AUSTRALIA DATA: Strong Home Lending May Contribute To Extended RBA Hold

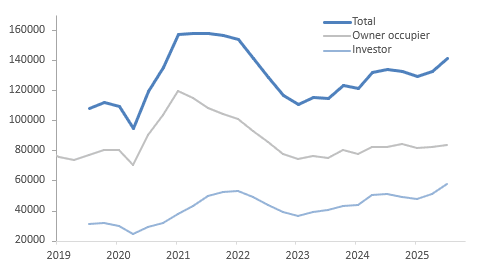

There was a strong rise in the number of new dwelling loans and their value in Q3 as house price inflation rose. The recovery in home lending began in Q2 after the RBA began easing in February and the 75bp to August appears to have contributed to the sharp rise. The Board is unsure how restrictive policy is and remains cautious. It noted this month that “the housing market is continuing to strengthen, a sign that recent interest rate reductions are having an effect”. The lending data is consistent with this and likely to add to its caution about easing further.

- The total number of home loans rose 6.4% q/q to be up 5.8% y/y driven by both owner occupiers and investors, but particularly the latter. Values increased 9.6% q/q to be 13.2% y/y higher as higher home prices added to the amount.

- Owner-occupier loans rose 2.0% q/q after 0.9% q/q to be +1.7% y/y with the growth split between first-time buyers (+2.3% q/q & 0.9% y/y) and others (+2.8% q/q & 3.3% y/y). The level is below that recorded in Q4 2024.

- The softness in owner-occupier lending compared to investors likely reflects poor affordability in the Australian housing market. Our affordability index has improved since Q2 2024 helped by higher incomes and lower rates but remains around 36% below trend and close to its series low.

- Loans to first-time homebuyers are likely to rise further in Q4 with the introduction of the government’s 5% deposit scheme.

- Investor loans soared 13.6% q/q after 5.9% in Q2 to be up 12.3% y/y with strength across states and territories.

No. of new loan commitments dwellings ex refi

Source: MNI - Market News/ABS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSTRALIA: RBA Events & September Jobs Data Week’s Key Events

September jobs data on Thursday and the RBA minutes Tuesday and Governor Bullock’s appearance early Thursday are the highlights this week. With markets pricing in less than a full rate cut by year-end, these events will be scrutinised to gauge how long the RBA may be on hold.

- RBA Governor Bullock appears in a fireside chat at the Nomura Research Forum in Washington DC at 1545 local time on Wednesday but 0645 AEDT Thursday.

- Tuesday’s publication of the September 30 decision minutes will also be important given the Board’s more cautious tone and Bullock avoiding to state what the current stance is. She also noted that Board is concerned about certain CPI components including market services.

- Other RBA events this week include Assistant Governor (Economic) Hunter speaking on Wednesday at 1030 AEDT and Assistant Governor Kent (Financial Markets) on Thursday at 0850 AEDT.

- Thursday also sees September employment which consensus expects to rise 20k with the unemployment rate rising 0.1pp to 4.3% but the participation rate steady at 66.8%. The August data had disappointed falling 5.4k but unemployment was steady at 4.2% and underemployment moderated further.

- NAB’s September business survey prints on Tuesday. Confidence and conditions appear to be recovering and with that employment too. The price/cost components remain important. The price of final products appears to have stabilised.

- Westpac’s lead indicator for September is released on Wednesday and has been signalling a slowdown in growth.

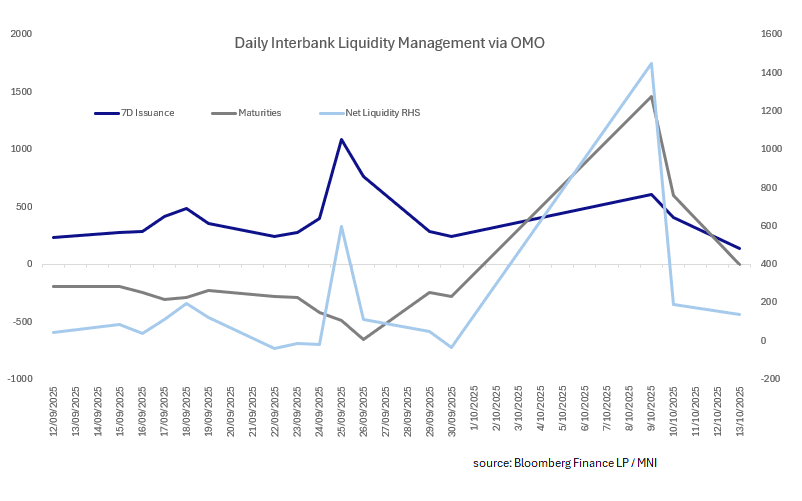

CHINA: Central Bank Injects CNY137.8bn via OMO

- The PBOC issued CNY137.8bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY 0 bn.

- Net liquidity injection CNY137.8bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.39%.

- The China overnight interbank repo rate is at 1.31%, from the prior close of 1.30%.

- The China 7-day interbank repo rate is at 1.40%, from the prior close of 1.35%.

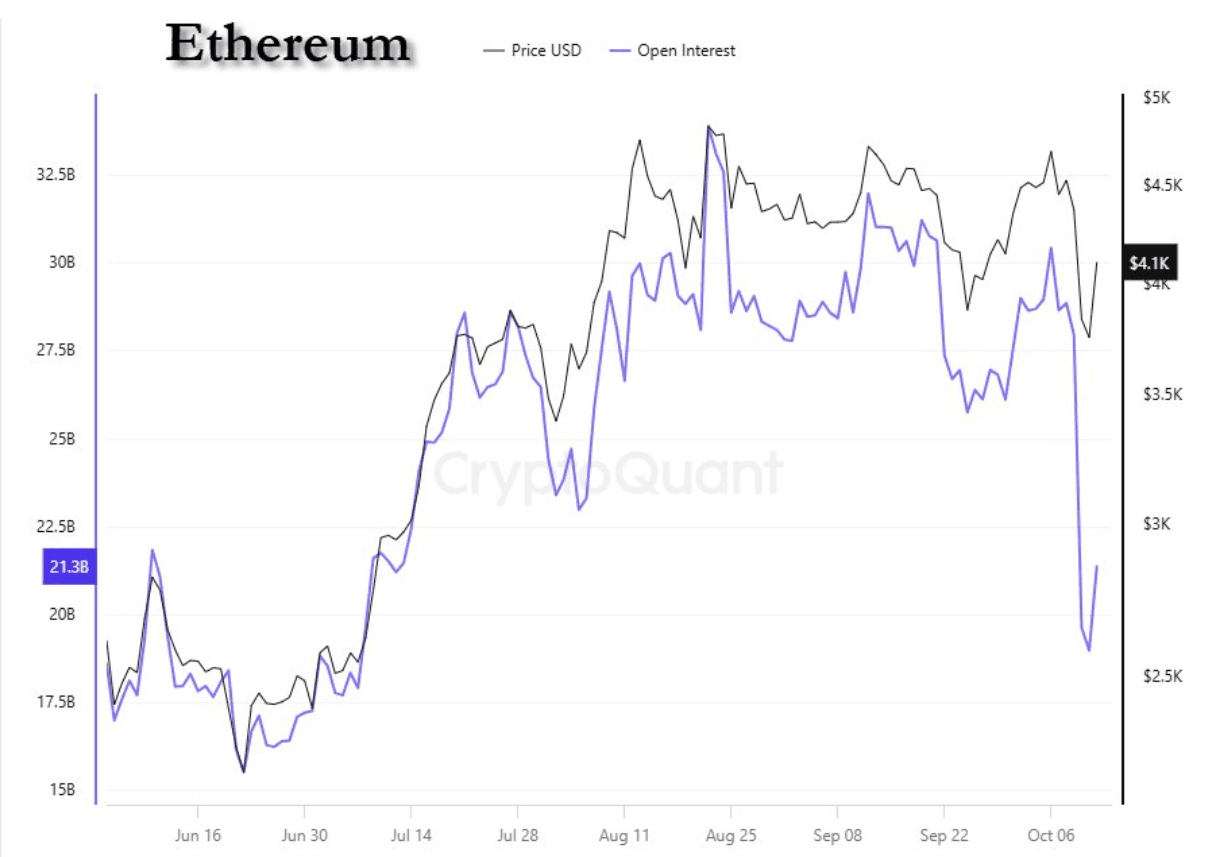

CRYPTO: Ethereum - Bounces But Can It Follow Through After Such A Wipeout ?

Ethereum had a range Friday night of $3489.99 - $4392.39, Asia is trading around $4150, +0.25%. Ethereum like the rest of Crypto capitulated on Friday down over 20% at its lows. The pullback from $3500 has been just as brutal as US/China rhetoric is seemingly being walked back. After what some have called the largest drawdown in Crypto history it is tough to think the market will just shrug this off and go straight back to making new highs. I suspect accounts that managed to stay in will use bounces to at least lighten up positioning until we truly understand how the US/China situation plays out.

- Look for some choppy markets as price tries to consolidate within a $3500-$4800 range.

- The price action certainly again highlights the risk for crypto investors in vehicles that promise liquidity which is always ample when people get in, but is never there when there is a need to exit. This is especially true for all the ALT-Coins who had even bigger write downs.

- The margin and leveraged accounts will have all been taken out, so where does that next wave of fevered buying come from which is needed to keep feeding the machine.

- Zerohedge posted on X: “Total annihilation of spec/levered positions”

Fig 1: Ethereum spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P