MNI US OPEN - Ueda Signals More Hikes But Timing Unclear

EXECUTIVE SUMMARY

- UEDA SIGNALS MORE HIKES, TIMING UNCLEAR

- CARNEY SAYS CANADA-US TRADE TALKS RESUMING IN MID-JANUARY

- JOINT DEBT TO FUND UKRAINE FOR 2026 AS BELGIAN PM HOLDS FIRM

- GUIDANCE SHIFT SUGGESTS BANXICO PAUSE

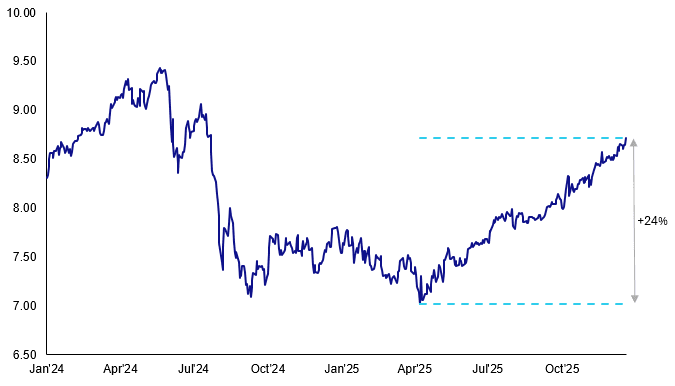

Figure 1: MXN/JPY extends recovery off YTD lows to over 20% following Banxico, BOJ decisions

Source: MNI, Bloomberg Finance L.P.

NEWS

BOJ (MNI): Ueda Signals More Hikes, Timing Unclear

Bank of Japan Governor Kazuo Ueda laid the groundwork for further interest rate increases after the BOJ’s board decided on a unanimous 25-basis-point hike to the highest level in three decades on Friday, but provided little clue as to timing and stressed that policymakers must examine the impact of higher rates on the economy, inflation and financial conditions. The next increase in the policy rate, now at 0.75%, could be in sight if, as seems likely, wage increases next year continue to buoy inflation towards the 2% target on a stable and sustainable basis, Ueda told a press conference, but without saying when that might be apparent.

US/CANADA (MNI): Canada-US Trade Talks Resuming in Mid-January - Carney

Canadian Prime Minister Mark Carney said Thursday trade talks with the U.S. will resume in mid-January, after President Donald Trump halted them a few weeks ago. Carney again called talks next year revisiting a North American free trade pact a "review" while Trump and his officials have said they will seek more concessions from Canada in areas such as dairy products.

US (WSJ): OpenAI’s New Fundraising Round Could Value Startup at as Much as $830 Billion

OpenAI is aiming to raise as much as $100 billion as it seeks to pay for ambitious growth plans in a market that has cooled recently on the artificial-intelligence boom. The fundraising round, which is in the early stages, could value the company at as much as $830 billion, if it raises the full amount it is targeting, people familiar with the matter said. The startup aims to complete the round by the end of the first quarter at the earliest. Terms of the deal could still change, and it is unclear whether there will be sufficient investor demand to reach the goal.

MEXICO (MNI): Guidance Shift Suggests Banxico Pause

The Central Bank of Mexico changed its forward guidance in a way that could suggest a pause at the next meeting, or at least a shift toward a more data-dependent stance, after Thursday’s decision to cut interest rates by 25 basis points to 7.00%. The board did not signal a cut at the next meeting, as it had done previously, and instead said it will "evaluate the timing for additional reference rate adjustments." In the previous decision in November, Banxico had said it would "evaluate reducing the reference rate." As justification for a more cautious stance, the board cited the resilience of services inflation. Deputy Governor Jonathan Heath again dissented in favor of holding steady.

EUROPEAN COUNCIL (MNI): Joint Debt to Fund Ukraine for 2026 as Belgian PM Holds Firm

A marathon European Council summit that ran into the early hours of 19 December resulted in a deal to provide Ukraine with a EUR90bln loan that will not have to be repaid until Russia pays reparations to Kyiv once the war eventually ends. Rather than the preferred plan of Commission President Ursula von der Leyen and German Chancellor Friedrich Merz, which envisaged using frozen Russian assets held in the EU as collateral, the loan will be financed by joint debt issuance guaranteed by the EU budget. For months, Belgian PM Bart De Wever had held firm against calls to use the hundreds of billions of euros in frozen Russian assets held at Euroclear. With EU leaders unwilling to provide unlimited financial guarantees, De Wever maintained his stance and refused to back the frozen assets plan.

ECB (BBG): ECB Will Be as Agile as Needed at Coming Meetings, Villeroy Says

The European Central Bank will continue to be agile in setting interest rates at coming meetings, after keeping borrowing costs on hold on Thursday, Governing Council Member Francois Villeroy de Galhau said. While the ECB be can be satisfied with “mission accomplished” as inflation has been at target for seven months, it should keep full “optionality” given the uncertainty, the Bank of France Governor told Le Figaro in an interview.

ECB (BBG): ECB’s Schnabel ‘Rather Comfortable’ on Bets Next Move to Be Hike

Executive Board member Isabel Schnabel is comfortable with investor bets that the European Central Bank’s next interest-rate move will be an increase. While borrowing costs are at levels that — barring further shocks — will be appropriate for some time, consumer spending, business investments and a jump in government outlays on defense and infrastructure will bolster the economy, Schnabel said. “Both markets and survey participants expect that the next rate move is going to be a hike, albeit not anytime soon,” she said last week in an interview in her office in Frankfurt. “I’m rather comfortable with those expectations.”

ECB (BBG): ECB’s Muller Says Too Early to Say Where Rates May Go Next

European Central Bank Governing Council member Madis Muller said it’s too soon to say where borrowing costs may go next. Speaking a day after the ECB kept its deposit at 2% for a fourth straight meeting, the Estonian official said there’s no current need to make adjustments but wouldn’t be drawn beyond that. “If you ask what will happen in six months or after that, it’s honestly too early to speculate,” Muller told Estonian radio.

FRANCE (MNI): PM Lecornu Confirms Failure of State Budget Joint Committee Talks

Latest on French politics from PM Lecornu on X: "The Government acknowledges the failure of the joint committee in which members of parliament and senators sat, without the government [...] I regret, however, the lack of willingness to reach an agreement on the part of some members of parliament, as we unfortunately feared had been the case for the past few days. In accordance with the deadlines set by the Constitution and organic laws, Parliament will therefore not be able to pass a budget for France before the end of the year [...] In this context, I will convene, starting on Monday, the main political leaders to consult them on the steps to take to protect the French and find the conditions for a solution."

CHINA (FT): China Boosts AI Chip Output by Upgrading Older ASML Machines

China’s semiconductor manufacturers are upgrading their advanced chipmaking equipment in ways that bypass global export controls, as the country seeks to rival the US in developing artificial intelligence. According to people familiar with the matter, Chinese fabrication plants producing advanced smartphone and AI chips have bolstered the performance of advanced deep ultraviolet lithography (DUV) machines made by Netherlands-based ASML. US and Dutch export controls prevent ASML from supplying its most advanced DUV machines to China, leaving many Chinese fabs to rely on older equipment — notably the Twinscan NXT:1980i system — to manufacture the seven-nanometre chips needed to develop AI systems.

RUSSIA (NYT): Putin to Project Unyielding Stance on Ukraine at News Marathon

President Vladimir V. Putin of Russia on Friday started his annual news conference, an event that is expected to highlight the Kremlin’s determination to continue the war in Ukraine until all of its conditions are met. The year-end hourslong marathon, where both journalists and other citizens pose their questions to the Russian leader, is an elaborately orchestrated television show and a demonstration of how, over the past three decades, Mr. Putin has solidified his position as the ultimate — and perhaps only — decision maker in the country. He is portrayed as personally engaged in everyday issues like leaking pipes in small cities, even as he oversees major matters of foreign conflict.

DATA

UK DATA (MNI): UK November Borrowing Lowest in Four Years - ONS

- UK NOV PSNB GBP+11.65 BN

- UK NOV PSNB-EX GBP+11.65 BN

- UK NOV PSNCR GBP10.29 BN

- UK NOV CGNCR-EX GBP13.59 BN

UK government borrowing was GBP11.7 billion in November, nearly GBP2 billion lower than the same month last year and the lowest for any November since 2021, the Office for National Statistics said on Friday. For the financial year to date, borrowing was GBP132.3 billion; GBP10.0 billion more than in the same eight-month period of 2024 and the second-highest April-to-November nominal borrowing on record after 2020. Public sector net debt excluding public sector banks stood at 95.6% of GDP, a level last seen in the early 1960s. Public sector net financial liabilities excluding public sector banks were estimated at 85.1% of GDP, 2.7 percentage points more than a year ago.

UK DATA (MNI): Retail Sales Were Soft; But Signal Distorted by Budget and Black Friday

- UK NOV RETAIL SALES INC FUEL -0.1% M/M, +0.6% Y/Y

- UK NOV RETAIL SALES EX-FUEL -0.2% M/M, +1.2% Y/Y

Retail sales was on the soft side but not disastrous here with some upward revisions. We always prefer to look at Nov/Dec together due to the timing of purchases over the holiday period (which may have been particularly impacted this year by Budget uncertainty). Also there are concerns over the ONS' Black Friday seasonal adjustments - so this data is probably less reliable than usual. The ONS notes that non-store retailing fell 2.9%M/M as demand for gold slowed, while supermarket sales fell for the fourth consecutive month. We don't expect any real policy signal from this print.

UK DATA (MNI): GfK Consumer Confidence Reverses November's Fall

- UK DEC GFK CONSUMER CONFIDENCE INDEX -17

December's GfK Consumer Confidence Barometer increased two points to -17 (vs -18 Bloomberg consensus, -19 November). The index is now back at the level seen in October, and is exactly in line with December 2024. The index has sat between -20 and -17 since June. GfK notes the Budget being "not as bad as most had feared" as a potential upward driver, though they also highlight that households still face cost-of-living pressures and rising economic uncertainty despite softening inflation.

ECB DATA (MNI): Wage Tracker Still Points to Declining Pay Pressures Through '26

The ECB's forward looking wage tracker continues to suggest that negotiated wage pressures will ease through 2026, albeit at a slower pace than expected in October. The tracker now includes Q4 2026, albeit with a low employee coverage ratio of just 23%. Negotiated wages excluding one-off payments are expected at 2.8% in Q1 '26, 2.6% in Q2 and 2.5% in Q3, before rising to 2.7% in Q4.

GERMANY DATA (MNI): GfK Consumer Climate Falls, Wider Picture Remains Subdued

- GERMANY JAN GFK CONSUMER CLIMATE -26.9 (-23.0 FCST, -23.4 DEC)

The German GfK consumer climate decreased by 3.5 points to -26.9 in its January advance reading, below consensus expectations which looked for a marginal uptick to -23.0. GfK notes "while economic expectations are stagnating, both income expectations and willingness to buy are declining". The consumer climate had lagged improvements in German business sentiment, but that also turned to the downside again in most recent readings. The bigger picture may be that both consumers and businesses are sceptical if the fiscal easing programme from the government will bring a lasting upturn to the country.

GERMANY NOV PPI +0.0% M/M, -2.3% Y/Y (MNI)

FRANCE DATA (MNI): Stronger Retail Sales Helped by Spike in New Car Sales

French retail sales volumes saw their largest monthly increase in over four years in November to leave their level at its highest since Sep 2023 after a few dour years. PPI inflation meanwhile saw an energy-driven acceleration on the month although base effects drove a deflationary -3.3% Y/Y. French retail sales volumes grew 1.5% M/M in November (fastest since Jun 2021) after a modest 0.2% M/M in October, with most sectors seeing either rebounds of October weakness or sharp spikes, particularly new cars and household appliances.

FRANCE NOV PPI +1.1% M/M, -3.3% Y/Y (VS +0.0% M/M, -0.8% Y/Y OCT) (MNI)

SWEDEN DATA (MNI): Dec ETI and Nov Retail Sales Strengthen Recovery Signals

- SWEDEN NOV RETAIL SALES +5.6% Y/Y

This morning's Swedish data provided further evidence of a cyclical recovery, alongside positive labour market signals. The Riksbank acknowledged stronger activity trends at yesterday's monetary policy decision, but still believed "a policy rate at its current level helps to strengthen domestic demand and thus also economic activity". That said, if domestic data continue to strengthen, and inflation doesn't fall as much as expected, we would expect a more explicitly hawkish pivot at one of the quarterly decisions in H1 '26.

NORWAY DATA (MNI): Fall in Registered Unemployment Rate Supports Yesterday's Stance

The first piece of data following yesterday's Norges Bank decision supported the less dovish-than-expected rate path revisions. The registered unemployment rate for December fell back to 2.1%, below the 2.2% expected by consensus and Norges Bank. The number of unemployed persons, in seasonally adjusted terms, fell 1k to 63.835k - the lowest level since July. Meanwhile, vacancies per day fell a little to 1.887k (vs 1.967k in November), but remains above the 1.852k seen in October.

JAPAN DATA (MNI): Japan Nov Core CPI Rises 3.0% vs. Oct 3.0%

- JAPAN NOV CORE CPI +3.0% Y/Y; OCT +3.0%

- JAPAN NOV CORE-CORE CPI +3.0% Y/Y; OCT +3.1%

- JAPAN NOV SERVICES PRICES +1.6% Y/Y; OCT +1.6%

Japan’s annual core consumer inflation rate rose 3.0% y/y in November, unchanged from October, reflecting a combination of lower energy prices and higher food prices excluding perishables, data released by the Ministry of Internal Affairs and Communications showed on Friday. The November reading remained above the Bank of Japan’s 2% target for a 44th consecutive month and held at the 3% level for the second straight month. Energy prices increased 2.5% y/y in November, accelerating from October’s 2.1% rise, boosting the overall index. By contrast, food prices excluding perishables rose 7.0%, easing slightly from 7.2% in October and weighing on inflation.

FOREX: USDJPY Surges Through 157.00 on BoJ

- USDJPY is rallying well early Friday, rising over 1% to clear the 156.95 December 9 high as the lack of meaningful, hawkish guidance from BoJ Governor Ueda following the expected target rate hike weighs on JPY. The BoJ did signal it will continue raising rates in line with improvements in growth, wages and inflation, while maintaining accommodative conditions to support the economy - but this fell well short of any firmer commitment on tightening.

- Price action does strengthen bullish conditions in the pair, opening back up the 157.89 November 20 high and bull trigger. Above 158.00, the January 10 high and key resistance stands at 158.87. Speculative positioning may well prevail in terms of short-term drivers for spot as volumes remain high in recent trade.

- GBP meanwhile outperforms as markets digest yesterday's BoE meeting as well as follow-up comments from Governor Bailey this morning, in which he repeated that the Bank is getting nearer to the neutral rate. Despite this, GBPUSD is seeing only limited volatility as the JPY weakness spills over into USD markets. GBPUSD trades within range of resistance at the Dec 16 high of 1.3456 and support the Dec 17 low at 1.3312.

- NZDUSD pierces below its 20- and 50-day EMAs at 0.5748 as RBNZ hiking expectations have been pared to some extent this week. Some room for further adjustment remains, however.

- NY Fed's Williams is scheduled to appear on CNBC later. There are a host of Governing Council speakers scheduled today, where we don't expect meaningful departures from the ECB's central guidance, but will continue to monitor for nuances in view. Michigan inflation expectations and sentiment are on the data calendar.

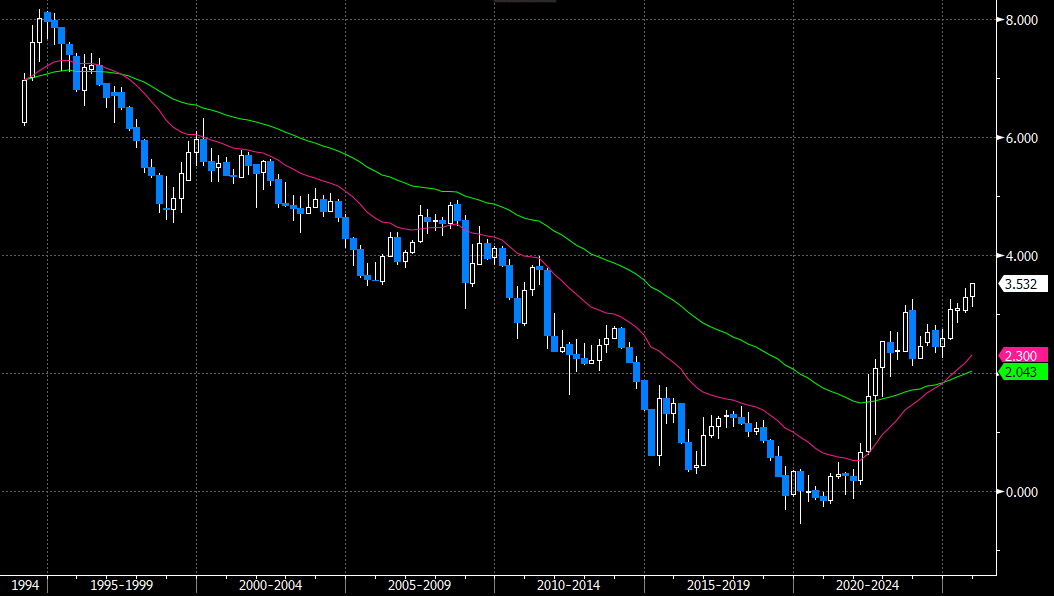

EGBS: German Curve Resumes Steepening Bias

With the ECB and Germany’s 2026 issuance plan now in the rear view, the German curve has resumed its steepening bias. 2-year yields are up 1bp today, while 30-year yields are now up almost 5bps. 30-year Bunds over just below resistance at 3.55%, clearance of which would expose 3.60%. Meanwhile, 10-year yields are up 3,5bps and threatening another test of the 2.90% figure.

- Bund futures are -35 ticks at 127.22. Futures are currently in consolidation mode, with a broader bear cycle still intact. Initial support is the Dec 10 low of 127.05.

- Today’s regional data hasn’t been market moving. The ECB’s forward looking wage tracker continues to point to downside pay pressures next year. Meanwhile, national central banks have been releasing their updated macroeconomic projections following the ECB’s December decision.

- Several ECB policymakers have spoken today, most sticking to President Lagarde’s press conference script. Villeroy flagged downside inflation risks.

- In France, the Joint Committee has been unable to reach an agreement on the 2026 state budget (PLF), meaning the Government cannot pass its full budget before year-end. As such, the Government is expected to introduce a special bill to ensure the continuity of operations while budget negotiations restart/resume in the new year). The 10-year OAT/Bund spread widened modestly (~0.9bps) since the news broke, now 0.5bps wider on the session at ~71bps. The 70bp figure continues to contain downside in the spread for now, and failure to pass a budget may keep this support intact into the start of next year.

- Eurozone December consumer confidence is due this afternoon, with ECB Chief Economist Lane also scheduled to speak.

Figure 2: 30-year Bund Yield - Quarterly (Source: Bloomberg Finance L.P)

GILTS: Support Tested in Futures, Curve Steepens

Spillover from weakness in wider core global FI trade, aided by the delivery of the latest BoJ rate hike and ongoing weakness in the German long end, weighs on long dated gilts.

- Elsewhere, retail sales data was soft (albeit subject to pre-Budget uncertainty and Black Friday distortions), while UK public finance data came in on the soft side (gilt-negative).

- Futures test yesterday’s low (90.99), with 90.50 providing a more meaningful downside level.

- Yields 1bp lower to 3bp higher, curve twist steepens.

- Benchmark yields stick comfortably within month-to-date ranges.

- 2s10s is set for the highest close of December at current levels (77.4bp). The next upside target is located at the pre-Budget closing high (79.5bp).

- Gilt/Bunds little changed at 162.5bp after yesterday’s failed break of 160bp. There hasn’t been a sub-160bp close in the spread since July ’24.

- BoE-dated OIS prices ~38bp of easing for ’26, next 25bp move not fully discounted until the June MPC after the hawkish reaction to yesterday’s BoE decision.

- SONIA futures flat to -2.5.

- We have flagged the potential for further downside in the SONIA/Euribor Dec ’26 spread in the new year, based on relative central bank outlooks.

