MNI US OPEN - US Govt Funding Package Clears Rules Committee

EXECUTIVE SUMMARY

- U.S. FEDERAL DATA RE-OPENING 2025: FAQS

- FUNDING PACKAGE CLEARS RULES COMMITTEE, FINAL VOTE EXPECTED AFTER 16:00 ET

- SPECULATION SWIRLS OVER POTENTIAL CHALLENGE TO PM STARMER

- WHITE HOUSE EXPLORES RULES THAT WOULD UPEND SHAREHOLDER VOTING: WSJ

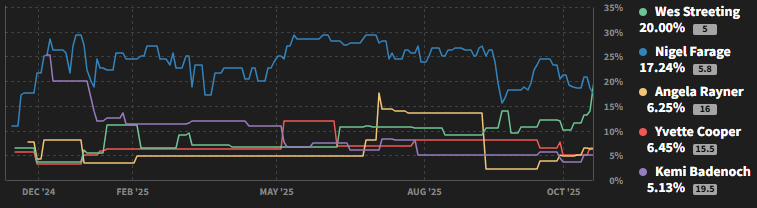

Figure 1: 'Next Prime Minister To Replace Keir Starmer' - betting market implied odds

Source: Smarkets

NEWS

US (MNI): U.S. Federal Data Re-Opening 2025: FAQs

With the U.S. federal government shutdown that began Oct 1 set to end later this week, dozens of postponed government agency data reports are due to be rescheduled for release over the coming weeks and months. Some may be cancelled altogether. We go through the prospects for major data releases over the coming weeks in the attached PDF. MNI’s rough estimates are in the table included in the link – we will publish updates to the official calendar as and when they are announced in the coming days.

US (MNI): Govt Funding Package Clears Rules Committee, Final Vote Expected After 16:00 ET

The House Rules Committee voted 8-4 along party lines to advance the Senate-passed government funding package to the floor of the House of Representatives, clearing a key procedural hurdle to reopening the government. The rule sets one hour of debate on the bill, followed by a final vote. The House will hold its first votes since September 19 at 16:00 ET 21:00 GMT. As the shutdown impasse was ended with the votes of eight 'rebel' Democrat Senators, the underlying conflict remains unresolved. If lawmakers fail to complete the remaining nine annual bipartisan spending bills by the new January 30 deadline, there is a risk of a second shutdown in February.

US (WSJ): White House Explores Rules That Would Upend Shareholder Voting

The White House is exploring new measures to curb the influence of proxy advisers and index-fund managers, wading into a hot-button debate raised by high-profile CEOs including Elon Musk and Jamie Dimon in recent months. Trump administration officials are discussing at least one executive order that would restrict proxy-advisory firms such as Institutional Shareholder Services and Glass Lewis, people familiar with the matter said. That could include a broad ban on shareholder recommendations or an order blocking recommendations on companies that have engaged proxy advisers for consulting work, the people said.

US (WSJ): The Fed Is Increasingly Torn Over a December Rate Cut

The path for interest-rate cuts has been clouded by an emerging split within the central bank with little precedent during Federal Reserve Chair Jerome Powell’s nearly eight-year tenure. Officials are fractured over which poses the greater threat—persistent inflation or a sluggish labor market—and even a resumption of official economic data may not bridge the differences.

FED (BBG): Fed’s Barr Calls for Guardrails as Financial Sector Adopts AI

Federal Reserve Governor Michael Barr said there needs to be clear guardrails to prevent risks as the financial sector looks to adopt artificial intelligence in its core functions. Regulators need to get the balance right between innovation and stability to ensure that AI boosts growth and productivity over the long-term, Barr said at the Singapore FinTech Festival on Wednesday.

UK (The Guardian): Starmer Allies Issue Warning to PM’s Rivals as Fears Grow Over Leadership Challenge

Downing Street has launched an extraordinary operation to protect Keir Starmer amid fears among the prime minister’s closest allies that he is vulnerable to a leadership challenge in the wake of the budget. Starmer’s most senior political aides warned that any attempt to oust the prime minister over tanking poll ratings would be a “reckless” and “dangerous” move that could destabilise the markets, international relationships and the Labour party.

UK (MNI): Even w/Streeting Denial, Speculation Swirls Over Potential Starmer Challenge

Secretary of State for Health Wes Streeting has reiterated that he "hopes the prime minister [Sir Keir Starmer] leads Labour into the next general election." Doing the morning media rounds, Streeting issues a non-binding commitment not to launch a leadership challenger, saying to the BBC, "I cannot see the circumstances in which I would do that [mount a leadership challenge] to our prime minister". Even if there is no credence to the rumours of Streeting launching a challenge, the furore will nevertheless raise speculation about the PM's position as the budget approaches in two weeks.

