MNI US OPEN - US Expands Waiver for Russian Oil Purchases

EXECUTIVE SUMMARY

- US WAIVER FREES UP 19 MILLION BARRELS OF RUSSIA OIL FOR PURCHASE

- TRUMP CLAIMED IN G7 CALL THAT IRAN IS “ABOUT TO SURRENDER”: AXIOS

- CHINA, U.S. TO TALK IN FRANCE THIS WEEKEND

- US STARTS SECTION 301 PROBES RELATING TO FORCED LABOR

- JAPAN’S KATAYAMA SAYS IN CLOSER US CONTACT ON FX THAN USUAL

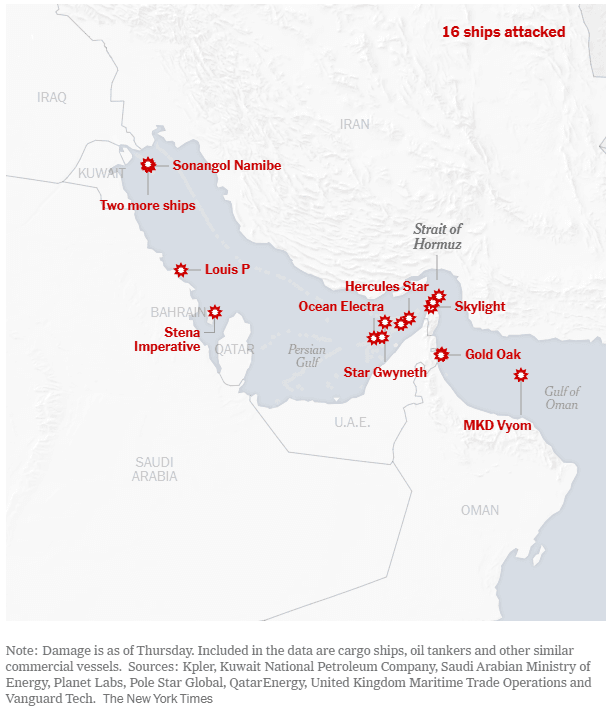

Figure 1: Where ships have been attacked in the Strait of Hormuz

Source: New York Times

NEWS

OIL (BBG): US Treasury Gives Green Light for Sale of More Russian Oil

The US has issued its second authorization for buyers to take Russian oil cargoes already at sea, widening a temporary waiver given last week to India alone in an effort to ease pressure on prices as the war in the Middle East continues. Treasury Secretary Scott Bessent, in a social media post, said the move was designed to be a “narrowly tailored, short-term measure” that “applies only to oil already in transit and will not provide significant financial benefit to the Russian government.”

OIL (BBG): US Waiver Frees Up 19 Million Barrels of Russia Oil for Purchase

Russian crude oil and fuel on about 30 tankers in Asian waters is potentially available for purchase after the US granted a temporary waiver to buy cargoes that were already at sea. The vessels are carrying at least 19 million barrels of Russian crude and 310,000 tons of refined products, according to ship-tracking data compiled by Bloomberg. The product is mainly naphtha — used to make plastics — and some diesel, prices of which have surged since Iran effectively closed the Strait of Hormuz.

US/IRAN (Axios): Trump Claimed in G7 Call That Iran Is “About to Surrender”

President Trump told G7 leaders in a virtual meeting Wednesday that Iran is "about to surrender," according to three officials from G7 countries briefed on the contents of the call. 24 hours later, Iran's new supreme leader issued his first public statement vowing to keep fighting. Trump is as confident about the war's outcome in private as he is in public. But his assessment is colliding with a more complex reality on the ground. The Iranian regime has shown no signs of imminent surrender or collapse — and on Day 14 of the war, is moving to gain more leverage by choking off the Strait of Hormuz. Trump boasted about the results of Operation Epic Fury on the G7 call Wednesday morning, telling allies, "I got rid of a cancer that was threatening us all."

US/IRAN (BBG): Trump Warns Iran to ‘Watch What Happens’ Today

“We have unparalleled firepower, unlimited ammunition, and plenty of time,” President Trump says of US attacks on Iran. “Watch what happens,” Trump warns Iran in a Truth Social post. “Iran’s Navy is gone, their Air Force is no longer, missiles, drones and everything else are being decimated, and their leaders have been wiped from the face of the earth,” Trump says

MIDEAST (WSJ): Israeli Officials Think Iran’s Regime Isn’t Likely to Fall Soon

Israeli officials now assess that Iran’s ruling regime is unlikely to fall in the immediate future, as Tehran’s battered rulers remain in control and conditions on the ground aren’t yet ripe for a popular uprising, people familiar with the matter said. Nearly two weeks into the war, Iran’s military and political leadership appears functional and responsive to events, while its domestic opponents have been cowed by a heavy security presence. Israeli officials assess that changing the equation would likely require many more weeks or months of fighting. Israeli Prime Minister Benjamin Netanyahu said on Thursday that he wasn’t sure if Iranians would be able to topple the Islamic republic although he said Israel was working to create the conditions that would allow for it.

