MNI US OPEN - Volatile Components Drive Upside UK CPI Surprise

EXECUTIVE SUMMARY

- RBNZ MAKES DOVISH 25BP CUT, EYES 2.5% OCR

- RIKSBANK HOLDS IN AUGUST, FURTHER 2025 CUT POSSIBLE

- UK UPSIDE CPI SURPRISE DRIVEN BY VOLATILE AIR FARES AND ACCOMMODATION

- JAPAN JULY EXPORTS POST 3RD STRAIGHT ANNUAL DROP

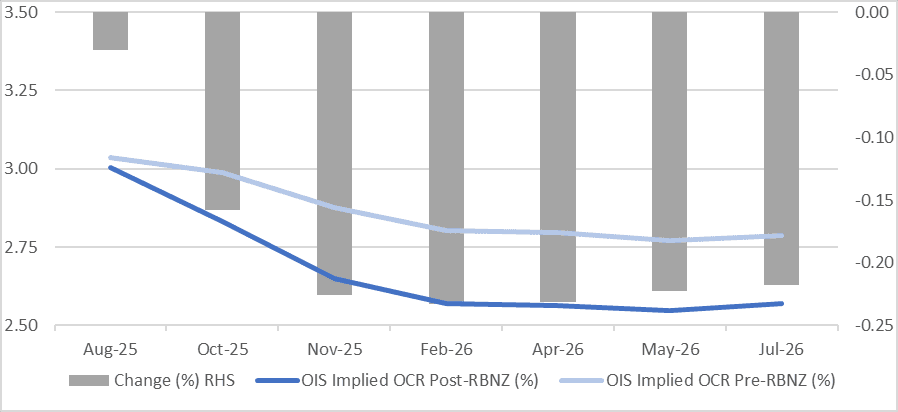

Figure 1: RBNZ-dated OIS pre-RBNZ vs. post-RBNZ (%)

Source: MNI/Bloomberg Finance L.P.

NEWS

RBNZ (MNI): MPC Makes Dovish 25bp Cut, Eyes 2.5% OCR

The Reserve Bank of New Zealand Monetary Policy Committee voted four-two to cut the Official Cash Rate 25 basis points to 3% on Wednesday, opting against a larger 50bp move, while publishing forecasts that signalled a more dovish policy path. Acting Governor Christian Hawkesby said the Bank was comfortable with the market's swift reaction, with the OCR now priced at 2.5% by February, noting the move was anticipated given the Reserve’s signals. “The signalling power of the vote and of the OCR track means that actual conditions and markets can start moving for us in terms of providing that additional easing,” he said.

RIKSBANK (MNI): Riksbank Holds in August, Further 2025 Cut Possible

The Riksbank Executive Board left its policy rate on hold at 2.0% at its August meeting and said that it saw "some probability of a further interest rate cut this year," leaving its guidance essentially unchanged and leaving open whether it will cut in September. The assessment of economic developments in the Monetary Policy Update provided some grounds to support the notion that the Swedish central bank has room to ease further, but the message was nuanced.

US/CHINA (BBG): Bessent Says China Tariff Status Quo ‘Working Pretty Well’

Treasury Secretary Scott Bessent indicated the US is satisfied with the current tariff set up with China, a signal the Trump administration is looking to maintain calm with its economic rival before a trade truce expires in November. When asked in a Fox News interview when progress in negotiations would be seen and if the US needed a trade agreement because of how tariffs were going, Bessent said that “we’re very happy” with the situation with China. “I think right now the status quo is working pretty well,” he said. “China is the biggest revenue line in the tariff income — so if it’s not broke, don’t fix it,” he said in the interview on Tuesday.

US (BBG): Trump Raises Stakes Over Copper Project With CEOs at White House

President Donald Trump met with the chief executive officers of the world’s two biggest mining companies to discuss a copper project that could supply the US with a quarter of its demand for decades to come, adding greater weight to his push to boost local output of the vital metal. Rio Tinto Group’s Jakob Stausholm; his incoming replacement, Simon Trott; and counterpart at BHP Group, Mike Henry, met the US leader to discuss the Resolution project in Arizona, according to a LinkedIn post by Stausholm.