ECB (MNI): ECB Transmission Uneven Across Incomes - Bulletin

Tighter monetary policy had an uneven impact across households in the euro area, with lower-income families maintaining or even increasing borrowing despite less favourable conditions, the European Central Bank's latest Economic Bulletin pre-release notes. According to Consumer Expectations Survey analysis , lower-income households increased applications for consumer credit from 2022 onwards, while higher-income families curtailed demand for both consumer and mortgage loans, the bulletin said on Wednesday.

RUSSIA/UKRAINE (MNI): Foreign Ministry-Russia Ready to Resume Istanbul Talks w/Ukraine

State-run TASS reports that, according to the head of the Russian Foreign Ministry's department, Russia is ready to resume talks with Ukraine in Istanbul. This confirms reporting last night from TASS, who carried comments from Russia's Chargé d'Affaires in Turkey, Alexei Ivanov, saying that "The Russian side has repeatedly emphasised that we are ready to continue direct negotiations with the Ukrainian side, with the Ukrainian delegation," adding, "If Kyiv demonstrates political will, we are ready for such negotiations at any time.

CHINA (MNI EXCLUSIVE): China Promotes FX Hedging as Yuan Swings Seen Growing

Chinese economists, exporters and officials discuss the outlook for FX hedging. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI): China Willing to Increase Spanish Imports - Xi

MNI (Beijing) China is willing to increase imports of high-quality Spanish products and cooperate in emerging fields such as new energy, President Xi Jinping told King Felipe VI of Spain during a meeting on Wednesday in Beijing, central state media outlet Xinhua has reported. China will continue its visa-free policy for Spanish citizens, Xi added.

RBA (BBG): RBA Warns of Market Complacency Toward Rising Geopolitical Risks

A senior Reserve Bank of Australia official warned that markets may be underestimating geopolitical and macroeconomic risks at a time when the global financial system is showing early signs of fragmentation. Speaking at the Association of Superannuation Funds of Australia conference in Broadbeach, Queensland, on Wednesday, RBA Assistant Governor Brad Jones pointed to “emerging evidence” of divergence in how central banks manage reserves — particularly through surging gold holdings among a small group of countries.

BOK (BBG): BOK’s Rhee Says Policy Moves Including Direction Depend on Data

Bank of Korea Governor Rhee Chang Yong signaled that while the central bank remains in an easing cycle, the timing and size of any future rate moves — or the direction of policy — may shift depending on forthcoming data. “Given the negative output gap, our official position is that we will maintain the easing monetary cycle,” Rhee said in an interview Wednesday with Bloomberg TV’s Haslinda Amin in Singapore. “But the magnitude and timing of the cut or even the change of direction will depend on the new data that we’ll see.”

INDIA (BBG): Exit Polls Show Modi Poised for Bihar Win After Tough Year

Prime Minister Narendra Modi’s alliance is leading in exit polls from elections in one of India’s poorest yet politically-pivotal states, suggesting a possible boost for the Indian leader after a year marked by economic headwinds and foreign policy challenges. In the eastern state of Bihar, where voting in local polls concluded on Tuesday, Modi’s Bharatiya Janata Party and its key regional ally, Janata Dal (United), are projected to win between 130 to 167 seats with the majority mark at 122 seats, according to forecasts. The main opposition alliance comprising of the Indian National Congress and some other regional parties is expected to secure between 70 to 108 seats.

SOUTH AFRICA (MNI): MTBPS Preview - November 2025

It will be another balancing act from Finance Minister Enoch Godongwana, as he treads a tightrope between stimulating growth and promoting fiscal consolidation, but in various respects he is arguably in a more comfortable position than a few months ago. The November Medium-Term Budget Policy Statement (MTBPS) is widely expected to reflect an improved fiscal position and a brighter fiscal outlook, with little sign of infighting among GNU partners over the upcoming mini budget. Godongwana may also provide formal updates on key policy measures, including a fiscal anchor and a lower SARB inflation target.