US/CHINA (MNI): China, U.S. to Talk in France This Weekend

MNI (Beijing) Chinese Vice Premier He Lifeng will lead a delegation to France from March 14 to 17 to hold trade and economic negotiations with the U.S., according to a statement by the Ministry of Commerce on its website Friday. Both sides will conduct consultations on trade and economic issues of mutual concern, guided by the important consensus reached at the Busan summit and previous phone calls between the two heads of state.

US/CHINA (MNI): China to Watch U.S Section 301 Investigation: MOFCOM

MNI (Beijing) Beijing believes the U.S has no right to determine through Section 301 investigations whether a trading partner has overcapacity and impose unilateral restrictive measures, spokesperson of Ministry of Commerce told reporters on Friday. China will closely monitor the progress of the situation and reserves the right to take all necessary measures to safeguard its legitimate rights and interests, the Ministry said.

US (BBG): US Starts Section 301 Probes Relating to Forced Labor

United States Trade Representative initiated investigations of 60 economies under Section 301 (b) of the Trade Act. China, European Union, India, UK, South Korea are among economies subject to these investigations. Investigations will determine whether acts, policies, and practices of each of these economies related to the failure to impose and effectively enforce a ban on the importation of goods produced with forced labor are unreasonable or discriminatory and burden or restrict US commerce.

UK/EU (FT): Reeves to Make New Push for Greater Single-Market Access

Chancellor Rachel Reeves will next week make another push for Britain to secure greater access to the single market against a backdrop of renewed trade strains between London and Brussels. Reeves will use her Mais economic lecture to pitch her vision for closer ties with the EU, which is central to a new growth strategy for the UK. “It will be a statement of intent,” said one person close to the chancellor. But her agenda is meeting resistance in some European capitals. Talks in Brussels about a limited “reset” of relations — covering a youth mobility scheme and a removal of barriers to trade in agricultural products and energy — have dragged on for months.

UK (The Guardian): Starmer May Face More Resignations After Release of Mandelson Whatsapp Messages, Say Sources

Keir Starmer could suffer further resignations when ministerial WhatsApp messages are published in the next tranche of the Peter Mandelson files, senior government sources have told the Guardian. With officials bracing for the subsequent releases – expected to include informal communications alongside formal messages like those in the first batch – Starmer apologised again on Thursday over his handling of Mandelson’s appointment, saying: “It was me that made a mistake, and it’s me that makes the apology to the victims of [Jeffrey] Epstein, and I do that.” Officials believe some of the exchanges to be released in the next tranche of Mandelson files will be damaging enough to lead to further departures.

BOJ (MNI EXCLUSIVE): BOJ's Renewed Price Focus Improves Hike Conditions

MNI discusses the BoJ's renewed focus on price pressures. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (BBG): Japan’s Katayama Says in Closer US Contact on FX Than Usual

Japanese financial authorities are staying in closer contact with their US counterparts than usual over currencies, as the yen trades near the weakest levels this year against a backdrop of widespread market volatility in response to the conflict in Iran. Finance Minister Satsuki Katayama told reporters on Friday she would refrain from commenting on the topic of currency intervention. “In any case, we are in much closer contact with US authorities than usual,” she said.

JAPAN (BBG): Japan to Sell Oil From National Reserves at Pre-Iran War Prices

Japan will sell oil from its national reserves at prices based on levels before the start of the Middle East war, according to the country’s trade minister. The country announced this week it would release about 80 million barrels of oil from its state and private reserves, and it could start as soon as next week. The crude would be sold at levels based on the pre-conflict official selling prices of Middle Eastern producers, Minister of Economy, Trade and Industry Ryosei Akazawa said on Friday.

PERU (BBG): Peru Holds Key Rate at 4.25% as Inflation Pressures Mount

Peru left interest rates unchanged after inflation accelerated above the midpoint of its target range for the first time in more than a year. The central bank held its benchmark rate at 4.25% on Thursday, as expected by all nine analysts surveyed by Bloomberg. Inflationary pressure is mounting due to bad weather, rising global fuel prices and a domestic natural gas crisis that led to two-week rationing of the cheap fuel, the bank said.

DATA

UK DATA (MNI): Employment Activities Biggest Negative Contributor to Monthly GDP

- UK JAN GDP 0.0% M/M, 0.2% 3M/3M, 0.9% 3M Y/Y

- UK JAN IND PROD -0.1% M/M, 0.4% Y/Y

- UK JAN MANUF OUTPUT 0.1% M/M, 1.3% Y/Y

- UK JAN SERVICES OUTPUT 0.0% M/M, 0.2% 3M/3M

- UK JAN TOTAL TRADE BALANCE GBP +3.92BLN

This from the ONS doesn't really bode well for the labour market (albeit remember this is January data so is quite lagged) - and bear in mind we have been at similar levels previously so we aren't breaking to new low in the index values yet: "The fall in employment activities was the largest negative contribution from a single industry to both services output and real GDP growth, contributing negative 0.08 percentage points to services output, and negative 0.06 percentage points to real GDP growth in January 2026. This fall in employment activities follows four consecutive months of growth." Note that employment activities includes things like headhunters, employment agencies HR provision etc.

GERMANY FEB WHOLESALE PRICES 1.2% Y/Y (MNI)

GERMANY FEB WHOLESALE PRICES 0.6% M/M (MNI)

FRANCE FEB HICP 1.1% Y/Y (1.1% FLASH, 0.4% JAN) (MNI)

FRANCE FEB HICP 0.7% M/M (0.8% FLASH, -0.4% JAN) (MNI)

FRANCE FEB CPI 0.9% Y/Y (1.0% FLASH, 0.3% JAN) (MNI)

FRANCE FEB CPI 0.6% M/M (0.7% FLASH, -0.3% JAN) (MNI)

SPAIN FEB FINAL HICP 2.5% Y/Y (2.5% FLASH, 2.4% JAN) (MNI)

SPAIN FEB FINAL HICP 0.4% M/M (0.4% FLASH, -0.8% JAN)

SWEDEN DATA (MNI): LFS Unemployment Rate Rebounds But Downward 3mma Trend Intact

- SWEDEN FEB UNEMPLOYMENT SA 8.4% (8.0% JAN)

- SWEDEN FEB UNEMPLOYMENT NSA 8.8% (8.6% JAN)

The Swedish LFS unemployment rate bounced back to 8.4% in February after 8.0% in January and 8.8% in December. This was in line with the median analyst estimate. That also leaves the 3mma unemployment rate at 8.4%, tracking below the Riksbank's 8.9% forecast for Q1 from the December MPR. Public Employment Service (PES) data has been signalling for a decline in the LFS unemployment rate for some time. At next week's Riksbank decision, the Board will likely express cautious optimism around the labour market through 2026, albeit with the Iran war adding heightened uncertainty to the outlook.

CHINA JAN-FEB NEW LOANS CNY5.61 TRLN VS MEDIAN CNY5.61 TRLN (MNI)

CHINA JAN-FEB TSF CNY9.6 TRLN VS MEDIAN CNY9.22 TRLN (MNI)

CHINA END-FEB M2 +9.0% Y/Y VS MEDIAN +9.0%; END-JAN +9.0% Y/Y (MNI)

EGBS: Bund Futures Off Session Lows But a Bear Cycle Still in Play

Bund futures have moved away from session lows, maintaining a close correlation with Brent crude price action. However, a bear cycle remains intact, reinforced by this morning’s piercing of key support at 125.90, the Dec 22 low. Bunds are currently -11 ticks at 126.07, but a resumption of weakness below today’s 125.73 low would expose Fibonacci projection levels at 125.49 and 125.25.

- Sensitivity to Iran war headline flow remains acute. Although US President Trump told G7 leaders that Iran is “about to surrender”, rhetoric from both the US and Iranian side yesterday suggests an end to the conflict is not imminent.

- 10-year Bund yields opened at 2.992% this morning, but have since eased back a little to 2.955%

- The German curve has lightly twist steepened, with 5s30s up 2.6bps to 92.9bps.

- 10-year EGB spreads to Bunds are wider once again, with European equity risk sentiment on the back foot. The 10-year BTP/Bund spread is at 82bps, with focus on whether it retests the 85bp level.

- Italian January industrial production was weaker than expected this morning (-0.6% M/M vs +0.4% cons). There is plenty of US data due this afternoon, but all the focus is on Middle East developments ahead of the weekend.

GILTS: Off Early Lows, Crude Remains Key

Gilts trade off early lows with crude back from highs following reports that Iran allowed a Turkish vessel to cross the Strait of Hormuz.

- Futures based at 88.49 before recovering to 88.80 last.

- Bears remain in technical control. Next support comes in the form of a projection drawn off the February 27-March 3-March 4 price swing (88.47). while initial resistance is located at the March 12 high (89.70).

- Yields 0.5-1.5bp higher.

- Monday highs remain intact in 2s and 5s.

- 10s briefly traded above 4.80% for the first time since September, placing focus on the September ’25 top (4.845%) after piercing the upper bound of the ascending triangle we have been monitoring in recent months.

- Further out the curve October highs are unchallenged in 20s and 30s, but 50s threatened a clean break above their ’25 top before backing off.

- 70bp has capped steepening moves in 2s10s over the past couple of sessions.

- ~19.5bp of BoE tightening priced through year-end vs ~22bp late yesterday.

- March ’25 lows in SFIZ6 (96.005) remain intact.

- The latest BoE/Ipsos inflation expectations survey showed that 1-year expectations fell to 3.2% from 3.5%, but it is somewhat outdated. The sample was surveyed between 6 and 11 February & 20 and 24 February 2026, before the escalation in the Middle East.

- Geopolitical issues should continue to dominate into the weekend, with U.S. PCE data also due.

Figure 2: UK 10-Year Gilt Yield (%)

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

| Mar-26 | 3.726 | -0.4 |

| Apr-26 | 3.703 | -2.6 |

| Jun-26 | 3.769 | +3.9 |

| Jul-26 | 3.821 | +9.2 |

| Sep-26 | 3.873 | +14.4 |

| Nov-26 | 3.910 | +18.0 |

| Dec-26 | 3.924 | +19.4 |

EQUITIES: E-Mini S&P Narrows Gap to Key Medium-Term Support at 6583.00

The sharp rebound in EuroStoxx 50 futures from Monday’s low is for now, considered corrective and this is allowing an extreme oversold trend condition to unwind. Key short-term resistance to watch is 5919.41, the 50-day EMA. A clear break of this average is required to signal a possible reversal. A resumption of the bear leg would open 5500.00, the Nov 21 ‘25 low. A clear breach of it would strengthen the bear cycle. A sharp bounce in S&P E-Minis on Monday and the reversal from Tuesday’s high highlights the fact that recent gains were most likely corrective. This has allowed a recent oversold trend condition to unwind. A continuation lower would open 6583.00, the Nov 21 ‘25 low and the next key medium-term support. Clearance of this level would strengthen a bearish threat. Initial firm resistance is 6878.09, the 50-day EMA.

- Japan's NIKKEI closed lower by 633.35 pts or -1.16% at 53819.61 and the TOPIX ended 20.82 pts lower or -0.57% at 3629.03.

- Elsewhere, in China the SHANGHAI closed lower by 33.655 pts or -0.82% at 4095.448 and the HANG SENG ended 251.16 pts lower or -0.98% at 25465.6.

- Across Europe, Germany's DAX trades lower by 162.51 pts or -0.69% at 23422.6, FTSE 100 lower by 50.07 pts or -0.49% at 10254.63, CAC 40 down 63.68 pts or -0.8% at 7919.56 and Euro Stoxx 50 down 35.16 pts or -0.61% at 5713.68.

- Dow Jones mini down 14 pts or -0.03% at 46709, S&P 500 mini down 1.75 pts or -0.03% at 6675.75, NASDAQ mini down 17 pts or -0.07% at 24545.

Time: 09:15 GMT (05:15 ET)

COMMODITIES: WTI Futures Hoilding Onto Bulk of Thursday's Rally

A volatile impulsive bull wave in WTI futures remains intact. The recent sharp pullback has allowed an extreme overbought trend condition to unwind. A key support zone to monitor is $76.92 - $68.95, the area between the 20- and 50-day EMAs. A clear break through this zone would signal a possible trend reversal. On the upside, a continuation higher near-term would open $103.15 next, a Fibonacci retracement. Gold remains in consolidation mode and is trading below $5419.11, the Mar 2 high. A short-term bullish theme is intact following recent gains. The metal has cleared all key retracement points of the sharp sell-off between Jan 29 - Feb 2. This strengthens the short-term bullish theme and signals scope for an extension towards key resistance and the bull trigger at $5595.5, the Jan 29 high. Initial firm support to watch lies at $4921.6, the 50-day EMA.

- WTI Crude down $0.18 or -0.19% at $95.53

- Natural Gas up $0.05 or +1.55% at $3.284

- Gold spot up $10.91 or +0.21% at $5090.83

- Copper down $6.55 or -1.12% at $580.3

- Silver down $1.24 or -1.48% at $82.6485

- Platinum down $50.31 or -2.36% at $2082.63

Time: 09:15 GMT (05:15 ET)

| Date | GMT/Local | Impact | Country | Event |

| 13/03/2026 | 1000/1100 | ** | EZ Industrial Production | |

| 13/03/2026 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 13/03/2026 | 1230/0830 | *** | Labour Force Survey | |

| 13/03/2026 | 1230/0830 | * | Intl Investment Position | |

| 13/03/2026 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 13/03/2026 | 1230/0830 | *** | Personal Income and Consumption | |

| 13/03/2026 | 1230/0830 | ** | Durable Goods New Orders | |

| 13/03/2026 | 1400/1000 | *** | JOLTS | |

| 13/03/2026 | 1400/1000 | *** | UMich Surveys of Consumers | |

| 13/03/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |