EGBS: Bunds Retrace Yesterday Afternoon’s Sell-off; Curve Bull Flattens

Bund futures are +51 ticks at 129.62, rallying on improved volumes and fully retracing yesterday afternoon’s selloff. Initial resistance is 129.83. Much like yesterday’s price action, there hasn’t been a clear driver to note, with strength coming despite a 0.7% rally in European equities and impending 10-year Bund supply.

- The German curve has bull flattened, with 30-year yields down 5.5bps. 10s30s closed at 55bps yesterday, the steepest since June 2021. The spread is currently back at 54.4bps. Bull flattening on the cash bond curve has translated to outperformance for long end swap spreads & ASWs.

- European equity strength promotes peripheral and semi-core EGB/Bund spread tightening, with the 10-year BTP/Bund spread notably 1.5bps narrower at 77bps (tightest since 2010). A persistent pullback in EUR rates vol since the April tariff-induced volatility episode has been a key driver of BTP spread tightening in the last few months.

- Today’s regional data saw German and Spanish final July HICP confirm flash estimates. The data did not move markets.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: EUR and MXN Unfazed by Latest Global Tariff Developments

- Despite President Trump threatening to impose 30% tariffs on the EU and Mexico, both the Euro and the Mexican peso have taken the news in their stride as markets remain cautiously optimistic that more lenient deals may be struck before the August 01 deadline. These limited reactions, and the lack of data on Monday keeps the dollar index within close proximity to Friday’s close.

- For EUR specifically, the brief bout of initial weakness did prompt a fresh pullback low at 1.1651 and notably, the 20-day EMA has been pierced. However, the lack of follow through shows that these shallow dips remain corrective, keeping bullish sentiment firmly intact for now. The July 01 high of 1.1829 remains the bull trigger for the pair.

- In similar vein, the USDMXN trend remains bearish, reinforced by fresh cycle lows for the pair last week. Potential is seen for a bearish extension towards 18.4302, the Aug 01 low.

- Elsewhere in G10, the likes of AUD and NZD are both underperforming in G10, however, it’s the Kiwi’s relative weakness that is helping AUDNZD extend its most recent upswing. The cross looks set to extend its winning streak to six consecutive sessions, shifting the upside target to 1.1032, the April 01 high.

- Tuesday’s data calendar is stacked with China activity figures kicking things off. The focus will then swiftly turn to US and Canadian inflation data, final inputs before both the Fed and BOC decisions on July 30. We will also have the beginning of quarterly earnings season with financials the usual early focus.

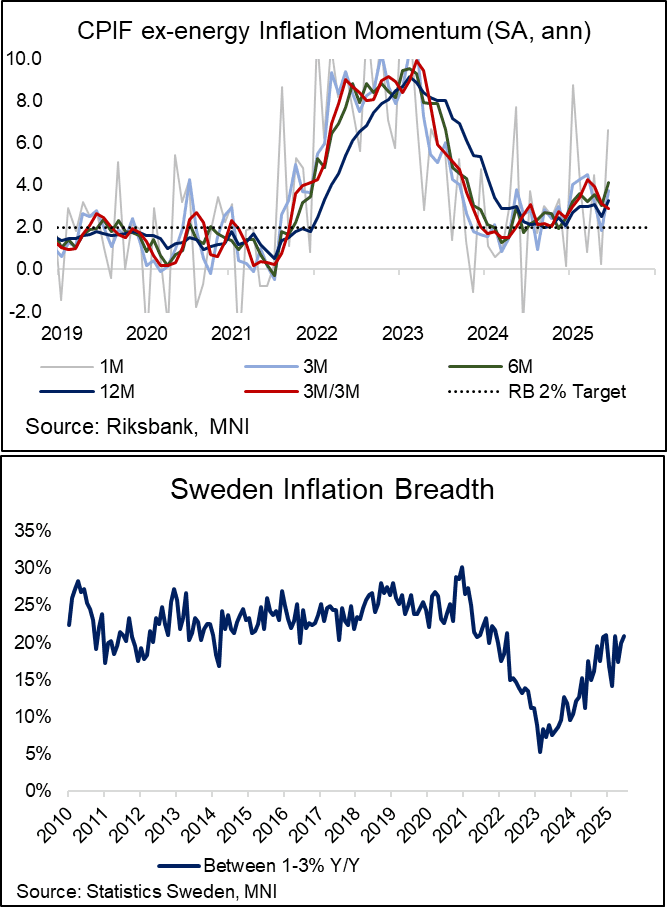

SWEDEN: 3m/3m Inflation Momentum Eases In June Despite Upside Surprise

Swedish seasonally adjusted core inflation momentum eased in June despite the NSA upside surprise to the Riksbank’s June MPR projection. While the chance of an August Riksbank cut has certainly fallen following the print, it cannot be fully ruled out yet. There is still another inflation print due on August 7 (flash, final on 14th) before the August 20 decision and even then, weak growth data may tilt the Executive Board in favour of further easing.

- MNI’s 3m/3m seasonally adjusted annualised inflation measure fell below 3% for the first time this year at 2.90% (vs 3.14% prior). However, other annualised seasonally adjusted measures did move higher alongside spot NSA rates.

- Splitting apart CPIF ex-energy, we calculate 3m/3m services momentum little changed at 2.75% (vs 2.77% prior), while core goods momentum was weak at -0.41% (vs 0.20% prior). Core goods momentum may rebound next month though, when January’s 1.04% M/M reading falls out of the 3m/3m calculation.

- Turning back to Y/Y NSA rates, the proportion of sub-components with annual rates between 1-3% Y/Y (i.e. broadly target consistent) ticked up to 21% from 20% in May and 17% in April. 63% of components had annual inflation rates below 3% in June, unchanged from May.

MNI EXCLUSIVE: MNI looks at the BOJ's internal policy calculations

MNI looks at the BOJ's internal policy calculations. -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com