COMMODITIES: Recent Gains Suggests Corrective Cycle for Gold is Over

The pullback in WTI futures since Oct 24, appears to be a flag formation - a bullish continuation pattern. This suggests that an upward corrective cycle is intact for now. Price has recently traded through the 50-day EMA, at $60.85, signalling scope for a stronger recovery. Note too that resistance at $62.34, the Oct 8 high, has been pierced. A clear move through it would expose key resistance at $65.77, Sep 26 high. The bear trigger is $55.96, the Oct 20 low. The downleg in Gold since Oct 20 appears to have been a correction and has allowed an overbought condition to unwind. Recent gains suggest the correction is over. Price remains above a key support at the 50-day EMA, at $3899.2. Clearance of this EMA would signal scope for a deeper retracement. Initial resistance is at $4161.4, the Oct 22 high. A stronger recovery would refocus attention on $4381.5, the Oct 20 high and bull trigger.

- WTI Crude down $0.58 or -0.95% at $60.47

- Natural Gas down $0 or -0.09% at $4.559

- Gold spot down $2.63 or -0.06% at $4124.23

- Copper up $0.2 or +0.04% at $506.75

- Silver up $0.56 or +1.08% at $51.787

- Platinum up $0.43 or +0.03% at $1587.14

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

TARIFFS: Goldman On Tariff Passthrough Estimates (2/2)

- Goldman Sachs write that the customs duties implied US effective tariff rate “had risen by 9pp through August, or by nearly 11pp net of frontloading effects.”

- “Following recent tariff increases on some products and countries and hints of exemptions for others, we now expect it to rise by 12pp in total in 2025 and by another 3.5pp or 15.5pp in total through 2026, a bit less than we previously assumed.”

- They estimate that foreign exporters are “absorbing some of the tariff cost, unlike in 2019, though some of the decline likely reflects underreporting of import value to evade tariffs”. Meanwhile, passthrough to consumer prices has reached “55% after six months, meaningfully lower than at the same point in 2019.”

- They estimate that “US consumers would eventually absorb 55% of tariff costs, US businesses would absorb 22%, foreign exporters would absorb 18%, and 5% would be evaded.” US businesses are likely bearing a larger share currently though.

- GS estimate that “tariff effects have raised core PCE prices by 0.44% so far this year”. Their forecast, which assumed peak passthrough will rise from 55% to 70% “implies a further 0.6% boost from tariffs through next year”. That leaves core PCE inflation at 3.0% Y/Y in Dec 2025 and 2.4% in Dec 2026.

- To give an idea of sensitivity, core PCE inflation would be 3.1% and 2.7% respectively if passthrough peaks at 100%, or 2.9% and 2.2% if passthrough holds at 55%.

