MNI US OPEN - Slack NFP Metrics Eyed, With Risks Rising

EXECUTIVE SUMMARY

- MNI US PAYROLLS PREVIEW - SLACK METRICS EYED WITH RISKS RISING

- FED’S GOOLSBEE SAYS HARD TO INTERPRET WEAKER JOB NUMBERS

- TRUMP GROWS PESSIMISTIC ABOUT THE PROSPECT OF ENDING THE RUSSIA-UKRAINE WAR

- UK RETAIL SALES STRONGER M/M BUT ONLY BECAUSE OF DOWNWARD REVISIONS

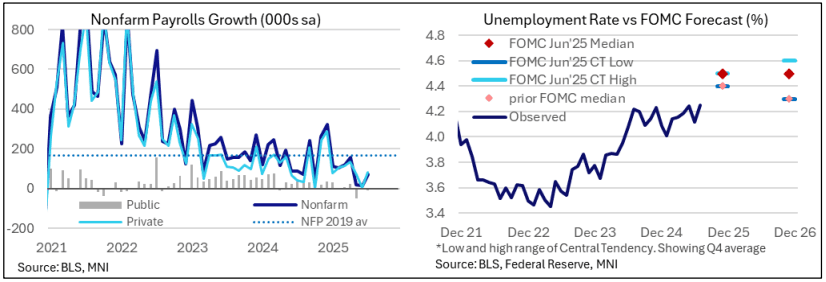

Figure 1: Recent US labour market developments

NEWS

MNI US PAYROLLS PREVIEW: Slack Metrics Eyed With Risks Rising

Nonfarm payrolls growth is seen at 75k in August (sa) per the broad Bloomberg survey, after 73k in July. Revisions are going to be particular focus after last month’s huge downward revisions heavily altered recent trends, with non-health private payrolls growth at best stalling for the past three months, and dominated the market reaction. The median primary dealer analyst eyes 70k whilst the Bloomberg whisper currently sits at 83k but with the ADP report still to come after publication of this preview.

FED (MNI): Hard to Interpret Weaker Job Numbers - Fed’s Goolsbee

Chicago Federal Reserve Bank President Austan Goolsbee said Thursday downward revisions to payroll employment are hard to interpret because they are happening at the same time as immigration restrictions, and he will take the upcoming August payroll figures with a grain or salt, focusing more closely instead on the jobless rate. Goolsbee said he still has not yet made up his mind on whether to support cutting interest rates in September, and is still balancing out growing concern about the labor markets with lingering worries about persistent inflation.

US/UKRAINE (NBC News): Trump Grows Pessimistic About the Prospect of Ending the Russia-Ukraine War

President Donald Trump has grown increasingly pessimistic about the chance of brokering an end to the Russia-Ukraine conflict anytime soon or seeing the leaders of the two warring countries meet in person, according to two senior administration officials. Trump isn’t abandoning hopes of settling the dispute: He joined a conference call Thursday with Ukrainian President Volodymyr Zelenskyy and European leaders, in which he stressed that “Europe must stop purchasing Russian oil that is funding the war,” a White House official said. Trump also made the point that European leaders must subject China to economic pressure for underwriting the Russian war effort, the official added.

US/INDIA (BBG): India Minister Says Don’t ‘Panic’ Over Delay in US Trade Deal

India’s Commerce and Industry Minister Piyush Goyal said negotiations with the US on the trade deal should be allowed to continue and that there was no need to “panic” over the delay. “We continue to have very good relations with the US, and I’m sure that we’ll be able to resolve some of these issues and come to an equitable, fair and balanced agreement,” Goyal said in an interview with news agency ANI. Formal talks between New Delhi and Washington are on pause at the moment after a US team canceled its trip to India in August.

US/JAPAN (BBG): Trump Signs Order Sealing Japan Tariff Deal With 15% Rate

President Donald Trump signed an executive order Thursday implementing his trade agreement with Japan, with a maximum 15% tariff on most of its products, including automobiles and parts. The deal, including a promise that Japan will create a $550 billion US investment fund, was reached in July, but had yet to be formalized as Washington and Tokyo haggled over its terms. Japan’s top trade negotiator, Ryosei Akazawa, who was in Washington this week for talks, met with Trump on Thursday, according to a US official.

US/MEXICO/CANADA (WSJ): Trump Prepares to Start North American Trade Deal Renegotiation

The U.S. is preparing to start renegotiating its largest free trade deal—the U.S.-Mexico-Canada Agreement. Within the next month, the Office of the U.S. Trade Representative will begin public consultations on renegotiating the deal, which it must do by Oct. 4 under the 2020 law that implemented the pact. A request for comment from companies and unions could be issued as soon as this week, say people familiar with the administration’s thinking, though President Trump’s team has previously indicated to stakeholders that a request was close, before pushing back the release date.

US (WaPo): Trump to Rebrand Defense Department as War Department

President Donald Trump is expected to rebrand the Defense Department to the Department of War through an executive order Friday, a move that the administration has said more accurately reflects the mission of the men and women serving in uniform today. “Restoring the name ‘Department of War’ will sharpen the focus of this Department on our national interest and signal to adversaries America’s readiness to wage war to secure its interests,” according to a document describing the forthcoming executive order.

UK (FT): Sharp Rise in UK Pension Lump Sum Withdrawals Over Tax Concerns

The amount withdrawn from UK pensions in tax-free lump sums rose more than 60 per cent over the past financial year as savers prepare for possible changes to the tax rules on retirement funds. The rush comes as the government announced in last October’s Budget that pensions would be subject to inheritance tax by April 2027, upending financial plans as retirement funds will no longer be a tax-efficient form of succession planning.

CHINA (MNI EXCLUSIVE): China Copper Demand Set to Ease Over H2

Local analysts provide insight into China's copper demand. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (BBG): Japan to Hike Minimum Pay by Record, Backing BOJ’s Rate Hikes

Japan will raise its minimum hourly wage by a record 6.3% to ¥1,121 ($7.56), reinforcing the nation’s wage-price cycle and supporting the case for the Bank of Japan to keep hiking rates. Prefectures nationwide will boost minimum pay by an average of ¥66 an hour in the current fiscal year, the labor ministry said Friday. The increase marked the largest since records began in 1978. The new wage level, which applies to about three million workers, will gradually take effect from October.

THAILAND (BBG): Thai Parliament Elects Anutin as Prime Minister

Bhumjaithai Party leader Anutin Charnvirakul is set to become Thailand’s new prime minister after securing enough votes in parliament, the latest development to ease a political deadlock following a court ruling that dismissed Paetongtarn Shinawatra as premier. Anutin secured enough votes in the 492-member House of Representatives with the backing of reform-minded People’s Party and a coalition of conservative parties on Friday, according to a televised session of the ongoing vote

DATA

UK DATA (MNI): Retail Sales Stronger M/M but Only Because of Downward Revisions

- UK JUL RETAIL SALES +0.6% M/M, +1.1% Y/Y

- UK JUL RETAIL SALES EX-FUEL +0.5% M/M, +1.3% Y/Y

Retail sales came in stronger than expected in July, but only because of downward revisions to August data. The past series has changed to be quite a lot weaker through late 2024 and 2025 due to the errors. The ONS estimates that the retail sales contribution in Q2-25 remains at 0.02ppt while Q1-25 has been revised down to 0.03ppt from 0.06ppt, but notes that to 1dp this would leave Q1 GDP unrevised at 0.7%. In terms of market reaction - retail sales data had been holding up pretty well overall in recent months. So today's corrections / revisions take some of the shine off of that. It's unlikely to materially change any MPC member's vote, but the market does sometimes still react to these data.

EUROZONE Q2 GDP +0.1% Q/Q, +1.5% Y/Y (VS +0.6% Q/Q, +1.6% Y/Y Q1) (MNI)

GERMAN DATA (MNI): Core Measure and Revisions Take Away Some of Factory Orders Miss

- GERMANY JUL FACTORY ORDERS -2.9% M/M

Manufacturing orders weaker than expected on headline. Some of that is taken away through a positive core reading as well as a positive revision of the weak June data (which contributed to the 0.2pp Q2 GDP downward revision to -0.3% Q/Q). "When large-scale orders are excluded, new orders were 0.7% higher than in the previous month. The less volatile three-month on three-month comparison showed that new orders in the period from May 2025 to July 2025 were 0.2% higher than in the previous three months; when large-scale orders are excluded, new orders were down 1.3%.", Destatis comments.

ITALY DATA (MNI): Real Retail Sales Trend Remains Tepid

Italian nominal retail sales were flat M/M in July, but the more informative real retail sales series (not reported by BBG) instead fell 0.2% M/M (vs 0.6% in June, -0.5% in May). Looking through monthly volatility, the trend in real retail sales remains tepid, with little discernible growth seen over the past two years. This has contributed to weak household consumption growth in the national accounts, with consumption flat in Q2 after just 0.2% Q/Q growth in Q1 and Q4.

