GOLD: Pause In Latest Rally, Range Of Fed Speakers Later Today

Gold reached a high of $4145.50/oz early in today’s APAC session but was then pressured by the strengthening of the US dollar (BBDXY +0.1%) and higher US equity futures (S&P e-mini +0.1%) after several days of gains. Bullion is now down 0.4% to $4108.7, after an intraday low at $4103.75. The market is watching US developments closely with a vote in the House of Reps to end the government shutdown due on Wednesday. How the delayed data print will impact the outlook for the Fed.

- The market is waiting for more information with around 17bp of easing priced in for the 10 December FOMC meeting and a full cut by January. Fed comments since the last decision have added uncertainty. There is a range of members speaking today. ADP data on Tuesday signalled labour market weakness.

- Our US analysts believe that the post-shutdown data schedule should be published next week with a risk that October CPI won’t be released. See their FAQ here.

- Silver is down 0.3% to $51.07 after falling to $50.873.

- Equities are mixed with the CSI 300 down 0.4% but the KOSPI up 0.7%. Oil prices are lower with WTI -0.3% to $60.85/bbl. Copper is down 0.3%.

- Later the Fed’s Barr, Williams, Paulson, Waller, Bostic, Miran and Collins speak as well as the ECB’s Schnabel and de Guindos. The Eurogroup meeting is taking place. There are no data of note.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Key Resistance For Futures Remains Intact, RBA Mins Tomorrow

Aussie bond futures are holding higher, but away from best levels. Important key resistance points remain intact. 3yr futures were last 96.47 (+7bps), while 10yr futures were at 95.685 (+7bps). Earlier highs were at 96.505 for the 3yr and 95.7050 for the 10yr. Some cap for futures has come from the softer US Tsy futures tone and better risk appetite trends more broadly, with US official comments showing reduced recent rhetoric around US-China trade issues (albeit still with the threat of higher tariff levels come Nov 1, per remarks by US President Trump).

- Short term resistance points for futures are as follows. For 3yr: RES 1: 96.615 - High Sep 12 , while for 10yr: RES 1: 96.615 - High Sep 12.

- Cash ACGB yields are around 6-7bps lower across the curve, with the front end slightly weaker in yield terms. The 33yr benchmark last 3.50%, while the 10yr was at 4.29%, with little change in the Au3/10s curve.

- The bias is likely to be fade this yield move in Aussie, given RBA comfort around the current macro backdrop. A risk remains from higher US tariff levels on China, export controls etc, which could see negative spill over to the Australian economic outlook. For the 3yr Aussie bond, moves under 3.45% may be faded.

- At this stage, per Polymarket, 100% tariff odds by Nov 1 sit at 17%.

- Looking ahead to tomorrow, the publication of the September 30 decision minutes will be important given the Board’s more cautious tone and Bullock avoiding to state what the current stance is. She also noted that Board is concerned about certain CPI components including market services. NAB’s September business survey also prints on Tuesday.

GOLD: Trade Jitters Drive Safe-Haven Flows, New Highs For Gold & Silver

Gold fell early in the APAC session to $4006.48/oz on comments from US President Trump suggesting that the US-China trade situation may not be as severe as implied on Friday. However, it didn’t last and concerns that the trade war could be reignited as well as a lower US dollar drove gold just above last Wednesday’s record to $4060.01, opening resistance at $4074.5, a Fibonacci projection. It is currently 1.0% higher at $4057.4.

- Silver has rallied strongly with prices up 2.3% to $51.47, close to the intraday high and above resistance and all-time high at $51.235. It is also above a Fibonacci projection at $51.405 opening round number resistance at $52.00. It has been boosted not just by trade-related safe-haven flows but also by constrained liquidity in London. In addition, it remains unclear if it will be excluded from US import duties.

- Regional equities have sold off with the Hang Seng down 3.5% and ASX -1.0% but S&P e-mini up 1.2%. Oil prices are higher with WTI +1.4% to $59.73/bbl. Copper is up 2.0%.

- Later the Fed’s Paulson speaks. The US bond market is shut but equities are open. IMF/World Bank meetings are taking place. The ECB’s Buch and BoE’s Mann and Greene speak. Germany’s September WPI prints.