US (FT): Scott Bessent Bets on Stablecoins to Bolster Demand for Treasuries

Treasury secretary Scott Bessent is betting the crypto industry will become a crucial buyer of Treasuries in coming years as Washington seeks to shore up demand for a deluge of new US government debt. Bessent has signalled to Wall Street that he expects stablecoins, digital tokens that are backed by high-quality securities such as Treasuries, to become an important source of demand for US government bonds, said people familiar with the discussions.

US (BBG): Trump Embarks on $104 Million Bond-Buying Spree While in Office

President Donald Trump has bought hundreds of bonds since he returned to office, including those sold by US companies affected by the sweeping changes to federal policies he’s championed. The 690 transactions, the first of which was made the day after his inauguration, total at least $103.7 million, according to a document released by the White House on Tuesday that disclosed the billionaire’s investing activity this year through early August.

ECB (MNI): Lagarde Says Effective US Tariff Rate "Somewhat Higher" Than June Baseline

Lagarde holding remarks at the International Business Council of the World Economic Forum in Geneva. Key highlights: "Recent trade deals have alleviated, but certainly not eliminated, global uncertainty, which persists on account of the unpredictable policy environment." Says "The euro area economy proved resilient earlier this year in the face of a challenging global environment."

UK (FT): Rachel Reeves Explores Reform to Capital Gains Tax on Expensive Houses

Chancellor Rachel Reeves is examining ways of raising tax revenue from high-value homes including through reforms to capital gains tax, according to people familiar with the discussions, as UK ministers confront a hole in the public finances of at least £20bn. The idea of imposing a so-called mansion tax is being discussed within the Treasury as it considers ways to reform the UK’s property tax system, with various options on the table for raising revenue from more expensive houses. The UK exempts people’s main homes from CGT, although if they have other properties they can be subject to the levy.

ISRAEL (MNI): 60k to Be Called Up for Gaza City Op That Could Start Within Weeks

The Israeli gov't is reported to be reviewing the prospective ceasefire deal put forward by Qatar and Egypt and agreed to by Hamas on 18 August. Initially, PM Benjamin Netanyahu was reported to have been 'dismissive' towards the prospect of a truce being reached. The Times of Israel, though, claims that "Two Israeli officials said Tuesday that Jerusalem is studying the hostage-ceasefire proposal accepted by Hamas, and that Netanyahu is expected to convene discussions about it soon. A response is expected in the coming two days, said a Palestinian source close to the talks."

CHINA (BBG): China Set to Tackle Petrochemicals Overcapacity With Overhaul

The Chinese government is set to launch a sweeping overhaul of its petrochemicals and oil refining sector, phasing out smaller facilities and targeting outdated operations for upgrades, while redirecting investment to advanced materials. Remedies to curtail longstanding overcapacity in lower-value parts of the industry are likely within the next month, according to people familiar with the matter. The detailed plan is awaiting final approval from the Ministry of Industry and Information Technology, they said, declining to be identified discussing matters that aren’t public yet.

CHINA (MNI): China LPR Remains Unchanged in August

MNI (Beijing) China's Loan Prime Rate held steady on Wednesday, in line with expectations as the central bank highlights structural facilities to support key sectors. The LPR remained unchanged at 3.0% for the one-year maturity and 3.5% for the five-year tenor and over. Both rates fell in May by 10bp after the PBOC lowered the 7-day reverse repo rate – its benchmark policy rate – 10bp to 1.4% on May 8, followed by a 50bp reduction to the reserve requirement ratio on May 15.

INDIA/RUSSIA (BBG): India Ramps Up Buying of Russian Oil Despite US Criticism

India’s state-run refiners have returned to buying Russian oil after a brief pause, despite the South Asian nation facing higher tariffs for the trade and a volley of criticism from Trump officials. Processors including Indian Oil Corp. and Bharat Petroleum Corp. bought some cargoes of Russian Urals over the past two days, said traders familiar with the matter who asked not to be identified because they’re not authorized to speak publicly. Shipments are for loading in September and October, they added.

THAILAND (BBG): Thai Central Bank Says More Easing Only If Outlook Worsens

Thailand’s central bank would need to see a “significant material deterioration” in its economic growth outlook, or face unexpected shocks, to justify additional rate cuts beyond the three reductions it has made this year, a top official said. The Bank of Thailand’s monetary policy stance remains accommodative, and the rate panel has taken into account pressures to growth from US tariffs starting the second half, Deputy Governor Piti Disyatat said in a Bloomberg TV interview on Wednesday.

DATA

UK DATA (MNI): Upside Surprise Driven by Volatile Air Fares and Accommodation

- UK JUL CPI +0.1% M/M, +3.8% Y/Y

- UK JUL CORE CPI +0.2% M/M, +3.8% Y/Y

- UK JUL SERVICES CPI +0.7% M/M, +5% Y/Y

- UK JUL RPI +0.4% M/M, +4.8% Y/Y

Headline just 7 hundredths above the BOE's forecast. Air fares alone added 11 hundredths to headline CPI and accommodation 9 hundredths. That more than accounts for the upside surprise alone and is unlikely to be persistent. Those categories alone accounted for a 4 tenth increase in services CPI, which only came in 10 hundredths above the BOE's forecast. Food price inflation coming in higher than expected will be a bit of a concern. Note that the BOE's forecasts for the next 2-3 months are already above consensus though, with a number of analysts in their previews noting the potential that we are close to the peak. The September peak is unlikely to be meaningfully different to where it was expected before this data, however, with air fares likely to have normalised by then.

UK DATA (MNI): Brightmine Pay Deals Stay at 3.0%, Upper Quartile Falls to Cycle Low

- UK MAY-JUL MEDIAN PAY AWARDS +3%: Brightmine

Brightmine median pay awards in the 3 months to July remained at 3.0% for the eighth consecutive rolling quarter. While the BoE and analysts expect inflation to egde up in July's print and to peak even higher in September and hence remaining sticky, CPI is still some way off the levels seen over the past few years. The press release again points to employers remaining cautious in the face of uncertainty and the upcoming Autumn Budget.

EUROZONE JUL FINAL HICP +0% M/M, +2% Y/Y (MNI)

EUROZONE JUL FINAL CORE HICP -0.2% M/M, +2.3% Y/Y (MNI)

EUROZONE JUL FINAL SERVICES HICP +1.1% M/M, +3.2% Y/Y (MNI)

JAPAN DATA (MNI): Japan July Exports Post 3rd Straight Drop

- JAPAN JULY EXPORTS -2.6% Y/Y; JUNE -0.5%

Japan’s exports fell for the third straight year-on-year drop in July, down 2.6% after June’s 0.5% decline, as U.S. tariffs hit shipments of automobiles and iron, and steel products, Ministry of Finance data showed Wednesday. Automobile exports slid 11.4% in July, the fourth consecutive fall after -7.3% in June, following front-loaded shipments earlier this year. Exports of iron and steel products dropped 21.0% after June’s 13.2% fall. Imports declined 7.5% in July, the first fall in two months after June’s 0.3% gain. Japan posted a trade deficit of JPY117.5 billion, reversing a JPY152.1 billion surplus in June.

JAPAN DATA (MNI): Core Machine Orders Above Forecasts, Suggesting Resilient Capex

- JAPAN JUNE CORE MACHINE ORDERS +3.0% M/M; MAY -0.6%

Japan June core machine orders were better than forecast. We rose 3.0%m/m, versus -0.5% forecast and -0.6% prior. The y/y print was 7.6%, against a 4.7% forecast and 4.4% prior. The chart below overlays y/y core machine orders (the white line on the chart) against capex for Japan in y/y terms (ex Software). Today's machine orders print continues to paint a resilient capex picture for Japan's economy. We don't get the full capex read for Q2 until the start of Sep. Still, the recent Q2 GDP print (preliminary) showed business up 1.3% in Q2, which was above forecasts (+0.7%). So today's core machine orders result is consistent with that backdrop.

FOREX: UK Inflation Favours GBP, But No Range Break Yet

- UK inflation data came in hotter-than-expected, with an outsized contribution from services inflation helping boost the headline print to 3.8%. This leaves the UK with one of the highest core rates of inflation in the G10, and while much of the pressure stemmed from seasonality (airfares in particular), it still relieves pressure on the MPC to lean further on this year's easing cycle. That said, market moves have been generally contained. Year-end SONIA pricing factored out around 1bps of BoE rate cuts (now at ~12bps), and pressured EUR/GBP to daily lows of 0.8609 as a result.

- NZD slips against all others in G10 on the RBNZ rate decision for August. The bank cut rates by 25bps, but more importantly triggered NZD sales by signalling deeper rate cut below neutral - pressing markets to price in a greater likelihood of 50bps of further cuts into year-end. NZD/USD made light work of the 0.5833 200-dma support in the initial reaction, having already cleared 0.5847. 0.5803 marks the next downside level: the 50% retracement for the rally off the April low.

- The USD Index has crept to a new weekly high at 98.441 despite the GBP rally. Prices continue to edge higher as markets appear to be adopting a more neutral position headed into Friday's Jackson Hole appearance from Chair Powell. Despite Trump's renewed criticism of Powell's approach to policy overnight (this time, Trump highlighted the issues for the housing market from high rates), there remains a risk that Powell pushes against the urgency of easing in September - any suggestion of which would work against the 21bps of cuts currently priced, and favour the dollar.

- Fed minutes due Wednesday will be carefully watched for the conversation around rates and, in particular, any clues as to whether further FOMC members came close to dissenting alongside Bowman and Waller at the most recent rate decision. While today's Fed release will be of importance, it's Powell's appearance at Jackson Hole on Friday that'll likely be of more market interest.

EGBS: Bunds Stronger on Session, But Off Highs Post Auction

Bund futures moved off session highs following a weak 20/30-year auction, now +19 ticks at 129.26 (session highs were 129.35). A technical bear threat is still present for now, with a move above the 50-day EMA at 129.89 required to signal a reversal.

- German yields are 1-1.5bps lower, with the curve bull flattening.

- Alongside the Bund auction, Finland is launching a new 7-year RFGB via syndication. The ESM has also sent an RFP for a transaction, likely next week.

- 10-year EGB spreads to Bunds are biased slightly wider, with OATs underperforming. The BTP/Bund spread has inched back above 80bps.

- ECB President Lagarde suggested global uncertainty has been “alleviated, but certainly not eliminated”. Overall, she did little to push back on current market pricing (1.5bps of cuts through September, 12bps through December).

- ECB final headline and core July HICP confirmed flash estimates on a rounded basis, while services saw a small upward revision to 3.2% Y/Y.

GILTS: Bounces From CPI-Driven Lows Extends, Although Bearish Theme Intact

Gilt futures have traded through yesterday’s highs.

- The hawkish impact stemming from this morning’s firmer-than-expected CPI data was short-lived.

- At the time we argued that there wasn’t much in the way of game-changing information within the data, although the MPC will not have welcomed the overshoot vs. both market and its own projections.

- That idea played out when it came to the initial market reaction, with hawkish opening moves in both gilts and STIRs quickly countered. Support also stems from a bid in wider core global FI.

- Futures traded as low as 90.54 before recovering to 90.88.

- Bears remain in technical control, initial support and resistance located at 90.43/91.32.

- Yields 3-4bp lower across the curve.

- The May high in 10s (4.80%) remains untouched.

- 50s have pierced 5.00% over the past couple of sessions, but bears failed to force a sustained move above the psychological level, 4.94% last.

- Light outperformance for gilts vs. Bunds likely stems from pre-data positioning and spreads operating around multi-week wides ahead of the release.

- SONIA futures now -1.0 to +3.5 at/just off session highs. May lows go untested in SFIZ5, while June lows are untested in SFIZ6.

- BoE-dated OIS ~2bp more hawkish to ~2bp more dovish across liquid contracts, showing 6bp of easing for November and 11bp through year-end.

- Outside of the CPI data, Brightmine wage growth (released overnight) once again held steady at 3.0% in Y/Y terms for the three months through July.

- Little of note on the UK macro calendar for the remainder of the day.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.973 | +0.6 |

Nov-25 | 3.909 | -5.8 |

Dec-25 | 3.860 | -10.7 |

Feb-26 | 3.760 | -20.7 |

Mar-26 | 3.718 | -24.9 |

Apr-26 | 3.645 | -32.2 |

EQUITIES: Trend Set-Up in Eurostoxx 50 Futures Remains Bullish

The trend set-up in Eurostoxx 50 futures remains bullish and the contract traded to a fresh short-term cycle high yesterday. The print above the May and July highs strengthens a bull theme and signals scope for a climb towards 5575.00, the Mar 3 high (cont) and key resistance. Moving average studies remain in a bull-mode position, highlighting an uptrend. Support to watch lies at 5355.64, the 50-day EMA. The dominant uptrend in S&P E-Minis remains intact and the latest shallow retracement is considered corrective. Moving average studies are in a bull-mode position, highlighting a clear uptrend. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6402.75, the 20-day EMA, and 6282.00, the 50-day EMA.

- Japan's NIKKEI closed lower by 657.74 pts or -1.51% at 42888.55 and the TOPIX ended 17.72 pts lower or -0.57% at 3098.91.

- Elsewhere, in China the SHANGHAI closed higher by 38.922 pts or +1.04% at 3766.21 and the HANG SENG ended 43.04 pts higher or +0.17% at 25165.94.

- Across Europe, Germany's DAX trades lower by 92.87 pts or -0.38% at 24331.41, FTSE 100 lower by 13.65 pts or -0.15% at 9175.72, CAC 40 down 10.09 pts or -0.13% at 7968.99 and Euro Stoxx 50 down 6.46 pts or -0.12% at 5476.82.

- Dow Jones mini down 102 pts or -0.23% at 44896, S&P 500 mini down 13.25 pts or -0.21% at 6419, NASDAQ mini down 60 pts or -0.26% at 23408.5.

Time: 10:00 BST

COMMODITIES: Bullish Theme in Gold Intact, Despite Recent Pullback

WTI futures remain in a clear bear cycle and the contract continues to trade closer to its recent lows. A key support at $61.99, the Jun 30 low, has been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $63.91, the 50-day EMA. Despite the latest pullback, a bull cycle in Gold remains intact. Moving average studies are in a bull-mode position. The sideways trend that has been in place since the Apr peak appears to be a corrective phase - a pause in the uptrend. A resumption of gains would open $3439.0, the Aug 23 high. Key resistance and the bull trigger is at $3500.1, the Apr 22 low. On the downside, first support to watch lies at $3268.2, the Jul 30 low.

- WTI Crude up $0.65 or +1.04% at $63

- Natural Gas down $0.01 or -0.51% at $2.753

- Gold spot up $9.3 or +0.28% at $3324.81

- Copper up $0.05 or +0.01% at $449.05

- Silver down $0.34 or -0.91% at $37.0265

- Platinum up $0.37 or +0.03% at $1315.4

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 20/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 20/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 20/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 20/08/2025 | 1500/1100 | Fed Governor Christopher Waller | ||

| 20/08/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 20/08/2025 | 1800/1400 | FOMC Minutes | ||

| 20/08/2025 | 1900/1500 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 21/08/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 21/08/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/08/2025 | 0600/0800 | ** | Norway GDP | |

| 21/08/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 21/08/2025 | 0900/1100 | ** | Construction Production | |

| 21/08/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 21/08/2025 | 1130/0730 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 21/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 21/08/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 21/08/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 21/08/2025 | 1400/1000 | *** | NAR existing home sales | |

| 21/08/2025 | 1400/1000 | * | Services Revenues | |

| 21/08/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 21/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 21/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 21/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 21/08/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 30 Year Bond |