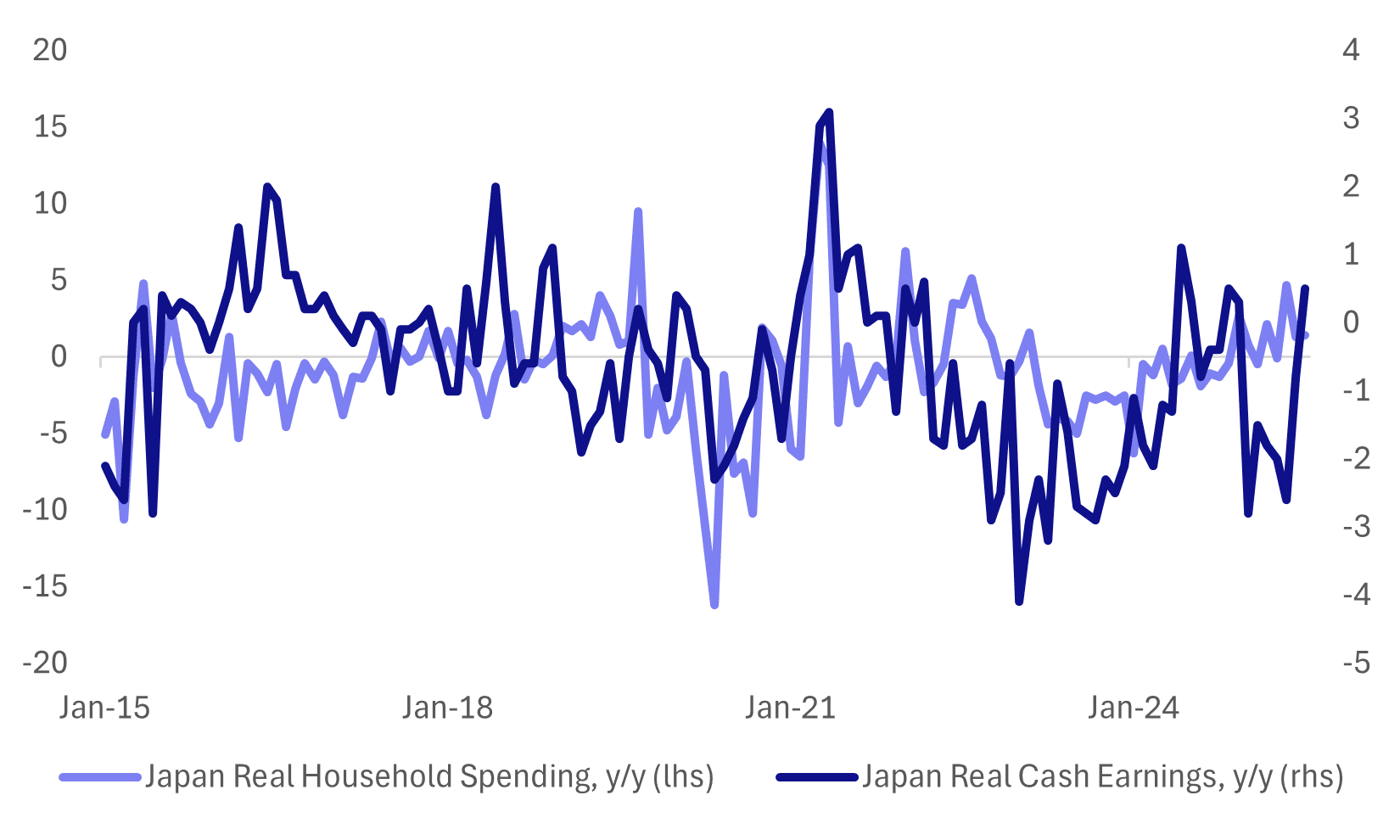

JAPAN DATA: Household Spending Below Forecast, But Wedge With Real Wages Removed

Japan July real household spending was a touch below forecasts. We rose 1.4%y/y, against a 2.3% forecast and 1.3% outcome in June. In m/m terms, we rose a solid 1.7%. The chart below plots real spending and real earnings outcomes, both in y/y terms. Today's updates bring the two series a little more in line with each other. For a number of months spending trends looked too strong relative to a softer real earnings backdrop. In terms of the detail, food and housing spending was negative y/y, while strong gains were seen for transport and medical care.

Fig 1: Japan Real Household Spending & Real Earnings Y/Y

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cash Open

TYU5 is trading 112-05+, down 0-04 from its close.

- The US 2-year yield opens around 3.722%.

- The US 10-year yield opens around 4.214%.

- Bloomberg - “JPMorgan’s Treasury Client Survey for the week ended Aug.4 showed longs rose 5ppts to its highest since April 14 in a shift from neutrals with shorts unchanged on the week. Net long position was the biggest since July 7.”

- MNI US DATA: US-China Goods Deficit At Smallest Since At Least 2009. There weren’t any major surprises in the final goods & services trade data for June as last week’s surprisingly small goods deficit in the advance report had already set the tone. US trade deficits with both the EU and China narrowed further, with the goods deficit to China of 0.6% GDP in Q2 the lowest quarterly deficit since at least 2009.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area.

- Data/Events: MBA Mortgage Applications

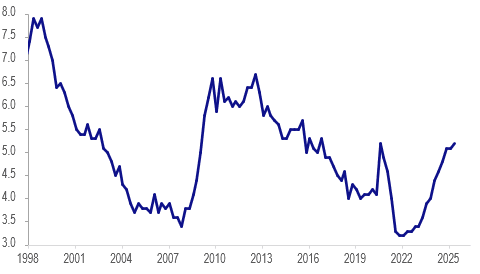

NEW ZEALAND: Q2 Sees Increased Labour Market Capacity

NZ employment was weaker in Q2 than the RBNZ projected in May declining 0.1% q/q and 0.9% y/y, in line with consensus, after a downwardly-revised 0.0% q/q & -0.7% y/y in Q1. The unemployment rate rose 0.1pp to 5.2%, highest since Covid-impacted Q3 2020, but as the RBNZ forecast. The next rate decision is on August 20 and will include an updated outlook. With job shedding continuing and activity indicators remaining lacklustre and inflation in the band, another 25bp rate cut is likely.

NZ unemployment %

Source: MNI - Market News/LSEG

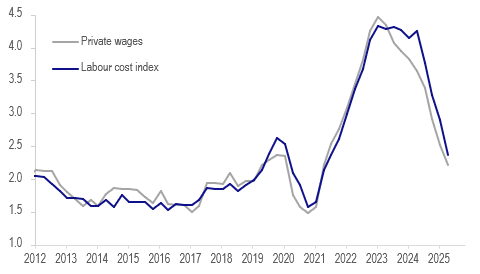

- With excess supply in the labour market, wage inflation continues to moderate. April 1 pay rises are included in the Q2 data boosting the quarterly rates but they were below Q2 2024.

- Q2 labour costs rose 0.6% q/q to be up 2.4% y/y down from 2.9% y/y in Q1 and the slowest rate since Q2 2021. Private wages rose 0.6% q/q to moderate to 2.2% y/y from 2.5%, lowest since Q1 2021.

NZ wages y/y%

- Underutilisation continues to trend higher too. It troughed recently at 9% in Q3 2022 and rose 0.4pp to 12.8% in Q2, the highest since Q3 2020. It is up 0.9pp since Q2 2024.

- The participation rate fell 0.2pp to 70.5%. There was a 5% y/y rise in 15-24 year olds in education which is probably being driven by difficulties in finding employment. The employment rate for this age group is down 3pp to 53.1%.

JGBS: Futures Weaker Overnight, Cash Earnings Due

In post-Tokyo trade, JGB futures closed weaker, -11 compared to settlement levels, after US tsys lost ground on Tuesday following stagflationary signals from the July services ISM and after a disappointing 3-year auction.

- US yields ended mostly higher, led by the short end with the 2-year cheapening 5bps to 3.72%. The 10-year yield was up 2bps to 4.21% while the 30-year was 1bp lower at 4.78%. Bonds focused on the pop in the prices paid component that slightly softened September Fed rate cut hopes.

- Bloomberg - " In a break from a decades-old policy, the Japanese government will encourage farmers to disregard a de facto cap on rice production and boost cultivation of the food staple, a step that could win support from the agriculture sector and soothe consumers' frustration over soaring living costs."

- (Bloomberg) - "The Japanese yen has rallied more than 2% so far this month, among the biggest gainers out of 31 G-10 and EM currencies tracked by Bloomberg. The outperformance will persist as stalling US economic growth boosts the yen's haven appeal, while seasonal patterns support an extension of the rally."

- Today, the local calendar will see Cash Earnings data.