NZD: Asia-Pac: NZD/USD Drifts Higher In Sympathy & Lower CNY Fix

The NZD/USD had a range of 0.5722 - 0.5745 in the Asia-Pac session, going into the London open trading around 0.5740, +0.30%. Some clarification from China over the weekend on their new rare earth export controls has seen the US walk back its aggressive stance and a more conciliatory tone is being set. I suspect a lot of Friday's moves will see some decent pullbacks on this, but how long it lasts is anybody's guess. The NZD has drifted higher from the open in sympathy to moves elsewhere and another very low CNY fix from the PBOC which has underpinned the move for now. The NZD had a poor weekly close though and technically remains a sell on rallies now for those looking for a currency to be short of in their basket. The sell zone remains back toward the 0.5800 area with the market looking for a potential move back towards the 0.5500/0.5600 area.

- MNI - Services & Manufacturing Indices Signal Ongoing Weak Q3 Activity. The BNZ services and manufacturing PMIs for September were consistent with the RBNZ’s assessment in its October statement that “economic activity recovered modestly in the September quarter”. Continued weak activity, including employment, at the end of the quarter is consistent with further RBNZ easing with policy likely to become stimulatory.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5850(NZD300m Oct 14), 0.5950(NZD312m Oct 16) - BBG

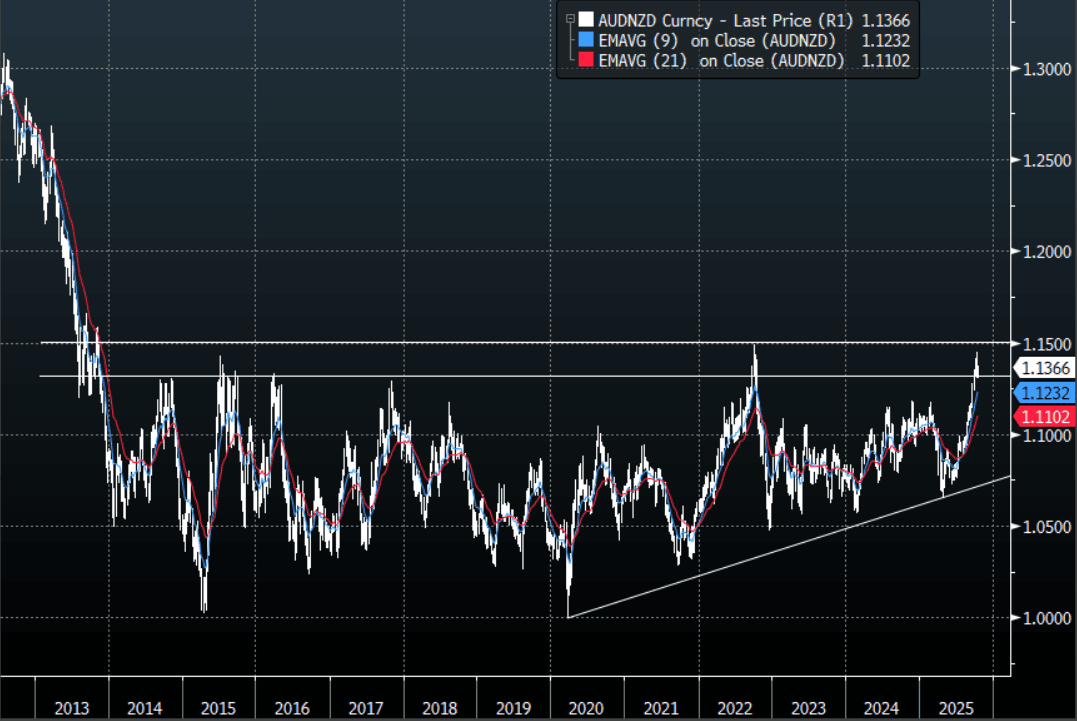

- AUD/NZD range for the session has been 1.1321 - 1.1373, currently trading around 1.1365. The Cross failed again above the 1.1400 area where I suspect initial paring back of longs. A clear sustained break above 1.15/1.16 resistance and the market will begin to think about levels back towards 1.2000 and above. Dips back toward 1.1200 should be a good place to start buying again if seen.

Fig 1: AUD/NZD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P