MNI US OPEN - US Senate Passes Measure to End Shutdown

EXECUTIVE SUMMARY

- SENATE PASSES FUNDING PACKAGE, US GOVERNMENT SET TO REOPEN ON WEDNESDAY

- TRUMP SAYS CLOSE TO INDIA TRADE DEAL TO BRING TARIFFS DOWN

- CHINA HATCHES PLAN TO KEEP US MILITARY FROM GETTING ITS RARE-EARTH MAGNETS: WSJ

- UK LABOUR MARKET DATA SOFT ACROSS THE BOARD

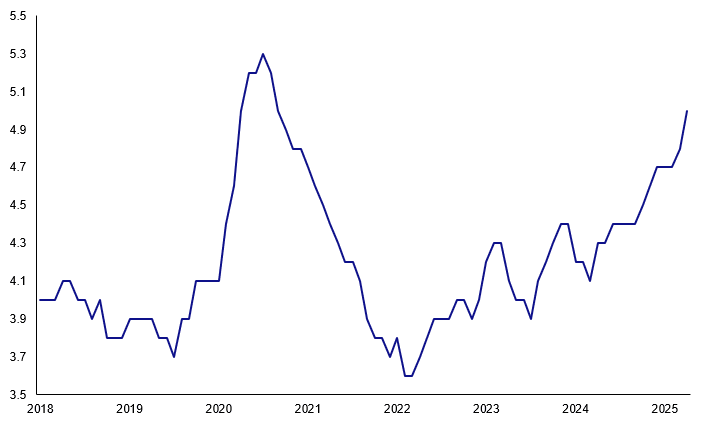

Figure 1: UK unemployment rate rises to new multi-year high

Source: MNI, ONS

NEWS

US (MNI): Veterans Day Exchange Schedules

The observance of the Veterans Day holiday will mean that some U.S. markets are subjected to abbreviated trading hours and/or closures today. Note that cash equities are open while cash Tsys are closed. Click the link above to find detailed operating hours/closures.

US (MNI): Senate Passes Funding Package, US Government Set to Reopen on Wednesday

The United States Senate has passed a funding package to reopen the US government. The package, which now heads to the House of Representatives, includes three full-year FY2026 appropriations bills covering agencies related to the Departments of Agriculture, Military Construction and Veterans Affairs, and the legislative branch. Remaining US government agencies will be funded at existing levels through January 30 with a new short-term funding measure (Continuing Resolution). House Speaker Mike Johnson (R-LA) - who has kept the House recessed for 54 days - has teed up votes in the House at 16:00 ET 21:00 GMT on Wednesday, November 12, allowing members sufficient time to reach the capital in light of shutdown-related travel delays.

US/INDIA (BBG): Trump Says Close to India Trade Deal to Bring Tariffs Down

President Donald Trump said he “at some point” would reduce the tariff rate on Indian goods, saying the US was getting “pretty close” to a trade deal with New Delhi. “Right now they don’t love me, but they’ll love us again,” Trump said. “We’re getting a fair deal.” Trump later predicted the nations were “pretty close to doing a deal that’s good for everybody.”

US/SWITZERLAND (MNI): US-Swiss Trade Deal Would Be Moderate Plus; Limited Impact on SNB

A potential Swiss trade deal with the US should see a moderate upward revision of 2026 GDP forecasts, but is unlikely to sway SNB rates this year or the next. "I haven't said any number [...] we're going to be working on something to help Switzerland along. We hit Switzerland very hard. We want Switzerland to remain successful" US President Trump added to earlier sources reports, touting a 15% tariff rate to potentially be agreed within two weeks. Note that following the US's August 1st 39% tariff announcement on Swiss imports, the Swiss government downwardly revised its 2026 GDP forecast by 0.3pp to 0.9%, while leaving its 2025 forecast of 1.3% intact. Inflation forecasts were materially unchanged following the tariff announcement.

US/CHINA (WSJ): China Hatches Plan to Keep U.S. Military From Getting Its Rare-Earth Magnets

China plans to ease the flow of rare earths and other restricted materials to the U.S. by designing a system that will exclude companies with ties to the U.S. military while fast-tracking export approvals for other firms, according to people familiar with the plan. The "validated end-user" system, or VEU, would enable Chinese leader Xi Jinping to follow through on a pledge to President Trump to facilitate the export of such materials while ensuring that they don't end up with U.S. military suppliers, a core concern for China, according to the people familiar with the plan.

US (WSJ): SoftBank Sells Its Nvidia Stake for $5.8 Billion

SoftBank Group said it sold its stake in Nvidia for $5.83 billion as it reported its quarterly net profit more than doubled thanks to billions of dollars of gains from its OpenAI investment. The Japanese technology-investment company on Tuesday reported net profit of 2.502 trillion yen, equivalent to $16.23 billion, for the three months ended September, up sharply from ¥1.180 trillion a year earlier.

US/COMMODITIES (BBG): US Aluminum Hits Record High as Tariffs Shrink Inventory

The price for aluminum delivered to the US hit a record high on Monday as inventories dwindle due to US tariffs. That all-in American price, which includes the global benchmark cash price set on the London Metal Exchange and the so-called US Midwest premium, climbed to $4,816.004 a ton in the previous session.

BOE (MNI): BOE Should Hold Policy Levels for Now - Greene

Preliminary results from the Bank of England's agents' pay survey, published before the February meeting, show wage settlements rising by 3.5%, Bank of England Monetary Policy Committee member Megan Greene said on Tuesday. That suggests "monetary policy should be more restrictive than otherwise ... we might not be meaningfully restrictive in our monetary policy stance." The BOE published alternative scenarios with endogenous rate paths for the first time at its MPC meeting this month, and "interestingly all but one of these rules suggested a prolonged hold in interest rates is appropriate," Greene said at a UBS conference.

RIKSBANK (MNI): Thedeen Says Bar to Rate Change Has Increased

The Riksbank's November meeting minutes have been released. Governor Thedeen suggests his bar for supporting a rate move in either direction has increased. A reminder that in an interview with the MNI Policy Team last week, he suggested the current 1.75% policy rate is likely stimulative, despite its being near the bottom of the estimated range for the neutral rate.

ECB (BBG): ECB Is in a Good Position on Interest Rates, Kocher Says

European Central Bank Governing Council member Martin Kocher suggested that he’s comfortable with the current policy settings. “We are in a good position on interest-rate policy,” the Austrian central bank chief said Tuesday in Vienna, reiterating what has become the standard line from ECB officials. “The expectation is that not much more will happen in the next months.”

ECB (BBG): ECB’s Elderson Says Current Rate Level Is Appropriate: Expansion

European Central Bank Executive Board member Frank Elderson says the current level of interest rates “is appropriate, but we will continue to be data-dependent and will decide one meeting at a time,” according to interview with Expansion. “Our monetary policy is in a good place. It’s true that the economic environment remains uncertain, so we cannot commit to a pre-determined interest rate path. What we need to do is to make sure that the rates are consistent with achieving our target, and so far they are.”

ECB (MNI): China’s Surplus Driven by Weak Demand - ECB Bulletin

China's weak domestic demand rather than U.S.-China trade tensions is the key factor for the strong rise of exports to Europe and the stagnation of imports, the European Central Bank published in its latest Economic Bulletin on Tuesday. China’s real estate downturn and policies promoting self-reliance under “Made in China 2025” have eroded household demand and curbed imports, particularly of consumer and intermediate goods, with weak domestic sales and falling export prices prompting firms to seek foreign markets — notably in sectors such as motor vehicles and steel, where exports have grown by about 75% since 2022, the ECB said.

EU/CHINA (BBG): EU Eyes Huawei Ban in Mobile Networks of Member Countries

The European Commission is exploring ways to force European Union member states to phase out Huawei Technologies Co. and ZTE Corp. from their telecommunications networks, according to people familiar with the matter. Commission Vice President Henna Virkkunen wants to convert the European Commission’s 2020 recommendation to stop using high-risk vendors in mobile networks into a legal requirement, according to the people, who asked not to be identified because the negotiations are private.

CHINA (BBG): China Tightens Rules for State-Owned Firms to Add Foreign Debt

China is making it harder for some state-owned companies to borrow overseas, expanding a campaign to rein in local government debt risks, according to people familiar with the matter. The National Development and Reform Commission, China’s top economic planning agency, has in recent weeks set tighter criteria, including those for profitability and business scope, for regional-level state-owned enterprises to get additional offshore debt quotas, said the people who requested anonymity discussing private matters.

CHINA (MNI): China to Boost Private Investment Financing - NDRC

MNI (Beijing) China will increase financing support for key private investment which has been affected by changes in the international environment and the fall in real estate prices, officials of National Development And Reform Commission told reporters on Tuesday. Efforts will be made to introduce a "green channel" for sci-tech companies to facilitate their listing, financing, and mergers and acquisitions, while supporting private investment projects in issuing Real Estate Investment Trusts (REITs) in the infrastructure sector, they said.

CHINA (MNI): China Ready to Use Central Budget to Support SMEs

MNI (Beijing) China's National Development and Reform Commission will make good use of the central budget to support private investment projects, Guan Peng, the agency's deputy director of the Economic Operation Adjustment Bureau, told reporters on Tuesday. Officials will strengthen procurement policy to support SME firms, with local governments encouraged to increase the portion of advance payment to private firms to more than 30% of the contract amount, Peng added.

CHINA (BBG): PBOC Pushes Yuan Borrowing Abroad to Internationalize Currency

China’s central bank vowed to further encourage financing in the yuan by overseas entities, betting cheap borrowing costs and increased demand for the currency offshore will be crucial drivers for its globalization. The country will promote the role of the yuan as a funding currency as one of the key steps to advance its internationalization, the People’s Bank of China said in its annual report released Oct. 30.

CHINA/CANADA (BBG): China Is Willing to Consolidate Ties With Canada, Wang Yi Says

China is willing to strengthen communication with Canada and take effective actions to accelerate the resumption of exchanges and cooperation across various fields, the official Xinhua News Agency reports, citing Foreign Minister Wang Yi.

INDIA/RUSSIA (BBG): Most Indian Oil Refiners Skip Buying Russian Crude for December

India has scaled back purchases of Russian crude for arrival in December, showing that Western sanctions and trade talks with the US are having a major impact on buying patterns. Five big Indian refiners haven’t placed any orders for Russia oil for next month, according to people familiar with the matter, who asked not to be named due the sensitivity of the trade. Typically, deals for crude for the following month are done by the 10th of the current month.

THAILAND (BBG): Thailand Spurns Cambodia Peace Deal Tied to US Trade Talks

Thailand has suspended a peace process with Cambodia that was a condition for tariff negotiations with US President Donald Trump, after Thai soldiers were injured in a land-mine blast near the border. The suspension will remain in place until the Thai armed forces deem “hostilities” have ceased, Prime Minister Anutin Charnvirakul told reporters after a meeting of the National Security Council on Tuesday. “We will do what we think is right.”

CHILE (MNI): Predictions Markets See Jara-Kast Run-Off as Overwhelmingly Likely

With just a few days to go until the first round of the presidential election on 16 November, political prediction markets show a strong bias towards the view that the two candidates set to make the December run-off will be left-wing Unity for Chile (UpCh) candidate Jeanette Jara and right-wing populist Republican Party of Chile (PRCh) leader Jose Antonio Kast. Data from Polymarket shows an overall implied probability of 81% that the 14 December run-off will be between Jara and Kast, the latter of whom was defeated by incumbent left-wing President Gabriel Boric in the 2021 run-off by a margin of 56%-44%. More here:

DATA

UK DATA (MNI): Labour Data Soft Across the Board

- UK SEP AWE PRIVATE REGULAR PAY +4.17% 3MO Y/Y (VS +4.43% AUG)

- UK SEP 3MO EMPLOYMENT CHANGE -22K (VS +91K AUG)

- UK OCT PAYE PAYROLLS TOTAL EMPLOYEES 30.27M (VS 30.30M SEP)

- UK SEP UNEMPLOYMENT RATE 4.97% (VS 4.83% AUG)

- UK OCT PAYE MEDIAN PAY +3.1% Y/Y (VS +5.9% SEP)

Private regular pay is a bit softer than expected at 4.17% Y/Y in the 3-months to September (BOE forecast 4.23%). This still rounds to 4.2% in line with expectations, however. This is due to a soft single month figure of 3.79% Y/Y, while the revision to August is very small (from 4.21% to 4.23% Y/Y). The unemployment rate was also higher than expected at 4.97% against the expected 4.87% from the BOE and 4.9% consensus. 3-month LFS employment change -22k (expected broadly flat). The revisions to PAYE payrolls are in a negative direction (last September revised to -32k from -10k) with the flash October number also at -32k (expected broadly flat). This puts the 3-month change at -54k (the 3-months to Sep revised to -23k from flat).

Looking into the details of the AWE data there have been slowdowns in all the single month Y/Y growth and it looks like a relatively broad slowdown in wage growth: Construction to 2.87% Y/Y from 3.94% Y/Y - the lowest single month print since May 2024 and the lowest 3-month print also since May 2024 (at 3.49% Y/Y). Manufacturing to 4.10% Y/Y from 4.66% Y/Y - lowest single month since May 2022 and lowest 3-month print since July 2022 (at 4.39% Y/Y). Finance and business services to 2.29% Y/Y - the lowest single month print since July 2020 and lowest 3-month print since August 2020 (at 2.74% Y/Y).

UK DATA (MNI): BRC Retail Sales Values Only Increase Y/Y Due to Food Inflation

- UK BRC OCT BY VALUE SHOP SALES LFL +1.5% Y/Y, TOTAL +1.6%

BRC Retail Sales slowed again in October, posting a 1.6% Y/Y increase in value terms (vs 2.3% September). The year-on-year growth in the value of retail sales was the weakest since May and was almost entirely driven by food sales, which in turn were almost entirely driven by food price inflation. Food sales rose at a slower pace than September, rising 3.5% Y/Y (vs 4.3%). Again, the press release noted that the positive figure "was mostly driven by higher prices rather than higher volumes". The year-on-year rate is now at its lowest since May, but we note that the BRC shop price index and official ONS data both show a slowdown in food price inflation recently, so its hard to know how whether there is much of a slowdown here in volume terms.

JAPAN DATA (MNI): Current Account Surplus Surges on Income Inflows, But May Not Aid Yen

Japan Sep trade and current account balance data were stronger than forecast, particularly on the current account side. In unadjusted terms we printed 4483.3bn, versus 2456.6bn projected and 3701.4bn prior. In seasonally adjust terms we were at 4347.6bn for the current account, close to double the consensus projection and prior outcome. This is the best outcome for at least a few decades. This isn't necessarily a yen positive though, at least based off recent correlations. Current account shifts haven't coincided with yen shifts in recent years.

JAPAN DATA (MNI): Japan Oct Sentiment Posts 6th Straight Rise

Japan’s Economy Watchers sentiment index rose for a sixth consecutive month in October, prompting the government to upgrade its assessment from the previous month, data released by the Cabinet Office on Tuesday showed. The index for the current economic climate stood at a seasonally adjusted 49.1 in October, up from 47.1 in September, while the outlook index for two to three months ahead climbed 4.6 points to 53.1 from 48.5. The outlook index also posted a sixth straight month. Sentiment improved across households, businesses, and the labour market.

AUSTRALIA DATA (MNI): NAB Survey Signals Ongoing Recovery & Lower Inflation

NAB business confidence and conditions were little changed in October with the former down 1 point to +6 and the latter up 1 point to +9. The survey details were generally positive though with forward orders positive and their highest in two and a half years, investment up, labour demand steady and cost/price increases moderating. It is consistent with an ongoing economic recovery and contained inflation and therefore the RBA on hold.

AUSTRALIA DATA (MNI): Westpac Consumer Details Mixed, Spending Rise Not a Given

The details of the November Westpac consumer confidence survey are mixed signalling that there could be payback in December. It rose despite lower sentiment amongst mortgage holders as a group and less optimism regarding the labour market outlook but stronger domestic growth and less risk from US tariffs seemed to have driven the rebound into net optimism territory. Westpac asked about Christmas spending intentions and 15% said they would spend more than last year up from 11.6% in November 2024 with around 35% planning to spend less, similar to 2024.

NEW ZEALAND (MNI): Inflation Expectations Stable, RBNZ on Track for November Cut

The RBNZ's Q4 survey of expectations posted unchanged inflation expectations. The central bank is likely to be relieved that not only are they within its 1-3% target band but they didn't increase in the latest reading following the rise in Q3 CPI to 3.0% y/y from 2.7%, although the RBNZ's measure of core held steady at 2.7%. The RBNZ has maintained for some time that the Q3 increase would be temporary and its August projections showed inflation moderating from Q4 and approaching the band midpoint in 2026 given the degree of spare capacity in the economy.

FOREX: GBP Pressured by UK Data, US-Swiss Trade Deal Buoys CHF

- The US Senate has passed a funding package to reopen the US government, sending it to the house which should allow for a reopening on Wednesday. The USD index has been consolidating around the 99.50 mark as details surrounding the release of US tier-one data is awaited. This left country-specific drivers in focus, with soft UK labour market data prompting GBP downside while CHF outperforms on optimism for a US-Swiss trade deal.

- A December BoE cut is now 80% and renewed downward pressure for GBPUSD looks set to snap a four-day winning streak for the pair. The bounce fell short of initial resistance at 1.3231, the 20-day EMA. Moving average indicators continue to signal a bearish trend, potentially strengthening the narrative that recent gains could be considered corrective.

- CHF outperforms following late yesterday's optimism on a potential Swiss trade deal with the US. While such a deal would be unlikely to sway SNB rates this year or the next, it should see a moderate upwards revision of 2026 GDP forecasts for the country. EURCHF sees downside pressure as a function of that at 0.9287. Key medium-term support for the pair remains at the clustered lows between 0.9206/22.

- Despite firmer consumer confidence data, AUD has reversed a touch lower this morning, eroding a small portion of the impressive gains Monday. This has allowed AUDNZD to edge lower, with the 2013 highs at 1.1586 broadly holding. Initial support for the cross moves up to 1.1513.

- Two ECB speakers as well as Norges Bank's Wolden Bache are scheduled for the rest of the day.

EGBS: 2.70% Figure is Containing Upside in 10-year Bund Yields For Now

10-year Bund yields remain below the 2.70% figure that contained upside yesterday. A move back towards the 2.80% seen in early September may require increased conviction that the ECB’s easing cycle has concluded, alongside durable signs that the ramp-up in German fiscal spending and associated issuance is underway heading into 2026.

- The German curve has lightly bear steepened today, with 5s30s up 0.5bps to 99.6bps. 5s30s has struggled to consolidated above the 100bp figure over the last two months. EUR swap rates are little changed on the session. The multi-week move higher in EUR 10-Year swap rates (from a low of 2.525% to a high of 2.715%) seems to have stalled.

- Bund futures are -10 ticks at 129.03 amid fairly light cumulative volumes of under 200k. Spillover from this morning's UK labour market data was worth about 10 ticks of upside in Bunds. A short-term bear cycle remains intact, with support seen at 128.80 (yesterday's low) and 128.70 (Oct 10 low).

- European equity futures are up 0.4%, which sees 10-year EGB spreads to Bunds marginally narrower on the session.

- The Netherlands sold E2.41bln of the 2.50% Jul-35 DSL this morning.

- There’s been a flurry of ECB speak from Elderson, Sleijpen, Kocher and Vujcic today. None have been particularly noteworthy. The bar to the median Governing Council supporting another cut is increasing, particularly after stronger-than-expected growth signals in recent weeks.

- The November ZEW survey was weaker-than-expected (expectations component 38.5 vs 41.0 cons, 39.3 prior), but had no market impact. It is a survey of investors so often exhibits corelations with stock market movements.

GILTS: Bull Steepening on Soft Labour Data, Over 80% Odds of Dec BoE Cut Priced

Gilts have rallied on the back of this morning’s soft labour market data.

- Futures trade as high as 93.72.

- Resistance at the Nov 4 high/bull trigger (93.98) untested, with technical parameters remaining bullish and the recent pullback deemed corrective.

- Yields 5-7bp lower, curve bull steepens.

- 2-Year gilt yields print the lowest level since August ’24 (3.732%).

- Fresh extension lower would target the 22 August ’24 low (3.653%).

- The 2s10s curve is ~6bp off its October low, last ~66.5bp. Uptrend support drawn off the August ’23 lows remained intact during October/early November. We detailed steepening risks for that curve in the early part of last week.

- SONIA futures little changed to +7.0, SFIZ6 year-to-date highs (96.700) intact.

- BoE-dated OIS prices ~21bp of easing for December, 30bp through February and 39bp through March.

- BoE Governor Bailey is viewed as the key swing voter. This morning’s data increases the odds of him voting for a December cut.

- We believe that volatility around non-Bailey MPC speeches is likely to be much reduced ahead of the Budget on Nov 26, given the entrenched views of other MPC members.

- This certainly held true as MPC hawk Greene reiterated her previously aired areas of focus this morning, having no impact on the short end & gilts.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.762 | -20.7 |

Feb-26 | 3.667 | -30.3 |

Mar-26 | 3.579 | -39.0 |

Apr-26 | 3.469 | -50.1 |

Jun-26 | 3.423 | -54.7 |

Jul-26 | 3.369 | -60.1 |

Sep-26 | 3.345 | -62.4 |

EQUITIES: Trend Condition in E-Mini S&P Bullish Despite Breach of 50-Day EMA

A medium-term bull trend in Eurostoxx 50 futures remains intact and recent weakness appears to have been a correction. Price has managed to find support below two important price points; the 50-day EMA, at 5580.70, and 5577.00, the base of a bull channel drawn from the Aug 1 low. A clear break of both levels would strengthen a bear theme and highlight a stronger reversal. Sights are on the bull trigger at 5742.00, the Oct 29 high. The trend condition in S&P E-Minis remains bullish and the pullback since the Oct 30 high appears corrective. The contract has managed to find support below the 50-day EMA, currently at 6716.03 and a key support. Friday’s activity also highlights a potential reversal signal - a bullish doji candle. This defines key support at 6655.50, the Oct 7 low. A continuation higher would signal the end of a correction and open 6953.75, Oct 30 high and bull trigger.

- Japan's NIKKEI closed lower by 68.83 pts or -0.14% at 50842.93 and the TOPIX ended 4.16 pts higher or +0.13% at 3321.58.

- Elsewhere, in China the SHANGHAI closed lower by 15.839 pts or -0.39% at 4002.758 and the HANG SENG ended 47.35 pts higher or +0.18% at 26696.41.

- Across Europe, Germany's DAX trades higher by 43.61 pts or +0.18% at 24004.77, FTSE 100 higher by 82.95 pts or +0.85% at 9870.23, CAC 40 up 53.2 pts or +0.66% at 8108.98 and Euro Stoxx 50 up 31.22 pts or +0.55% at 5695.69.

- Dow Jones mini down 32 pts or -0.07% at 47430, S&P 500 mini down 15 pts or -0.22% at 6841.75, NASDAQ mini down 101.5 pts or -0.39% at 25613.5.

Time: 10:00 GMT

COMMODITIES: Recent Weakness in WTI Futures Appears to Be a Flag Formation

Recent weakness in WTI futures appears to be a flag formation - a bullish continuation pattern. This suggests that an upward corrective cycle remains intact for now. Price has recently traded through the 50-day EMA, at $60.84, signalling scope for a stronger recovery. Note too that resistance at $62.34, the Oct 8 high, has been pierced. A clear move through it would expose key resistance at $65.77, Sep 26 high. The bear trigger is $55.96, the Oct 20 low. The downleg in Gold since Oct 20 appears to have been a correction and has allowed an overbought condition to unwind. Recent gains also suggest the correction is over. Price remains above a key support at the 50-day EMA, at $3890.0.0. Clearance of this EMA would signal scope for a deeper retracement. Initial resistance is at $4161.4, the Oct 22 high. A stronger recovery would refocus attention on $4381.5, the Oct 20 high and bull trigger.

- WTI Crude up $0.31 or +0.52% at $60.43

- Natural Gas down $0.04 or -0.9% at $4.299

- Gold spot up $26.6 or +0.65% at $4142.81

- Copper down $3 or -0.59% at $507.5

- Silver up $0.44 or +0.86% at $50.9589

- Platinum up $21.06 or +1.34% at $1594.96

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 11/11/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 11/11/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 11/11/2025 | 1200/1200 | BOE APF Quarterly Report | ||

| 11/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 11/11/2025 | 0325/2225 | Fed Governor Michael Barr | ||

| 12/11/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/11/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/11/2025 | 0900/1000 | * | Industrial Production | |

| 12/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 12/11/2025 | 1045/1145 | ECB Schnabel Speech at BNP Paribas | ||

| 12/11/2025 | 1140/1240 | ECB de Guindos at FIBI International Banking Conference | ||

| 12/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 12/11/2025 | 1205/1205 | BOE Pill in Panel at International Monetary Research Conference | ||

| 12/11/2025 | - | *** | Money Supply | |

| 12/11/2025 | - | *** | New Loans | |

| 12/11/2025 | - | *** | Social Financing | |

| 12/11/2025 | - | ECB Lagarde, Cipollone at Eurogroup Meeting in Brussels | ||

| 12/11/2025 | - | BOE MPG Meeting | ||

| 12/11/2025 | 1330/0830 | * | Building Permits | |

| 12/11/2025 | 1420/0920 | New York Fed's John Williams | ||

| 12/11/2025 | 1500/1000 | Philly Fed's Anna Paulson | ||

| 12/11/2025 | 1505/1005 | Kansas City Fed's Jeff Schmid | ||

| 12/11/2025 | 1520/1020 | Fed Governor Chris Waller | ||

| 12/11/2025 | 1730/1230 | Fed Governor Stephen Miran | ||

| 12/11/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 12/11/2025 | 1830/1330 | Bank of Canada meeting minutes | ||

| 12/11/2025 | 2050/1550 | New York Fed's Roberto Perli | ||

| 12/11/2025 | 2100/1600 | Boston Fed's Susan Collins |

Note: US Government shutdown ongoing, meaning any Government-compiled US statistics will not be released.