MNI Eurozone Inflation Insight: Nov 2025

Dec-03 12:28By: Moritz Arold

European Central Bank+ 2

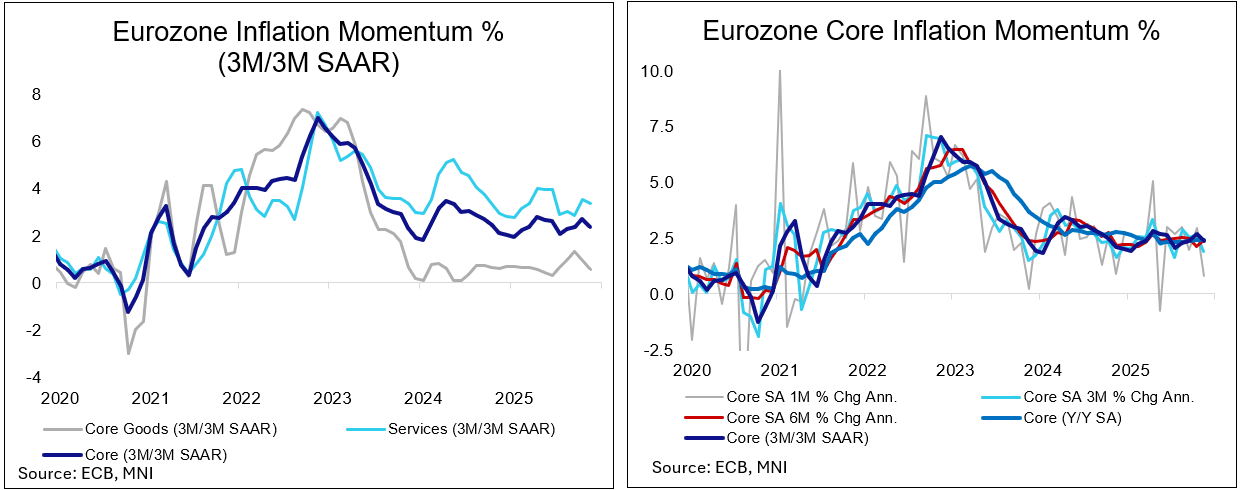

- HICP inflation was as originally expected but marginally above where consensus likely stood following most country-level data in the flash November release. Core HICP was in line with expectations.

- Energy was the main mover and surprise, coming in 0.3pp above expectations.

- The full November release on Dec 17 will provide a more useful update on exact drivers. That especially applies to services inflation, where it is not yet clear to what extent firm October airfares may have unwound.

- By country, Germany and Spain were stronger than expected, while France, Italy and the Netherlands saw downside misses.

- The ECB is still seen as being highly unlikely to cut at its Dec 18 meeting (<1bp priced), where new projections will be watched to judge whether a very mild easing bias (6bp of cuts by mid-2026) is warranted.