MNI US Macro Weekly: Softer Labor Data Opens Way To Fed Cuts

Sep-05 19:50By: Tim Cooper and 1 more...

Federal Reserve+ 1

Download Full Report Here

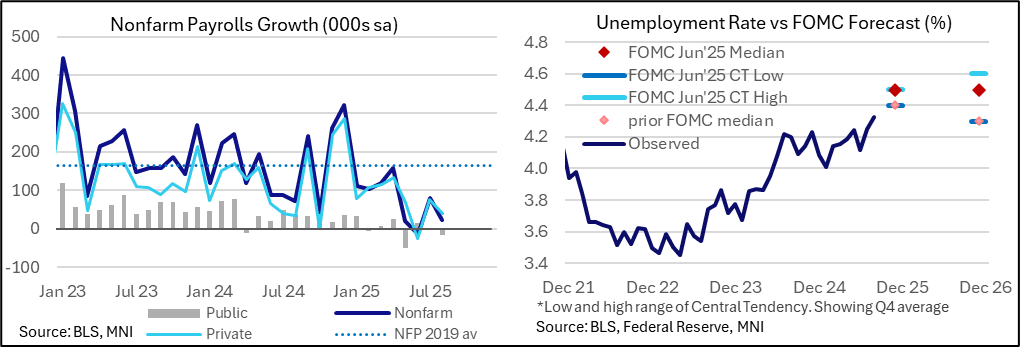

- A September Fed rate cut now looks assured after the August nonfarm payrolls report surprised on the dovish side for both payrolls employment and the unemployment rate.

- Along with other soft jobs data seen this week (ADP, JOLTS), the report confirmed that there are indeed rising downside risks to employment but also that the “curious” kind of balance in the labor market, per Chair Powell’s words at Jackson Hole, remains in play, even as inflation risks linger.

- Powell made those comments in the context of a broader speech suggesting that rate cuts could resume soon, and Fed Funds futures point to 27.5bp of cuts for the Sept 17 decision vs 25bp pre-NFP release.

- Other data seen this week painted a relatively more positive picture of economic activity for the most part. GDP nowcasts suggest above-trend growth in Q3, with services activity (per ISM and PMI) at some of its strongest levels of the year in August.

- Offsetting this were further deterioration in construction and weak signs from the manufacturing sector, which judging from latest ISM Manufacturing and factory orders has been unable to regain traction after tariff-related volatility earlier in the year.

- Similarly, a surprisingly large July trade deficit showed little limited normalization on the external front.

- The last week of Fedspeak ahead of the pre-FOMC blackout period was dominated by current voters, only one of which (Waller) made an explicit case for a September easing. Goolsbee (who spoke after the nonfarm payrolls data), Musalem and Williams sounded more cautious than Waller, though we're not sure any of them would dissent to a cut (though admittedly upcoming CPI data adds some uncertainty).

- While Board of Governors nominee Miran would be almost certain to support a cut, it's unclear whether he will be confirmed by the Senate in time for the Sept 16-17 meeting. On that note, we continue to await news on Governor Cook’s ability to participate, which appears to be in the hands of the courts.

- Meanwhile, the latest Beige Book described price pressures remaining modestly/moderately to the upside while labor market conditions have weakened.

- Next week sees key data for both sides of the Fed’s mandate, starting with Tuesday’s release of preliminary estimates of benchmark payrolls revisions, based off QCEW data for Q1, followed by US PPI Wednesday before CPI inflation on Thursday.