SWEDEN DATA (MNI): Budget Balance Moves Into Surplus in Aug; Nov Borrowing Report in Focus

The Swedish budget balance registered a surplus of SEK42.9bln in August, above the National Debt Office's (NDO's) SEK32.6bln projection. This means the cumulative forecast budget balance forecast error from the May borrowing report has been erased. The NDO notes that "net lending to government agencies etc. was SEK 9.8

billion lower than the forecast. The difference is mainly due to higher deposits from the Swedish Pension Agency and The Swedish Defence Materiel Administration".

JAPAN DATA (MNI): Japan July Real Wages Positive Since Dec

The inflation-adjusted real wage, a key gauge of households’ purchasing power, turned positive in July for the first time since December 2024, rising 0.5% y/y after -0.8% in June, preliminary data from the Ministry of Health, Labour and Welfare showed Friday. The rebound was driven by higher bonuses and wage hikes from annual labour negotiations. While supportive for the Bank of Japan’s case to raise rates, officials see the data as insufficient on its own, with focus instead on the likelihood of wage gains carrying into fiscal 2026.

JAPAN DATA (MNI): Household Spending Below Forecast, But Wedge With Real Wages Removed

- JAPAN JULY HOUSEHOLD SPENDING +1.4% Y/Y; JUNE +1.3%

Japan July real household spending was a touch below forecasts. We rose 1.4%y/y, against a 2.3% forecast and 1.3% outcome in June. In m/m terms, we rose a solid 1.7%. The chart below plots real spending and real earnings outcomes, both in y/y terms. Today's updates bring the two series a little more in line with each other. For a number of months spending trends looked too strong relative to a softer real earnings backdrop. In terms of the detail, food and housing spending was negative y/y, while strong gains were seen for transport and medical care.

FOREX: USD Weaker into NFP, At Risk of Correction on Stronger Print

- The USD trades weaker through to the NY crossover, with markets continuing to position for signals of a soft labour market and slowing economy in today's NFP print. Renewed USD sales through the European morning has the USD Index at new daily lows, despite generally light volumes across the board. The downtick in the dollar has the USD Index trading either side of the 50-dma, and weakness through 97.993 support would open 97.818 intraday: the 23.6% retracement for the downleg posted off the Aug27 high.

- AUD's new daily highs has the price narrowing in on resistance defined by the 15-min candle chart: 0.6550 marks the downtrendline drawn off the Sep 1st Europe AM high - touched twice since over the past 4 sessions. AUD and NZD are the firmest performers in G10 after the APAC session made light work in erasing a weaker Thursday close for NZD/USD.

- Naturally, the focus shifts to payrolls data in light of the recent string of soft job market data in the US: JOLTS, IJC and the employment components of ISM services & manufacturing all came in weaker-than-expected), which is helping weigh on the whisper number for today's print, down to 75k (inline with consensus) after holding between 80-85k just a few days ago.

- Alongside the US jobs print, Canada's August employment data also crosses, at which the unemployment rate is seen rising to 7.0%, matching the post-COVID high in the process. Into the data, the bull cycle in USDCAD that started mid-June remains in play. Near term, the recovery from the Aug 29 low highlights a potential early reversal signal and if correct, the end of the corrective pullback between Aug 22 - 29.

EGBS: Tight Ranges for Major Futures Ahead of US NFP

Bund futures have traded in a relatively contained 23 tick range this morning, currently +11 ticks at 128.55. Global focus remains on the US labour market report at 1330BST/1430CET.

- The weaker-than-expected German July factory orders reading helped Bunds pierce yesterday’s high at the old cash open (128.74 vs yesterday's high of 128.68), but the move lacked traction. That means key short-term resistance at 128.87 (Aug 28 high) remains intact. Until the Aug 28 high is broken, recent gains will be considered corrective.

- Eurozone final Q2 GDP was confirmed at 0.1% Q/Q, with details suggesting an upward contribution from inventories was key in avoiding a negative sequential reading. That said, a more hawkish readthrough came from the Q2 compensation per employee print, which exceeded ECB forecasts. Overall, there was limited market reaction to the data, with expectations already well set for next week’s ECB decision.

- German yields are little changed across the curve. While 10-year Bund yields met resistance at 2.80% earlier this week, the 2.70% handle looks to be containing downside today.

