MNI RBNZ WATCH: MPC Makes Dovish 25BP Cut, Eyes 2.5% OCR

The Reserve Bank of New Zealand Monetary Policy Committee voted four-two to cut the Official Cash Rate 25 basis points to 3% on Wednesday, opting against a larger 50bp move, while publishing forecasts that signalled a more dovish policy path.

Acting Governor Christian Hawkesby said the Bank was comfortable with the market's swift reaction, with the OCR now priced at 2.5% by February, noting the move was anticipated given the Reserve’s signals. “The signalling power of the vote and of the OCR track means that actual conditions and markets can start moving for us in terms of providing that additional easing,” he said. (See MNI RBNZ WATCH: MPC Likely To Cut 25bp To 3%)

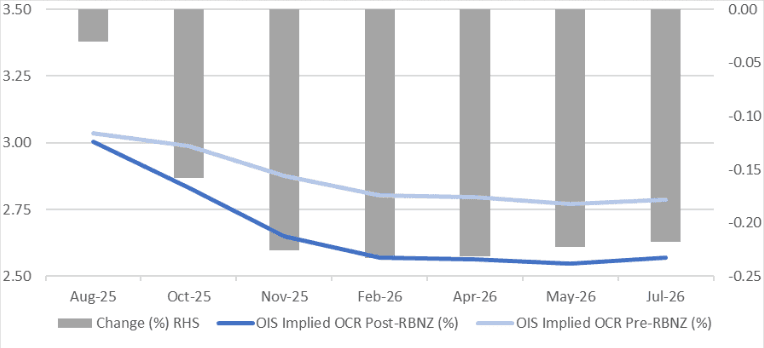

The four-two split was the most fractious in the MPC’s history. The dovish tilt saw NZGBs close 10-16bp richer, with OIS pricing down 14-23bp across future meetings, and 35bp of further easing priced by November. (See chart)

DOVISH TRACK

Hawkesby pointed to July’s hold decision and suggestions then that 3% might represent a floor, noting fresh data published since showed greater spare capacity. (See MNI RBNZ WATCH: MPC Holds, Eyes August Cut)

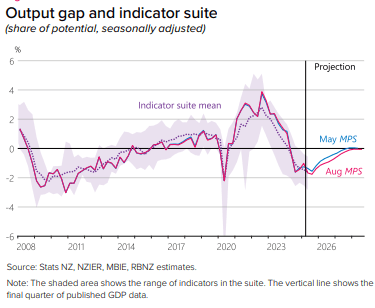

The Bank’s latest Hidden PDF revised Q2 GDP growth down 60bp to -0.3% from May’s projections, adding to concerns about the output gap, he continued. “That doesn't need to be the case, and so we need lower interest rates to close that gap,” he said, adding that the next two meetings in October and November will be live.

"That projection troughs at around 2.5% by the end of this year, and so that would be consistent with further cuts through the course of this year."

The MPS showed the OCR reaching 2.5% by March, 40bp lower than May’s track. While the decision was split, Hawkesby said there was strong consensus around the central projection.

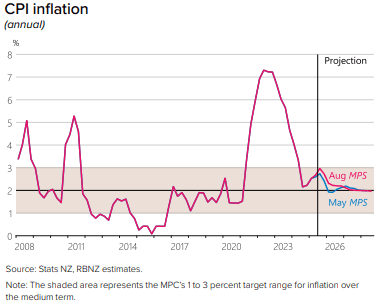

Forecasts also showed inflation peaking at 3% by September, up 30bp from May, and Hawkesby noted the rise reflected factors little affected by monetary policy. “I'd really emphasise quite strongly that the mandate is to set interest rates today to achieve our inflation target in the medium term,” he said. “With inflation pressures abating, our job is to stay focused on that horizon.”

NEUTRAL RATE

Chief Economist Paul Conway said the Bank’s view of neutral between 2.5-3.5% had not changed, but the OCR was clearly no longer restrictive. “We're sort of in that zone of neutral, but you can't be too mechanistic about these things,” he said, noting uncertainty from tariffs and global policy tensions.

Despite lower GDP forecasts, Assistant Governor Karen Silk said the economic slowdown was largely over. Q2 reflected an “uncertainty shock” from U.S. trade policies that hit consumer confidence, but underlying demand remains solid, she argued. “End of Q4 last year, Q1 this year, we did see consumption up, investment up. We then got hit with an uncertainty shock at the beginning of Q2. As that starts to wane, we believe monetary policy transmission will continue to have the impact we were starting to see late last year and into early this year,” she said.

The MPC next meets Oct 8.