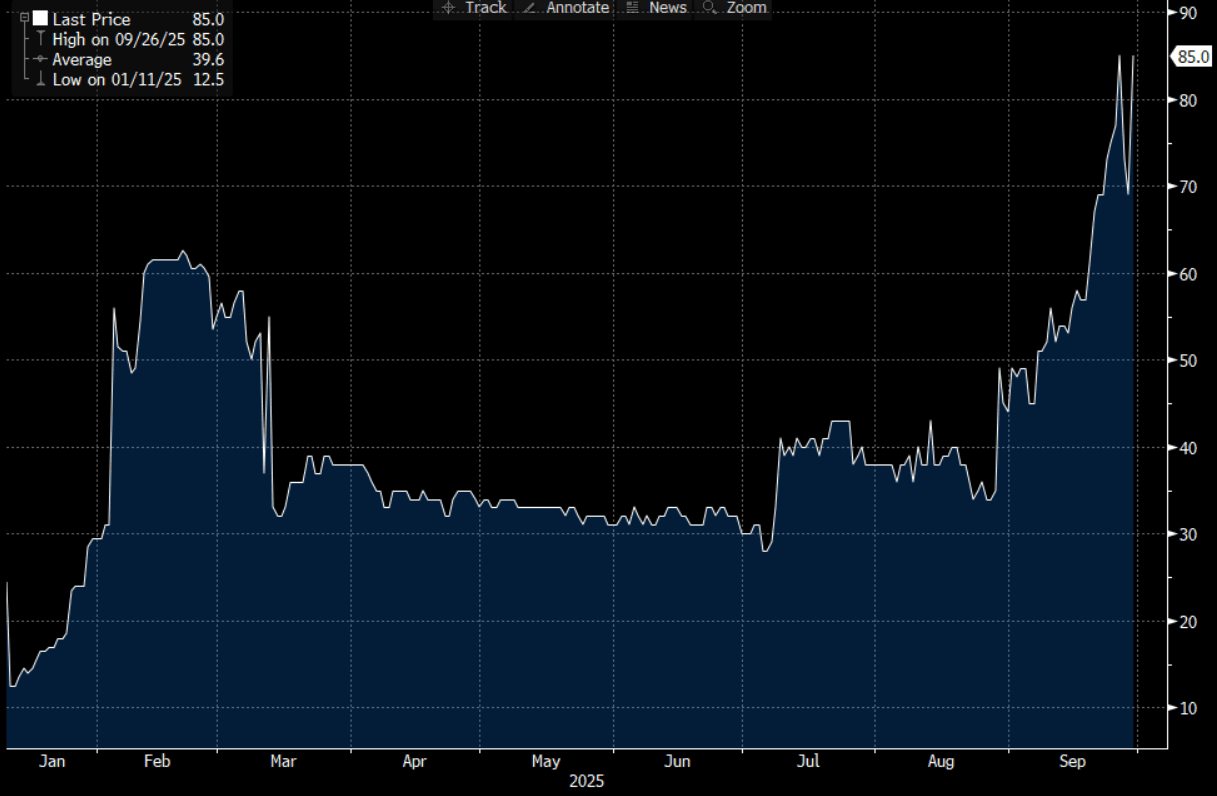

Fig 1: Polymarket Odds Of A US Shutdown

Source: MNI - Market News/Bloomberg Finance L.P

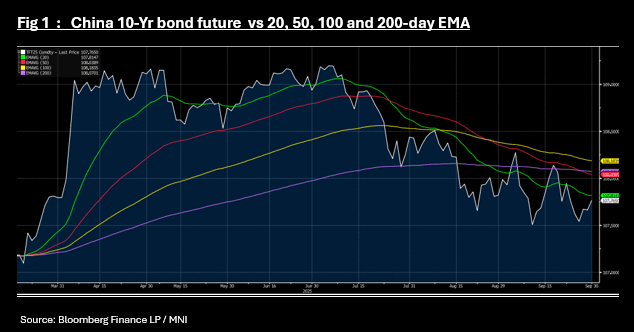

CHINA: Bond Futures Rise in Morning Trade

- After doing very little Monday, bond futures have started Tuesday off with a rally.

- The 10-Yr is up +0.10 at 107.76 and is near to the 20-day EMA of 107.81

- The 2-Yr future is up +0.01 at 102.35 and is near the 20-day EMA of 102.36.

- The 10-Yr government bond is at 1.88%