MNI US OPEN - Zelenskyy Says Ukraine Won’t Give Up Donbas

EXECUTIVE SUMMARY

- US EMBEDS TRACKERS IN AI CHIP SHIPMENTS TO CATCH DIVERSIONS TO CHINA: RTRS

- BESSENT DISMISSES CHINA INVESTING IN US AS PART OF A TRADE DEAL

- ZELENSKIY SAYS UKRAINE WON’T GIVE UP DONBAS REGION TO RUSSIA

- GLOBAL OIL MARKETS FACE RECORD SUPPLY GLUT NEXT YEAR, IEA SAYS

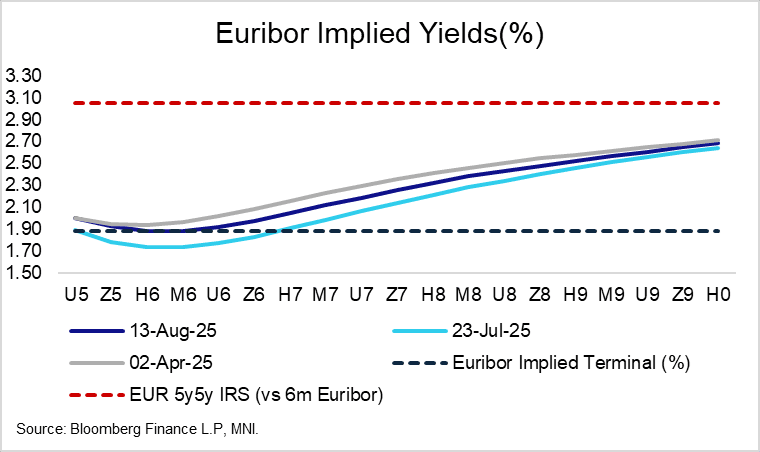

Figure 1: Euribor implied terminal rate at highest since April 2

NEWS

US/CHINA (RTRS): US Embeds Trackers in AI Chip Shipments to Catch Diversions to China, Sources Say

U.S. authorities have secretly placed location tracking devices in targeted shipments of advanced chips they see as being at high risk of illegal diversion to China, according to two people with direct knowledge of the previously unreported law enforcement tactic. The measures aim to detect AI chips being diverted to destinations which are under U.S. export restrictions, and apply only to select shipments under investigation, the people said.

US/CHINA (BBG): Bessent Dismisses China Investing in US as Part of a Trade Deal

Treasury Secretary Scott Bessent dismissed the possibility that Chinese investments in the US could be part of any trade pact, comments that narrow the options for the two sides to resolve their running dispute. When asked if China could make pledges worth billions of dollars like Japan, South Korea and the EU have as part of their trade agreements, Bessent said “my sense is no because a lot of the buyout or the funds from the buyout are going to go to critical industries that we need to reshore and a lot of those need to be reshored away from China.”

US/JAPAN (BBG): Japan’s Investment in $550 Billion US Fund May Be More Than 2%

The rate of actual Japanese investment forming part of a $550 billion US fund could be higher than the 1-2% initially cited, Japan’s top negotiator Ryosei Akazawa said in a live television interview on Wednesday. During the interview with TV Asahi, he pointed out that the US may not be able to get Japan’s investment unless they keep their promises, as he explained the details of the fund which forms a crucial pillar of the Japan-US trade deal agreed late July. Japan had said that the bulk of the $550 billion US fund will be loans and loan guarantees, with only 1% to 2% deployed as investment.

UKRAINE (BBG): Zelenskiy Says Ukraine Won’t Give Up Donbas Region to Russia

Ukrainian President Volodymyr Zelenskiy said he won’t cede the eastern region of Donbas to Russia and pushed for Kyiv to be included in talks as the US and Russian leaders prepare to meet on Friday. Vladimir Putin is demanding that Ukraine give up the Donetsk and Luhansk regions that together form Donbas as a condition to unlock a ceasefire and enter negotiations over a longer-term peace accord.

EU/CHINA (BBG): China Sanctions Two EU Banks, Hitting Back at Europe’s Moves

China sanctioned a pair of banks in the EU, fulfilling a promise to retaliate after the bloc targeted some Chinese lenders over Russia’s invasion of Ukraine. China included UAB Urbo Bankas and AB Mano Bankas in its countermeasure list, the Ministry of Commerce said in a statement on Wednesday. The move bans organizations and individuals in China from transactions, cooperation and other activities with the institutions. In a separate statement, the ministry said it hoped the EU would cherish its relationship with China, correct its wrongdoing and stop harming the nation’s interests.

CHINA/INDIA (BBG): China and India Rebuild Ties After Modi’s Rupture With Trump

India and China are restoring economic links strained by a deadly 2020 border clash, the latest sign Prime Minister Narendra Modi is drawing closer to the BRICS countries after US President Donald Trump hit the South Asian nation with a 50% tariff. Modi’s latest move is to resume direct flights with China as soon as next month, said people familiar with the negotiations who asked for anonymity to discuss private matters. The deal could be formally announced when Modi is expected to head to China for the first time in seven years and meet leader Xi Jinping at the Shanghai Cooperation Organisation held in Tianjin from Aug. 31, the people said.

INDIA/RUSSIA (MNI): Foreign Ministers to Meet 21 Aug as Moscow & New Delhi Boost Defence Ties

Russia's Foreign Ministry has confirmed that Foreign Minister Sergey Lavrov will host India's Minister of External Affairs S. Jaishankar in Moscow on 21 August for bilateral talks. Since the imposition of 25% 'reciprocal' tariffs by the US on 7 August, and the threat of an additional 25% tariff in response to India's purchases of Russian oil from 28 August, India has notably ramped up its diplomatic relations with both Russia and China

OIL (BBG): Global Oil Markets Face Record Supply Glut Next Year, IEA Says

Global oil markets are on track for a record surplus next year as demand growth slows and supplies swell, the International Energy Agency said. Oil inventories will accumulate at a rate of 2.96 million barrels a day, surpassing even the average buildup during the pandemic year of 2020, data from the IEA’s monthly report showed. World oil demand this year and next is growing at less than half the pace seen in 2023.

THAILAND (BBG): Thailand Cuts Key Rate, Braces for Protracted Growth Slowdown

The Bank of Thailand cut its key interest rate and signaled it will remain accommodative as higher US tariffs risk setting off a prolonged period of economic weakness. The central bank’s Monetary Policy Committee voted unanimously Wednesday to cut the one-day repurchase rate by 25 basis points to 1.5%, as predicted by 14 of 23 economists surveyed by Bloomberg. The rest forecast no change.

TURKEY (BBG): Jailed Istanbul Mayor Is Ready to Back Others Against Erdogan

Turkish President Recep Tayyip Erdogan’s strongest challenger is open to endorsing an alternative candidate if he’s prevented from contesting the next presidential election. Istanbul Mayor Ekrem Imamoglu, who has been in jail for almost five months, said “democratic legitimacy” was at stake. While he still hoped to represent the opposition alliance it was “not the time for hesitation,” he said in his first interview with foreign media since his March arrest.

DATA

SPAIN DATA (MNI): Final July HICP Confirms Flash, Airfares Push Up Core

- SPAIN JUL HICP -0.3% M/M, +2.7% Y/Y

Spanish final July HICP confirmed flash estimates at 2.70% Y/Y (vs 2.27% prior), while the monthly reading was revised up a rounded tenth to -0.3% (-0.34% unrounded, vs -0.4% flash). Excluding energy and unprocessed foods, HICP accelerated a touch to 2.34% Y/Y (vs 2.22% prior). As indicated in the flash release, there was a rise in electricity inflation (17.30% Y/Y vs 9.00% prior) which pulled the energy component higher in July. Energy HICP was 2.97% Y/Y (vs -0.77% prior).

SWEDEN DATA (MNI): Unemployment Claims Data Indicates Labour Market Slack Still Growing

The Swedish seasonally adjusted unemployment claims rate from the Public Employment Service (PES) was steady at 7.1% in July. This is the highest level since December 2021, and combined with another Y/Y fall in vacancies, continues to indicate slack is building in the labour market. Vacancies fell 22% Y/Y in July (vs -13% in June, -24% in May), bringing the vacancies to unemployment claims ratio down to 0.20, the lowest since early 2021.

CHINA JAN-JULY TSF CNY23.99 TRLN VS MEDIAN CNY24.28 TRLN (MNI)

CHINA JAN-JULY NEW LOANS CNY12.87 TRLN VS MEDIAN CNY13.27 TRLN (MNI)

CHINA END-JULY M2 +8.8% Y/Y VS MEDIAN +8.3%; END-JUNE +8.3% (MNI)

CHINA END-JULY M1 +5.6% Y/Y VS +4.6% Y/Y END-JUNE (MNI)

CHINA END-JULY M0 +11.8% Y/Y VS +12.0% Y/Y END-JUNE (MNI)

JAPAN DATA (MNI): Japan July CGPI Rises 2.6% Y/Y; Import Price Drops

- JAPAN JULY CORP GOODS PRICE INDEX +2.6% Y/Y; JUNE UNREV

- JAPAN JULY CORP GOODS PRICE INDEX +0.2% M/M; JUNE REV -0.1%

Japan’s corporate goods price index (CGPI) rose 2.6% y/y in July, easing from June’s unrevised 2.9%, while import prices posted a sixth straight decline, Bank of Japan data showed Wednesday. Price gains were weighed by slower increases in beverages and foods (+4.2% vs +4.5%) and a drop in electric power, gas and water (-0.1% vs +3.2%). The CGPI rose 0.2% in July after a 0.1% fall in June, marking the first increase in three months.

AUSTRALIA DATA (MNI): Aussie Wages Rise 0.8% Q/Q in Q2

The Wage Price Index rose 0.8% q/q in Q2, in line with expectations, and 3.4% y/y – 10 basis points above market forecasts and unchanged from Q1, Australian Bureau of Statistics data showed Wednesday. “Annual wage growth to the June quarter 2025 was unchanged from the 3.4% rise seen in the March quarter 2025 but was down from the 4.1% growth at the same time last year,” said Michelle Marquardt, head of prices statistics at the ABS. “The share of wage changes greater than 4% has declined since this time last year. The smaller proportion of jobs with larger wage increases has contributed to lower overall wage growth.”

FOREX: Greenback Through Support, GBP Still Primary Beneficiary

- The greenback is softer against all others in G10, prompting the USD Index to fall for a second session. The price is now through last week's lows of 97.945 further erasing the rally posted off the late July low. Yesterday's CPI print remains the primary driver here, as the data cleared the last hurdle to the Fed resuming an easing cycle from September. OIS markets are now effectively fully priced for a cut, with more than another 25bps cut set to follow before year-end.

- The resultant USD weakness has aided recent rallies in the major pairs. GBP remains a key beneficiary here as the recent hawkish shift at the BoE further contrasts with the Fed. GBP/USD is now cleared of the 50-dma and appears to be building a base toward 1.3589, the mid-July highs. Clearance here would further firm the S/T outlook and keeps the YTD cycle highs in consideration across the medium-term - last traded back at 1.3789 on July 1st.

- EUR/NZD trades under pressure, with NZD outperformance across the board. The cross is fading off the monthly August of 1.9680. Further weakness through 1.9525 would be a bearish signal, and go further in erasing the rally posted at the beginning of this month. Moves come ahead of the RBNZ rate decision set for next week, with a further 25bps rate cut largely expected.

- Focus for the duration of the session remains on the speaker schedule, with data releases sparse. Fed's Barkin, Goolsbee and Bostic are all set to speak - with markets looking to complete the expected layout of votes into September after Fed nominee Miran spoke earlier this week.

EGBS: Bunds Retrace Yesterday Afternoon’s Sell-off; Curve Bull Flattens

Bund futures are +51 ticks at 129.62, rallying on improved volumes and fully retracing yesterday afternoon’s selloff. Initial resistance is 129.83. Much like yesterday’s price action, there hasn’t been a clear driver to note, with strength coming despite a 0.7% rally in European equities and impending 10-year Bund supply.

- The German curve has bull flattened, with 30-year yields down 5.5bps. 10s30s closed at 55bps yesterday, the steepest since June 2021. The spread is currently back at 54.4bps. Bull flattening on the cash bond curve has translated to outperformance for long end swap spreads & ASWs.

- European equity strength promotes peripheral and semi-core EGB/Bund spread tightening, with the 10-year BTP/Bund spread notably 1.5bps narrower at 77bps (tightest since 2010). A persistent pullback in EUR rates vol since the April tariff-induced volatility episode has been a key driver of BTP spread tightening in the last few months.

- Today’s regional data saw German and Spanish final July HICP confirm flash estimates. The data did not move markets.

GILTS: Early Bull Flattening Holds

Gilts have rallied alongside global peers, reversing yesterday’s afternoon sell off, but remain softer than late Monday levels across much of the curve in the wake of yesterday’s labour market report.

- Weaker oil prices have provided some support today.

- Others have pointed to late Tuesday comments from U.S. Tsy Sec Bessent, suggesting the Fed should be open to a 50bp cut, although you would expect bull steepening on the curve if that was a meaningful driver, as opposed to the bull flattening seen today.

- Futures trade as high as 92.00 before fading back to 91.90.

- Bears have countered recent bullish technical developments.

- They look to yesterday’s low (91.51) as their first target, which protects the Aug 1 low (91.44) and July 18 low/bear trigger (91.08).

- Conversely, bulls need to close yesterday’s opening gap lower (~92.25) before switching focus higher.

- Yields 2-3bp lower across the curve, modest flattening noted.

- Fiscal issues continue to dominate local headlines. Guardian sources have reported that “the Treasury is looking at ways to raise more money from inheritance tax amid growing pressure on the country’s finances ahead of the autumn budget”.

- Curve steepening risks remain intact, albeit with crowded positioning and a more activist approach from policymakers when it comes to managing spikes higher in long end yields posing risks to that idea.

- BoE pricing steady, showing 16bp of easing through year-end, next cut fully discounted come the end of the Feb ’26 MPC.

- Little of note on the UK calendar today, with monthly economic activity and Q2 GDP readings due tomorrow.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.968 | +0.1 |

Nov-25 | 3.863 | -10.4 |

Dec-25 | 3.804 | -16.3 |

Feb-26 | 3.700 | -26.7 |

Mar-26 | 3.653 | -31.4 |

Apr-26 | 3.571 | -39.6 |

EQUITIES: E-Mini S&P Trading at Fresh Cycle High

The bounce off post-NFP lows in global equity indices has held, with the Eurostoxx 50 future still above the 50-day EMA. Additional strength refocuses attention on 5486.00, the May 20 high. To the downside, recent impulsive weakness did result in a temporary breach of the bear trigger - this makes the April 30 hi/lo range at 5078-5138 the area of downside interest. E-mini S&P prices recovered well Friday, meaning the bulk of the bounce off the NFP low is holding firm, keeping the underlying uptrend intact. The index holds above support at the 20-day EMA, at 6371.43 and is at a fresh cycle high. Through recent phases of weakness, the 50-day EMA at 6249.46, has held as support - and will be important on any intraday declines. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, leaving key short-term resistance and the bull trigger at 6468.50, the Jul 31 high.

- Japan's NIKKEI closed higher by 556.5 pts or +1.3% at 43274.67 and the TOPIX ended 25.54 pts higher or +0.83% at 3091.91.

- Elsewhere, in China the SHANGHAI closed higher by 17.547 pts or +0.48% at 3683.465 and the HANG SENG ended 643.99 pts higher or +2.58% at 25613.67.

- Across Europe, Germany's DAX trades higher by 186.73 pts or +0.78% at 24210.64, FTSE 100 higher by 14.64 pts or +0.16% at 9162.17, CAC 40 up 31.86 pts or +0.41% at 7785.39 and Euro Stoxx 50 up 42.05 pts or +0.79% at 5378.2.

- Dow Jones mini up 86 pts or +0.19% at 44644, S&P 500 mini up 11 pts or +0.17% at 6479.5, NASDAQ mini up 60.25 pts or +0.25% at 23998.

Time: 10:00 BST

COMMODITIES: WTI Futures Remain Weak After Break of Bear Trigger

WTI futures traded poorly Friday, cracking the 50-day EMA and piercing the bear trigger. This keeps S/T momentum pointed lower. The clear break exposes $58.17, the May 30 low. Gains early last week marked an extension of a corrective cycle - which may now have concluded. $69.41 marks the 50.0% retracement of the Jun 23-24 downleg - an important level. A continuation higher would open $70.96 next, the 61.8% retracement point. Gold traded lower at the start of the week, but last week's strength returned prices toward the top-end of the recent range and supports the view that short-term weakness is corrective - for now - and a bull cycle that started Jun 30 remains intact. However, the yellow metal is within close proximity to support at $3334.75, the 50-day EMA. A clear break of this level continues to signal scope for a deeper retracement and exposes the next key support at $3248.7, the Jun 30 low. Key near-term resistance is $3439.0, the Jul 23 high.

- WTI Crude down $0.61 or -0.97% at $62.56

- Natural Gas down $0 or -0.04% at $2.807

- Gold spot up $12.28 or +0.37% at $3360.53

- Copper down $0.3 or -0.07% at $458.25

- Silver up $0.58 or +1.53% at $38.507

- Platinum up $5.85 or +0.44% at $1349.45

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 13/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 13/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 13/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 13/08/2025 | 1700/1300 | Chicago Fed's Austan Goolsbee | ||

| 13/08/2025 | 1730/1330 | Atlanta Fed's Raphael Bostic | ||

| 14/08/2025 | - | NorgesBank Meeting | ||

| 14/08/2025 | 0130/1130 | *** | Labor Force Survey | |

| 14/08/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 14/08/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/08/2025 | 0600/0700 | ** | Trade Balance | |

| 14/08/2025 | 0600/0700 | ** | Index of Services | |

| 14/08/2025 | 0600/0700 | ** | Index of Production | |

| 14/08/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 14/08/2025 | 0600/0700 | *** | GDP First Estimate | |

| 14/08/2025 | 0645/0845 | *** | HICP (f) | |

| 14/08/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 14/08/2025 | 0900/1100 | ** | Industrial Production | |

| 14/08/2025 | 0900/1100 | *** | GDP (p) | |

| 14/08/2025 | 0900/1100 | * | Employment | |

| 14/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 14/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 14/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 14/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 14/08/2025 | 1800/1400 | Richmond Fed's Tom Barkin |