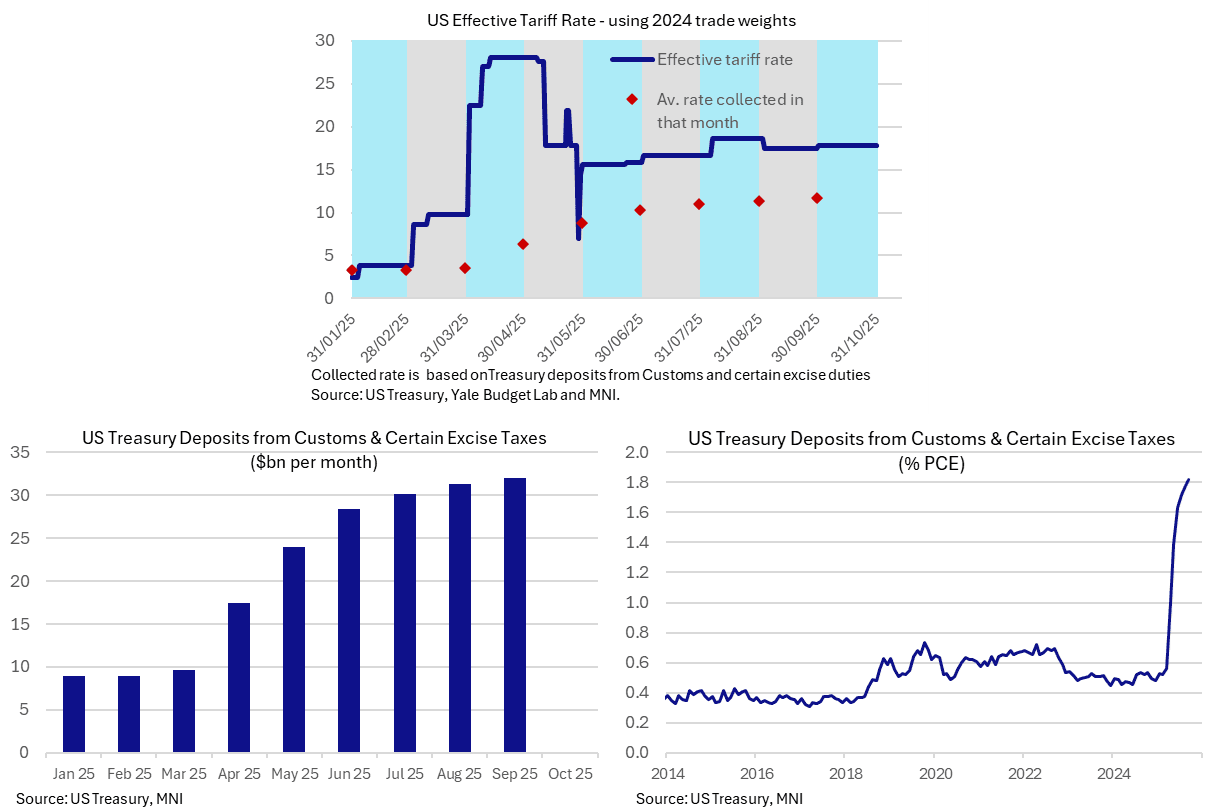

TARIFFS: Taking Stock Of Realized Tariff Rates After US-China Tensions (1/2)

- President Trump on Friday threatened new 100% tariffs on China and the imposition of its own export controls on “any and all critical software” on Nov 1 following China’s earlier export curbs on its rare earth metals.

- Trump has since appeared to downplay these threats, posting on Truth Social on Sunday “Don’t worry about China, it will all be fine! Highly respected President Xi just had a bad moment.”

- The speed with which apparent watering down of rhetoric has come after high tariff threats suggests low likelihood of effective tariff rates pushing north of 25% as was the case in April after Chinese retaliation to reciprocal tariffs sparked a surge in the China tariff rate to 145%. This of course is in a static sense as such levels of tariff rates are broadly seen as halting trade between the two countries.

- Nevertheless, it’s worth taking stock of latest tariff rates from both proposed rates and actual collection of customs duties.

- The latest Yale Budget Lab report from Sep 26 had an effective tariff rate of 17.4% at end-Sept, expected to have increased to 17.9% into October.

- Customs duties meanwhile have seen a stalling in progress in recent months, up to $32bn in September ($384bn annualized) after $31.3bn in Aug and $30.0bn in Jul. For context, this was in the $8-9bn region prior to the second Trump administration.

- It leaves an implied tariff rate either side of 11.5% depending on which period of trade you use for the denominator vs closer to 11.25% in Aug or 3.0% back in Dec.

- Alternatively, customs duties have increased by 1.3pps to ~1.8% of personal consumption expenditure, with most of this cumulative increase having come by June when it was worth an additional 1.1pp. These figures give an idea of the system-wide impact, whilst Goldman Sachs analysis in the second part of this post goes into detail as to how much might actually show up in consumer prices.

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Oct15 $1.1600(E1.2bln); Oct16 $1.1580-00(E3.4bln)

- USD/JPY: Oct15 Y143.00($1.8bln)

- AUD/USD: Oct14 $0.6500(A$1.0bln), $0.6580-00(A$1.2bln)