DATA

GERMANY DATA (MNI): German Services Ex-Airfares CPI Contribution Shrinks

- GERMAN OCT FINAL CPI +2.3% Y/Y, +0.3% M/M

- GERMANY OCT FINAL HICP +2.3% Y/Y, +0.3% M/M

German final October HICP was unrevised from the flash readings at 2.3 Y/Y (2.4% in Sep) and 0.3% M/M. The final reading to CPI was also unrevised at 2.3% Y/Y (2.4% in Aug) and 0.3% M/M whilst core CPI remained at 2.8% Y/Y. Details point towards the services upside surprise in the country being airfares-driven, taking away from its relevance for the ECB. Services accelerated to 3.5% Y/Y (confirming the flash reading) for its highest rate since April, adding 0.04pp to headline inflation in October. Goods inflation meanwhile more than negated that, with a 0.13pp lower contribution to headline, mostly on the back of both lower food and energy Y/Y.

ITALY DATA (MNI): Underlying IP Momentum Sluggish, But Surveys Suggest Improvements

Italian industrial production rebounded in September, rising 2.8% M/M, well above the 1.5% consensus. August's already weak reading was revised down to -2.7% (vs -2.4% initial). Stripping out the monthly volatility, which may be a function of seasonal factors, IP momentum remains sluggish. That said, sentiment data points towards a gradual recovery in the months ahead. On a 3m/3m SWDA basis, production was down 0.5% in September, after a 0.6% fall in August.

SWEDEN DATA (MNI): Signs of Labour Market Improvements in October PES Data

The Swedish labour market is showing signs of improvement, according to Public Employment Service data for October. This shouldn't impact the Riksbank outlook - it's rather confirming that the current policy stance is supporting the economic recovery. The policy rate is expected to remain at 1.75% for "some time". However, we continue to think that the risk of a hike back to 2% is greater than the risk of another cut over a 12-month horizon. The unemployment claims rate fell a tenth to 6.8%, the lowest since July 2024.

AUSTRALIA DATA (MNI): Strong Home Lending May Contribute to Extended RBA Hold

There was a strong rise in the number of new dwelling loans and their value in Q3 as house price inflation rose. The recovery in home lending began in Q2 after the RBA began easing in February and the 75bp to August appears to have contributed to the sharp rise. The Board is unsure how restrictive policy is and remains cautious. It noted this month that "the housing market is continuing to strengthen, a sign that recent interest rate reductions are having an effect". The lending data is consistent with this and likely to add to its caution about easing further.

FOREX: USDJPY Uptrend Extends, Ignoring Verbal Warnings

- The Japanese yen has weakened again Wednesday, with USDJPY’s move higher notable given further FX jawboning from Finance Minister Katayama, who reiterated authorities are closely watching FX moves with a high sense of urgency.

- This has led USDJPY to erase the ADP-driven losses from Tuesday, and then accelerate through 154.50, a level that had been holding across early November. Furthermore, 154.80 has also been cleared, placing the pair at the highest level since February. This puts sights on 155.35, a Fibonacci projection. A number of cross-Yen also stand at noteworthy levels, CHFJPY for example sees fresh all-time highs at 193.82.

- EURCHF (-0.23%) sees further downside pressure as a function of the looming US-Swiss trade deal, to session lows of 0.9246 at typing. This keeps the extremely significant support cluster between 0.9206-22 for EURCHF in high focus for those looking for a break to the lowest levels since the peg removal in 2015. Meanwhile USDCHF (-0.15%) has tracked further back below the 0.8000 handle.

- Internal criticism from a senior Labour party member weighed on GBP this morning, followed by a sudden move lower that may have been flow or fix related. On net, GBPUSD sits at 1.3118, with first support and the bear trigger for the pair at 1.3010, the Nov 4 and 5 lows.

- US MBA Mortgage applications as well as Canada building permits highlight the data calendar today. A set of Fed speakers is scheduled for today, while ECB's de Guindos and BoE's Pill are also set to speak but likely won't move the needle. The US government is expected to reopen tomorrow if the House expectedly signs the deal on that today.

EGBS: Regional Equity Rally Weighing on Bund Futures

- A short-term bear cycle in Bunds remains intact, with initial resistance at 129.31 (20-day EMA) untested. Intraday, Bunds are down 13 ticks at 129.10. With market moving headline flow light, Bunds appear to be taking cues from the 1% uptick in European equity futures.

- German yields are up to 1bp higher today, and 20/30-year Bund supply is now in the rear view. Results were generally acceptable, though the 30-year line saw slightly weaker demand metrics than the 20-year.

- Ahead of the supply, we saw what looked to be an RX/UB steepener trade in futures (~E325k DV01), which helped German 10s30s to a session high of ~59.5bps.

- 10-year EGB spreads to Bunds have narrowed as a result of the equity rally. OATs outperform, with the 10-year spread to Bunds down 2bps to ~74.5bps – the lowest since August,

- The EUR 10s30s swap curve has steepened almost 7bps since October 30, and is on track for a fresh cycle closing high at ~29bp. Confirmation of/reiterations surrounding the transition plans of large Dutch pension funds has reignited steepener interest, albeit with positioning in these trades already deemed to be somewhat heavy. 30bp presents the next obvious area of upside interest, followed by the Oct 7 ’21 closing level (35.03bp).

- German final October HICP confirmed flash estimates at 2.3% Y/Y, while Italian industrial production rebounded in September, rising 2.8% M/M, well above the 1.5% consensus.

- ECB’s de Guindos is scheduled to speak later this morning. We don’t expect any new signals.

GILTS: Bear Steepening, Questions Surrounding PM's Future Dominate

Gilts hold lower and trade wider. vs. Bunds across the curve.

- Futures -37 at 93.50 vs. lows of 93.46. Key resistance at 93.98 held yesterday but bulls remain in technical control.

- Yields 2-4bp higher, curve steepens. 2s10s extends the recovery from October lows after uptrend support held.

- Gilt/Bunds +2bp at 175bp.

- Rumours surrounding a potential leadership challenge within the ruling Labour Party, presence of syndicated gilt supply (albeit I/L, with books now closed) and the bid in equities seem to be the driving factors.

- The former seems to be the key differentiator and driver of gilt widening vs. Bunds, particularly given the proximity to the Budget (November 26) and recent reduction in UK political & fiscal risk premia.

- Note that Health Secretary Streeting played down suggestions that he is planning to challenge PM Starmer, but the furore will nevertheless raise speculation about the PM's position.

- BoE-dated OIS 0.5-2.0 bp less dovish vs. closing levels, showing 20bp of easing for December, 31bp through February, 40bp through March and 51bp through April.

- SONIA futures 0.25-3.0 lower, implied terminal rate pricing continues to hover around 3.30%.

- SFIZ6 and SFIZ5/Z6 registered incremental dovish cycle extremes yesterday.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.768 | -20.2 |

Feb-26 | 3.660 | -30.9 |

Mar-26 | 3.574 | -39.5 |

Apr-26 | 3.463 | -50.7 |

Jun-26 | 3.419 | -55.0 |

Jul-26 | 3.367 | -60.2 |

Sep-26 | 3.346 | -62.3 |

EQUITIES: This Week's Climb for Eurostoxx Reinforces Bullish Conditions

A medium-term bull trend in Eurostoxx 50 futures remains intact and this week’s gains reinforce bullish conditions. The contract has traded through resistance at 5742.00, the Oct 29 high to confirm a resumption of the uptrend. This paves the way for an extension towards 5777.41 next, a Fibonacci projection. On the downside, initial firm support is seen at 5655.99, the 20-day EMA. The trend condition in S&P E-Minis remains bullish and the bear leg since the Oct 30 high appears to have been a correction. The contract has managed to find support below the 50-day EMA, currently at 6722.19, and a key level. Activity on Nov 7 highlights a potential reversal signal - a bullish doji candle. This defines key support at 6655.50, the Oct 7 low. Sights are on 6953.75, Oct 30 high and bull trigger.

- Japan's NIKKEI closed higher by 220.38 pts or +0.43% at 51063.31 and the TOPIX ended 37.75 pts higher or +1.14% at 3359.33.

- Elsewhere, in China the SHANGHAI closed lower by 2.618 pts or -0.07% at 4000.14 and the HANG SENG ended 226.32 pts higher or +0.85% at 26922.73.

- Across Europe, Germany's DAX trades higher by 299.74 pts or +1.24% at 24387.14, FTSE 100 lower by 2.35 pts or -0.02% at 9897.22, CAC 40 up 73.29 pts or +0.9% at 8229.52 and Euro Stoxx 50 up 60.93 pts or +1.06% at 5786.63.

- Dow Jones mini up 77 pts or +0.16% at 48107, S&P 500 mini up 26.25 pts or +0.38% at 6897.75, NASDAQ mini up 173 pts or +0.67% at 25815.5.

Time: 10:00 GMT

COMMODITIES: Recent Gains Suggests Corrective Cycle for Gold is Over

The pullback in WTI futures since Oct 24, appears to be a flag formation - a bullish continuation pattern. This suggests that an upward corrective cycle is intact for now. Price has recently traded through the 50-day EMA, at $60.85, signalling scope for a stronger recovery. Note too that resistance at $62.34, the Oct 8 high, has been pierced. A clear move through it would expose key resistance at $65.77, Sep 26 high. The bear trigger is $55.96, the Oct 20 low. The downleg in Gold since Oct 20 appears to have been a correction and has allowed an overbought condition to unwind. Recent gains suggest the correction is over. Price remains above a key support at the 50-day EMA, at $3899.2. Clearance of this EMA would signal scope for a deeper retracement. Initial resistance is at $4161.4, the Oct 22 high. A stronger recovery would refocus attention on $4381.5, the Oct 20 high and bull trigger.

- WTI Crude down $0.58 or -0.95% at $60.47

- Natural Gas down $0 or -0.09% at $4.559

- Gold spot down $2.63 or -0.06% at $4124.23

- Copper up $0.2 or +0.04% at $506.75

- Silver up $0.56 or +1.08% at $51.787

- Platinum up $0.43 or +0.03% at $1587.14

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 12/11/2025 | 1045/1145 | ECB Schnabel Speech at BNP Paribas | ||

| 12/11/2025 | 1140/1240 | ECB de Guindos at FIBI International Banking Conference | ||

| 12/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 12/11/2025 | 1205/1205 | BOE Pill in Panel at International Monetary Research Conference | ||

| 12/11/2025 | - | *** | Money Supply | |

| 12/11/2025 | - | *** | New Loans | |

| 12/11/2025 | - | *** | Social Financing | |

| 12/11/2025 | - | ECB Lagarde, Cipollone at Eurogroup Meeting in Brussels | ||

| 12/11/2025 | - | BOE MPG Meeting | ||

| 12/11/2025 | 1330/0830 | * | Building Permits | |

| 12/11/2025 | 1420/0920 | New York Fed's John Williams | ||

| 12/11/2025 | 1500/1000 | Philly Fed's Anna Paulson | ||

| 12/11/2025 | 1505/1005 | Kansas City Fed's Jeff Schmid | ||

| 12/11/2025 | 1520/1020 | Fed Governor Chris Waller | ||

| 12/11/2025 | 1730/1230 | Fed Governor Stephen Miran | ||

| 12/11/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 12/11/2025 | 1830/1330 | Bank of Canada meeting minutes | ||

| 12/11/2025 | 2050/1550 | New York Fed's Roberto Perli | ||

| 12/11/2025 | 2100/1600 | Boston Fed's Susan Collins | ||

| 13/11/2025 | 0030/1130 | *** | Labor Force Survey | |

| 13/11/2025 | 0700/0700 | *** | UK Monthly GDP | |

| 13/11/2025 | 0700/0800 | *** | Final Inflation Report | |

| 13/11/2025 | 0700/0700 | ** | Trade Balance | |

| 13/11/2025 | 0700/0700 | ** | Index of Services | |

| 13/11/2025 | 0700/0700 | ** | Index of Production | |

| 13/11/2025 | 0700/0700 | ** | Output in the Construction Industry | |

| 13/11/2025 | 0700/0700 | *** | GDP First Estimate | |

| 13/11/2025 | 0700/0800 | *** | Final Inflation Report | |

| 13/11/2025 | 0730/0730 | BOE MPG Minutes Released | ||

| 13/11/2025 | 0930/0930 | Productivity Flash Estimates | ||

| 13/11/2025 | 1000/1100 | ** | EZ Industrial Production | |

| 13/11/2025 | 1200/1200 | BOE Greene in Panel on Central Bank Independence | ||

| 13/11/2025 | - | ECB de Guindos at ECOFIN Meeting in Brussels | ||

| 13/11/2025 | 1300/1400 | ECB Elderson Moderates Climate and Banks Panel | ||

| 13/11/2025 | 1300/0800 | San Francisco Fed's Mary Daly | ||

| 13/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 13/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 13/11/2025 | 1330/0830 | *** | CPI | |

| 13/11/2025 | 1530/1030 | Minneapolis Fed's Neel Kashkari | ||

| 13/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 13/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 13/11/2025 | 1700/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 13/11/2025 | 1700/1200 | ** | US DOE Petroleum Supply | |

| 13/11/2025 | 1715/1215 | St. Louis Fed's Alberto Musalem | ||

| 13/11/2025 | 1720/1220 | Cleveland Fed's Beth Hammack | ||

| 13/11/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 13/11/2025 | 1900/1400 | ** | Treasury Budget |

Note: Government-compiled US statistics may be impacted by US government shutdown