MNI CHINA MONEY MARKET INDEX:Liquidity Ample, Yield Curve Flat

Ample interbank liquidity will keep Chinese money market rates low over the next month, reducing the need for central bank interest rate cuts, and further push down long-end government bond yields, MNI’s China Money Market Index indicated, with traders seeing limited impact on the economy from the Middle East energy shock.

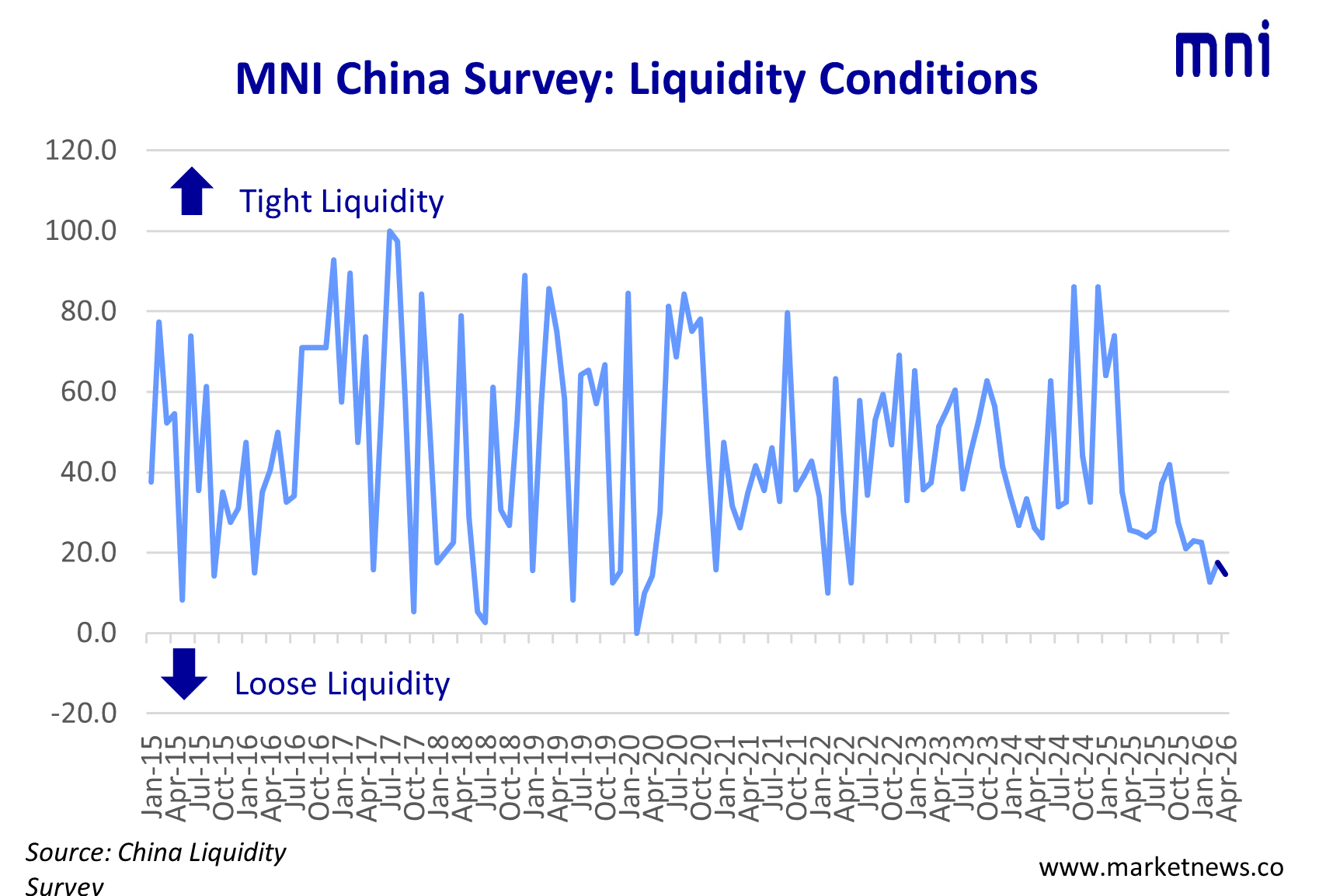

All participants expected the seven-day repo rate for deposit-taking institutions (DR007) to remain at the current low level or even fall further next month, with the sub-index rising to 57.8 from 52.9 in March. DR007 is benchmarked by the PBOC’s key seven-day reverse repo rate.

The PBOC’s seven-day reverse repo rate outlook sub-index edged down to 54.9 from last month’s 56.9, with 90.2% of participants expecting a steady policy rate in the coming month, and 9.8% saying the PBOC could cut the rate, compared with 13.7% last month.

Money market rates are declining, with overnight rates at 1.2%–1.25%, and seven-day repo rates at 1.35%–1.4%, both below the policy rate of 1.4%, indicating very loose liquidity, said a trader from Jiangsu. Major banks' average net liquidity supply has been about CNY5.6 trillion per day, pushing prices lower, said a Shanghai trader. A Hebei trader noted that abundant funds have fuelled a bull market for bonds, while credit demand stays weak, leaving liquidity idle within the financial system. (See MNI: PBOC To Reduce OMOs Further, Drain Bond Liquidity)

The China liquidity outlook sub-index fell to 43.1 from March’s 49.0 (the lower it reads, the looser liquidity), the lowest since January, with no participant expecting tight conditions in the coming month, compared with 3.9% last month. The sub-index covering current liquidity conditions fell to 14.7 from 17.6, with 70.6% of participants seeing looser liquidity than last month, compared with 64.7% in March.

The Jiangsu trader said the central bank has kept its open market operations at a minimal scale in recent weeks, trying to guide rates back toward the policy rate.

The overall sub-index for the PBOC’s OMO outlook remained unchanged at 49.0, with 23.5% of traders seeing “net injections” next month, compared to 29.4% in March. The sub-index covering the PBOC’s current OMOs edged down to 50.0 from 52.0 as all participants assessed OMOs as being “in line with demand”.

The outright-reverse-repo-coming-month-outlook sub-index rose to 39.2 from 36.3, as fewer traders expected the PBOC to increase operations.

The next-six-month-policy-outlook sub-index showed expectations for further easing continuing to fall, with 45.1% of traders expecting additional policy moves, compared with 51.0% in March, taking the index to 27.5 from 24.5. The sub-index for current policy bias printed at 36.3 from 34.3, with 27.5% seeing an easier stance compared with 31.4% last month.

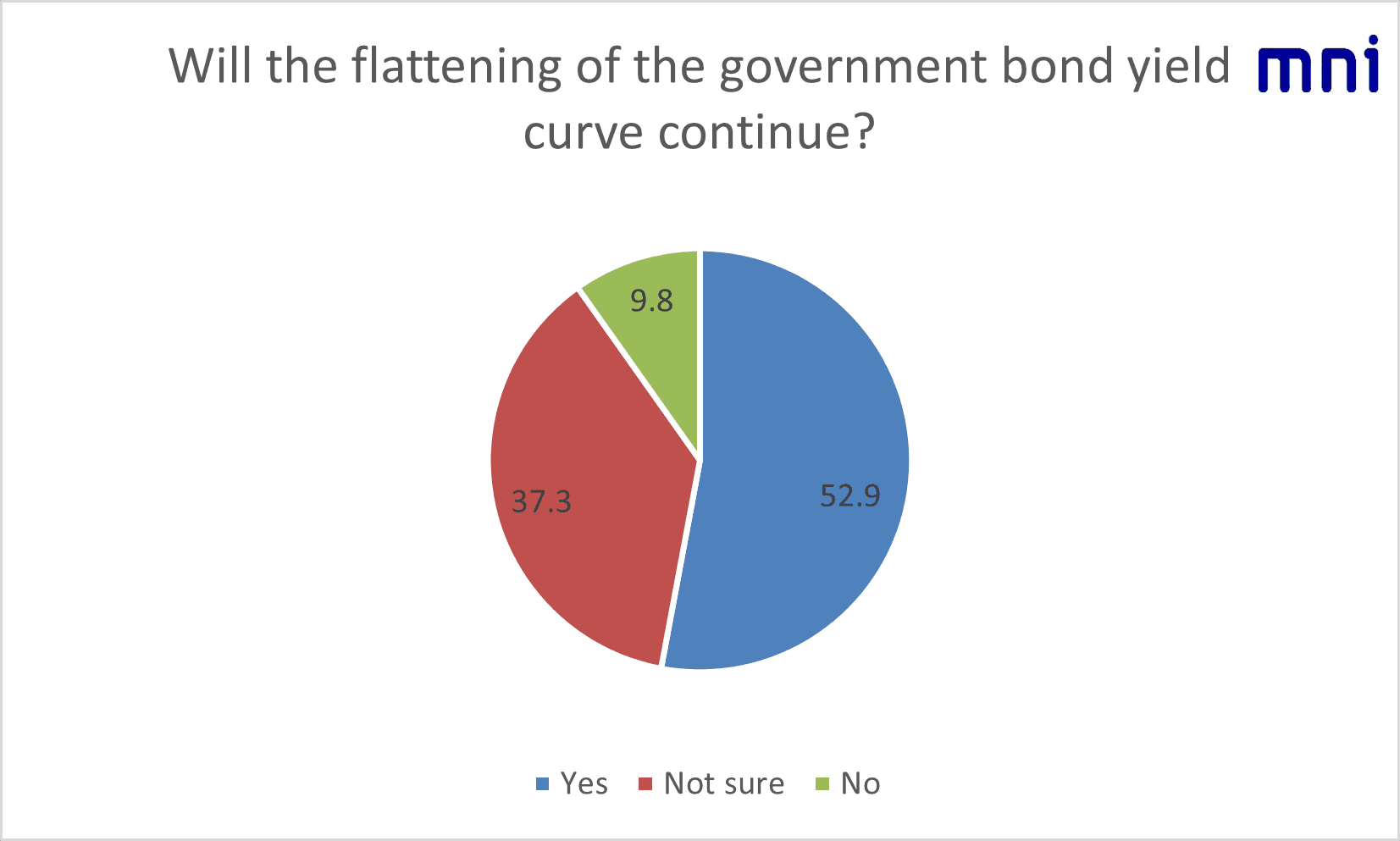

MNI’s special question showed 52.9% of traders expected a flatter CGB yield curve.

Short-end yields are already low, compressing arbitrage spreads, so funds have flowed to the medium and long end, said a Shanghai trader. A Fujian trader noted the 30-year and 10-year CGB yield spread was 49bp and narrowing rapidly. Without clear signs of economic recovery or a tightening of liquidity in the second half, a flat curve remains the likely scenario, he added.

The other special question indicated 56.9% of participants assessed the impact of the energy shock on the economy as controllable, though 10% were concerned about the sustainability of robust growth in Q1. (See MNI INTERVIEW: China 2026 Export Growth To Support Yuan)

Geopolitical uncertainty, persistent imported inflation, and risks of supply-chain disruptions could all pose challenges to the economic recovery, while exports may slow after recent front-loading fades and global demand may also reduce, said a trader from Beijing. A Shandong trader was worried that rising oil prices could push up costs as domestic demand remains weak, squeezing profit margins for companies unable to increase prices due to intense competition.

The MNI China Money Market Index (MMI) survey was conducted from April 12 to April 24, with participation of 51 traders from both state-owned and joint-venture banks.

For the full China MMI press release:

Hidden PDF