- 10-year EGB spreads to Bunds remain tighter despite a pullback in European equities from session highs. The BTP/Bund spread is back at 83.5bps, after almost testing 90bps on Tuesday afternoon. In France, focus remains on the fallout from Monday’s no-confidence vote.

- Belgium will hold a E500mln ORI operation at 1100BST.

GILTS: Off Early Highs, Curve a Little flatter Again

Gilts continue to trade below early session highs, taking cues from core global FI peers, with tight ranges in play ahead of the impending U.S. NFP release.

- Futures traded as high as 90.87, before moving back to and stabilising around 90.70.

- The Aug 28 & 29 highs (90.84) were pierced during the opening rally. Fresh extension higher would target key near-term resistance at the August 18 high (91.24).

- A break of the latter would increase the risk to the bearish technical cycle, with the recent bounce reflecting an unwind of oversold conditions at this stage.

- Yields are flat to 1.5bp lower, curve flatter.

- 10s and 30s are ~20bp off this week’s highs, although their uptrends remain intact.

- Similarly, steepening technical trends in 2s10s and 5s30s remain intact, despite the pullback from this week’s highs.

- GBP STIRs little changed vs. late Thursday levels.

- Just under 10bp of BoE easing showing through year-end, SONIA futures -0.5 to +2.5.

- Firmer-than-expected UK retail sales data was seen pre-open, although the upside surprise was driven by revisions/corrections to the series. The data won’t change the BoE outlook.

- Fiscal worries and headwinds for Deputy PM Rayner continue to headline UK news flow.

- The DMO revealed that the Thursday 11 Sep PGT will be the first that will see multiple lines offered.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.974 | +0.7 |

Nov-25 | 3.927 | -4.0 |

Dec-25 | 3.877 | -9.0 |

Feb-26 | 3.776 | -19.1 |

Mar-26 | 3.738 | -22.9 |

Apr-26 | 3.668 | -29.9 |

EQUITIES: Latest Pullback for E-Mini S&P Appears to Be Only a Shallow Correction

The primary trend set-up in Eurostoxx 50 futures is bullish, however a corrective bear cycle remains in play. Recent weakness resulted in a breach of 5370.73, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, initial resistance to watch is 5384.25, the 20-day EMA. A clear break of it would be bullish. A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract has traded to a fresh cycle high, breaching the Aug 28 high of 6523.00. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a Fibonacci projection. Initial support to watch is 6447.06, the 20-day EMA.

- Japan's NIKKEI closed higher by 438.48 pts or +1.03% at 43018.75 and the TOPIX ended 25.14 pts higher or +0.82% at 3105.31.

- Elsewhere, in China the SHANGHAI closed higher by 46.638 pts or +1.24% at 3812.514 and the HANG SENG ended 359.47 pts higher or +1.43% at 25417.98.

- Across Europe, Germany's DAX trades higher by 49.22 pts or +0.21% at 23819.09, FTSE 100 higher by 29.72 pts or +0.32% at 9246.61, CAC 40 up 9.37 pts or +0.12% at 7708.29 and Euro Stoxx 50 up 10.65 pts or +0.2% at 5357.36.

- Dow Jones mini up 8 pts or +0.02% at 45696, S&P 500 mini up 14 pts or +0.22% at 6524.75, NASDAQ mini up 105.75 pts or +0.45% at 23773.5.

Time: 10:00 BST

COMMODITIES: Recent Move Lower for WTI Futures Signals End of Corrective Phase

A bear cycle in WTI futures remains intact and the latest bull phase appears to have been a correction. Tuesday’s move down highlights a possible early reversal signal and the end of the corrective phase. Initial resistance to watch is $66.56, the Aug 4 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low. Gold is unchanged, it remains in a clear bull cycle and trades closer to its recent highs. This week’s gains resulted in a breach of key resistance at $3500.1, the Apr 22 high, and delivered a fresh all-time high in the yellow metal. The break confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3600.00. Initial firm support lies at $3424.5, the 20-day EMA.

- WTI Crude down $0.12 or -0.19% at $63.32

- Natural Gas up $0.03 or +1.01% at $3.105

- Gold spot up $0.08 or +0% at $3545.17

- Copper up $3.15 or +0.69% at $459

- Silver up $0.11 or +0.26% at $40.7765

- Platinum up $4.88 or +0.35% at $1382.05

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 05/09/2025 | 1230/0830 | *** | USDA Crop Estimates - WASDE | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Labour Force Survey | |

| 05/09/2025 | 1400/1000 | * | Ivey PMI | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |