FOREX: USD Weaker into NFP, At Risk of Correction on Stronger Print

Sep-05 09:09

- The USD trades weaker through to the NY crossover, with markets continuing to position for signals of a soft labour market and slowing economy in today's NFP print. Renewed USD sales through the European morning has the USD Index at new daily lows, despite generally light volumes across the board. The downtick in the dollar has the USD Index trading either side of the 50-dma, and weakness through 97.993 support would open 97.818 intraday: the 23.6% retracement for the downleg posted off the Aug27 high.

- AUD's new daily highs has the price narrowing in on resistance defined by the 15-min candle chart: 0.6550 marks the downtrendline drawn off the Sep 1st Europe AM high - touched twice since over the past 4 sessions. AUD and NZD are the firmest performers in G10 after the APAC session made light work in erasing a weaker Thursday close for NZD/USD.

- Naturally, the focus shifts to payrolls data in light of the recent string of soft job market data in the US: JOLTS, IJC and the employment components of ISM services & manufacturing all came in weaker-than-expected), which is helping weigh on the whisper number for today's print, down to 75k (inline with consensus) after holding between 80-85k just a few days ago.

- Alongside the US jobs print, Canada's August employment data also crosses, at which the unemployment rate is seen rising to 7.0%, matching the post-COVID high in the process. Into the data, the bull cycle in USDCAD that started mid-June remains in play. Near term, the recovery from the Aug 29 low highlights a potential early reversal signal and if correct, the end of the corrective pullback between Aug 22 - 29.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: EUROZONE JUN RETAIL SALES +0.3% M/M, +3.1% Y/Y

Aug-06 09:00

- MNI: EUROZONE JUN RETAIL SALES +0.3% M/M, +3.1% Y/Y

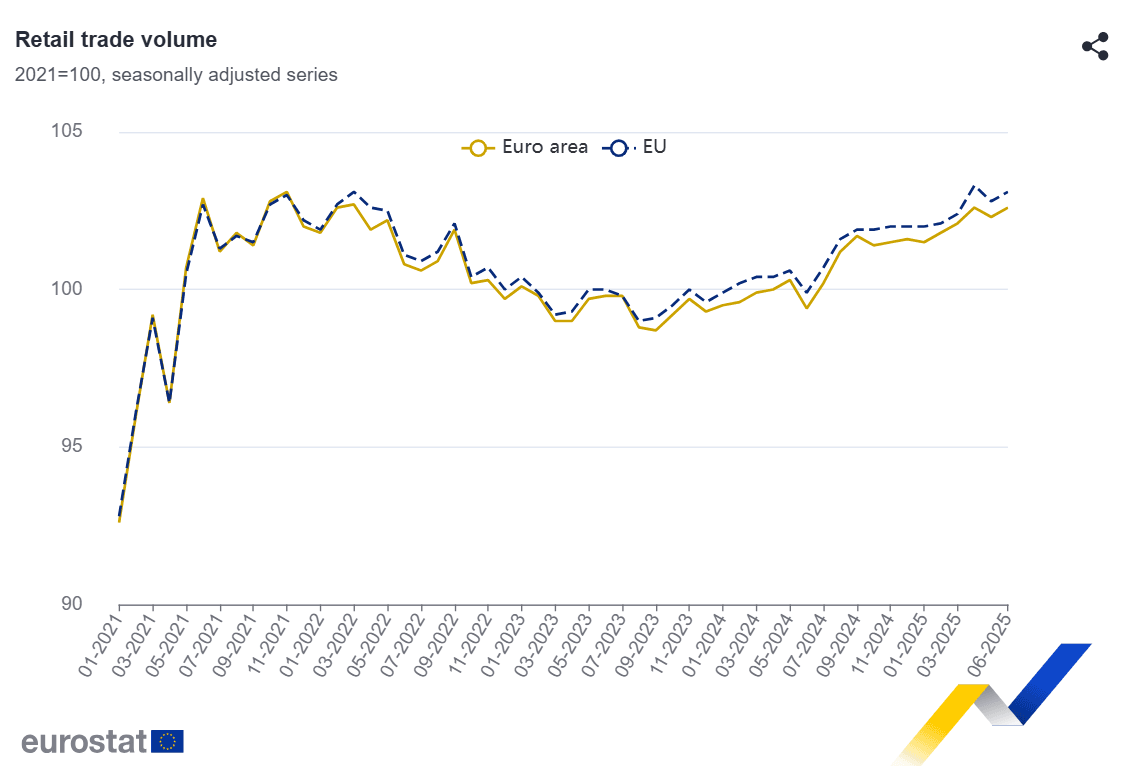

EUROZONE DATA: June Retails Sales Stronger Than Expected After Revisions

Aug-06 09:00

Eurozone (real) retail sales were inline with expectations in June on a sequential comparison, at 0.3% M/M, but the print was stronger on a level basis considering a positive revision to May (now -0.3%, revised from -0.7%). The uptrend in place since late-2023 continues even the level is still a little below 2021 highs.

- Across sectors, all main categories rose after across the board declines in May: Food, drinks, tobacco 0.2% M/M, non-food products ex automotive fuel 0.6%, automotive fuel 0.4%. None of the categories stand out in in YTD directional trends.

- Across countries, the June print was a bit mixed, with three out of the "big 4" printing positive but France weak at -0.9% M/M.

- The overall Y/Y print was 3.1% in June, firmer than consensus of 2.6% (1.9% May, revised from 1.8%). Across categories, non-food products and auto fuel continue to fare better Y/Y than the food, drinks, tobacco category.

- Eurozone consumer confidence ticked up a little most recently but remains subdued: "Consumers’ perception of their households’ financial situation, both backward- and forward-looking, and their intentions to make major purchases improved, while their expectations about the general economic situation in their country worsened", the European Commission commented on the latest respective release.

- A June McKinsey study found that inflation remains consumers' main concern in the EU, although this has decreased compared with last year.

GERMAN DATA: SME Sentiment Remains On Track For Recovery - KfW

Aug-06 08:56

"German SMEs are increasingly optimistic about the coming months. As a result, the business climate in the sector rose for the fifth time in a row in July – this time by 1.6 points to minus 12.4 points. Although this is still below the long-term average, which is marked by the zero line, the economic upturn seems within reach." - via KfW

- "Although small and medium-sized enterprises rated their current situation only marginally better than in the previous month, their business expectations for the next six months rose significantly, pushing the index further out of its slump."

- The KfW SME Barometer is produced by IFO and is based on the "institute's economic surveys" - so some correlation with the broader IFO business climate (which has been trending upwards this year) does not come unexpected.

- Business sentiment in Germany is, on balance, trending upwards more broadly, with also the Manufacturing PMI standing at cycle highs. The services PMI meanwhile has seen some volatility but little overarching directional trend this year.

Trending Top

Jun-26 16:22