FOREX: UK Inflation Favours GBP, But No Range Break Yet

- UK inflation data came in hotter-than-expected, with an outsized contribution from services inflation helping boost the headline print to 3.8%. This leaves the UK with one of the highest core rates of inflation in the G10, and while much of the pressure stemmed from seasonality (airfares in particular), it still relieves pressure on the MPC to lean further on this year's easing cycle. That said, market moves have been generally contained. Year-end SONIA pricing factored out around 1bps of BoE rate cuts (now at ~12bps), and pressured EUR/GBP to daily lows of 0.8609 as a result.

- NZD slips against all others in G10 on the RBNZ rate decision for August. The bank cut rates by 25bps, but more importantly triggered NZD sales by signalling deeper rate cut below neutral - pressing markets to price in a greater likelihood of 50bps of further cuts into year-end. NZD/USD made light work of the 0.5833 200-dma support in the initial reaction, having already cleared 0.5847. 0.5803 marks the next downside level: the 50% retracement for the rally off the April low.

- The USD Index has crept to a new weekly high at 98.441 despite the GBP rally. Prices continue to edge higher as markets appear to be adopting a more neutral position headed into Friday's Jackson Hole appearance from Chair Powell. Despite Trump's renewed criticism of Powell's approach to policy overnight (this time, Trump highlighted the issues for the housing market from high rates), there remains a risk that Powell pushes against the urgency of easing in September - any suggestion of which would work against the 21bps of cuts currently priced, and favour the dollar.

- Fed minutes due Wednesday will be carefully watched for the conversation around rates and, in particular, any clues as to whether further FOMC members came close to dissenting alongside Bowman and Waller at the most recent rate decision. While today's Fed release will be of importance, it's Powell's appearance at Jackson Hole on Friday that'll likely be of more market interest.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

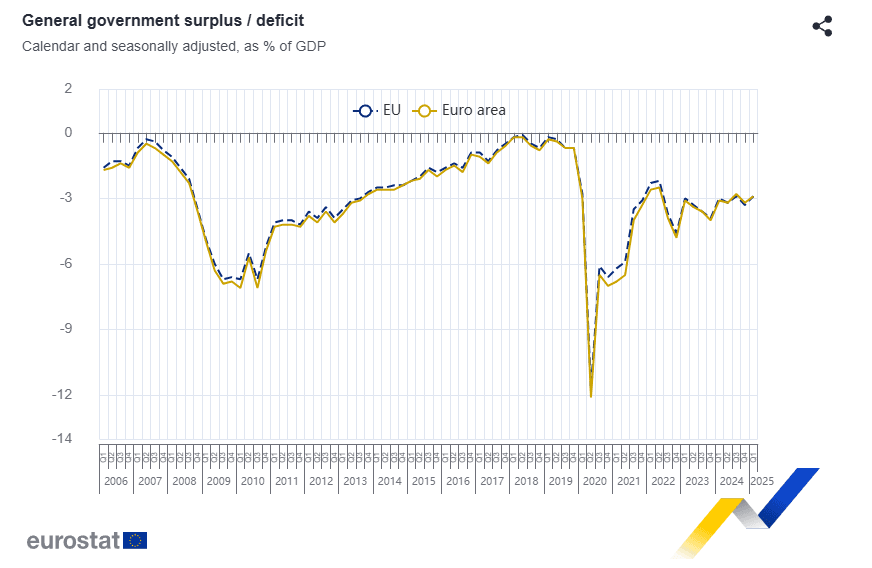

EUROPEAN FISCAL: EZ Debt/GDP Inches Up In Q1; Germany The Key Fiscal Theme Ahead

The Eurozone debt to GDP ratio inched up to 88.0% in Q1, up from 87.4% in Q4 2024 and 87.8% in Q1 2024. Compared with a year ago, the debt/GDP ratio has fallen most in Greece (-9.3pp to 152.5%), Cyprus and Ireland (-6.1pp to 34.9% - though, a reminder that Irish national accounts are best viewed through the lens of modified GDP, which strips out globalisation effects). The largest increases in debt/GDP were seen in Finland (+5.1pp to 83.7%), Austria (+4.1pp to 84.9%) and France (+3.6pp to 114.1%).

- The seasonally adjusted deficit to GDP ratio was 2.9% in Q1, down from 3.2% in Q4 2024 but up from 2.8% in Q3.

- A ramp-up in German (especially defence) spending is the key European fiscal theme in the coming years. Analysts were on balance surprised to the upside by the 2025-2029 fiscal plan announcement in terms of money spent, but some continue to point to some downside risks to the announced investment figures, and see the need for structural reforms in Germany.

- The seasonally adjusted German deficit inched down to 2.3% GDP in Q1 (vs 2.4% prior), but will likely start rising from the second half of this year onwards as the spending uptick kicks in.

- Although some high debt countries (e.g. France and Italy) are attempting to consolidate primary balances to reduce debt burdens, increased interest expenses (due to Covid-induced spending and higher interest rates) continue to push total debt/GDP in the opposite direction.

TARIFFS: Taiwan-US Trade Talks To Continue This Week

"*TAIWAN SAYS TO CONDUCT NEW ROUND OF TRADE TALKS W/ US THIS WEEK" Bloomberg

FOREX: Stronger Volumes Bid GBP to Session Highs

An uptick in volumes responsible for this bid in GBP; GBP futures see near 1,200 contracts trade inside the past three minutes (cash equivalent of over $90mln) for the best volumes of the day so far.

- This tips GBP/USD within range of the Friday high of 1.3475 - the next notable upside level. GBP now among the best performers in G10, but GBP/JPY still trades lower.

- Rate appears to be building a base at the mid-July pullback lows of 1.3365 after last week's data which - while not ruling out an August BoE rate cut - has dented the pricing for sequential cuts later this year.

- Prelim PMI data due Thursday is the calendar highlight, but broader focus remains on the state of public finances as the Chancellor's revenue raising options continue to dwindle: The Times write this morning that Reeves is to defy calls from some party members to institute a wealth tax - deeming the option as unworkable.