- Comments from BoE Governor Bailey failed to impact markets, generally reaffirming knowns/widely discussed themes.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Rate Cut-Adjusted SONIA (bp) |

Feb-26 | 3.709 | -1.6 |

Mar-26 | 3.620 | -10.5 |

Apr-26 | 3.506 | -21.9 |

Jun-26 | 3.447 | -27.8 |

Jul-26 | 3.381 | -34.4 |

Sep-26 | 3.358 | -36.7 |

Nov-26 | 3.339 | -38.6 |

Dec-26 | 3.344 | -38.1 |

EQUITIES: Eurostoxx 50 Futures Extend Recovery Off This Week's Low

A bull cycle in Eurostoxx 50 futures remains intact and the latest pullback appears corrective. The first key support to watch lies at 5654.19, the 50-day EMA. A clear break of the average would highlight a potential short-term reversal. This would open 5594.00, the Nov 26 low. For bulls, a resumption of gains would refocus attention on key resistance at 5825.00, the Nov 13 high. Yesterday’s price pattern is a bullish engulfing candle - a reversal signal. A pullback in S&P E-Minis has resulted in a breach of both the 20- and 50-day EMAs. This strengthens a short-term bear threat and signals scope for a deeper retracement of the recent bull phase between Nov 21 - Dec 11. Sights are on 6737.71, a Fibonacci retracement. Note that the key support and reversal trigger lies at 6583.00, the Nov 21 low. For bulls a resumption of gains would refocus attention on key resistance at 7014.00, the Oct 30 high.

- Japan's NIKKEI closed higher by 505.71 pts or +1.03% at 49507.21 and the TOPIX ended 26.77 pts higher or +0.8% at 3383.66.

- Elsewhere, in China the SHANGHAI closed higher by 14.077 pts or +0.36% at 3890.448 and the HANG SENG ended 192.4 pts higher or +0.75% at 25690.53.

- Across Europe, Germany's DAX trades higher by 46.94 pts or +0.19% at 24246.67, FTSE 100 higher by 0.68 pts or +0.01% at 9838.13, CAC 40 up 4.18 pts or +0.05% at 8155.45 and Euro Stoxx 50 up 4.68 pts or +0.08% at 5746.54.

- Dow Jones mini up 52 pts or +0.11% at 48040, S&P 500 mini up 22.75 pts or +0.34% at 6801, NASDAQ mini up 118.75 pts or +0.47% at 25147.

Time: 10:00 GMT

COMMODITIES: Gold Trend Structure Remains Unchanged and Bullish

The trend condition in WTI futures remains bearish. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A key support and the bear trigger at $56.11, the Oct 17 low, has been breached. Clearance of this level resumes the downtrend and opens $53.77, a Fibonacci projection. Key short-term resistance to watch is $61.25, the Oct 24 high. First resistance is at $58.83, the 50- day EMA. The trend structure in Gold is unchanged, it remains bullish. The bear phase between Oct 20 - 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4106.7. Clearance of this EMA would signal scope for a deeper retracement. Price is approaching key resistance and the bull trigger at $4381.5, the Oct 20 high. A break resumes the primary uptrend.

- WTI Crude down $0.26 or -0.46% at $55.89

- Natural Gas down $0.01 or -0.15% at $3.9

- Gold spot down $3 or -0.07% at $4329.31

- Copper up $6.15 or +1.13% at $549.95

- Silver up $0.55 or +0.85% at $66.017

- Platinum up $1.99 or +0.1% at $1923.74

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 19/12/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 19/12/2025 | 1200/1300 | ECB Cipollone Remarks, Roundtable at Aspen Institute | ||

| 19/12/2025 | 1200/1200 | BOE Market Participants Survey | ||

| 19/12/2025 | 1330/0830 | ** | Retail Trade | |

| 19/12/2025 | 1400/1500 | ** | BNB Business Confidence | |

| 19/12/2025 | 1500/1000 | *** | NAR existing home sales | |

| 19/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 19/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 19/12/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 19/12/2025 | 1510/1610 | ECB Lane Lecture at Central Bank of Ireland | ||

| 19/12/2025 | 1630/1630 | BOE to announce APF Q4 Sales Schedule | ||

| 19/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |