JGBS: Offshore Session Highs But Positive Bias Intact, JGB Curve Flatter

JGB futures sit off earlier highs, last 137.82, +.19 versus settlement levels. We got o 137.93 in the first of dealing, which is a fresh high back to mid August. US Tsy futures have maintained an early positive bias, 10yr TY futures just off session highs in latest dealings (+03+ to 112-30+).

- Earlier data, which showed stronger than expected July labor earnings data may have helped temper JGB futures gains. Still, the data was aided by stronger bonus payments, which tend to be volatile, while core earnings were relatively steady. Household spending for July was also a touch below market expectations, but remained positive.

- In the cash JGB space, yields are down across most benchmarks. The 30-yr is the softest, off close to 3bps to be back near 3.24%, while the 10yr is near 1.585%. In the swap space, the 10yr rate is under 1.40%.

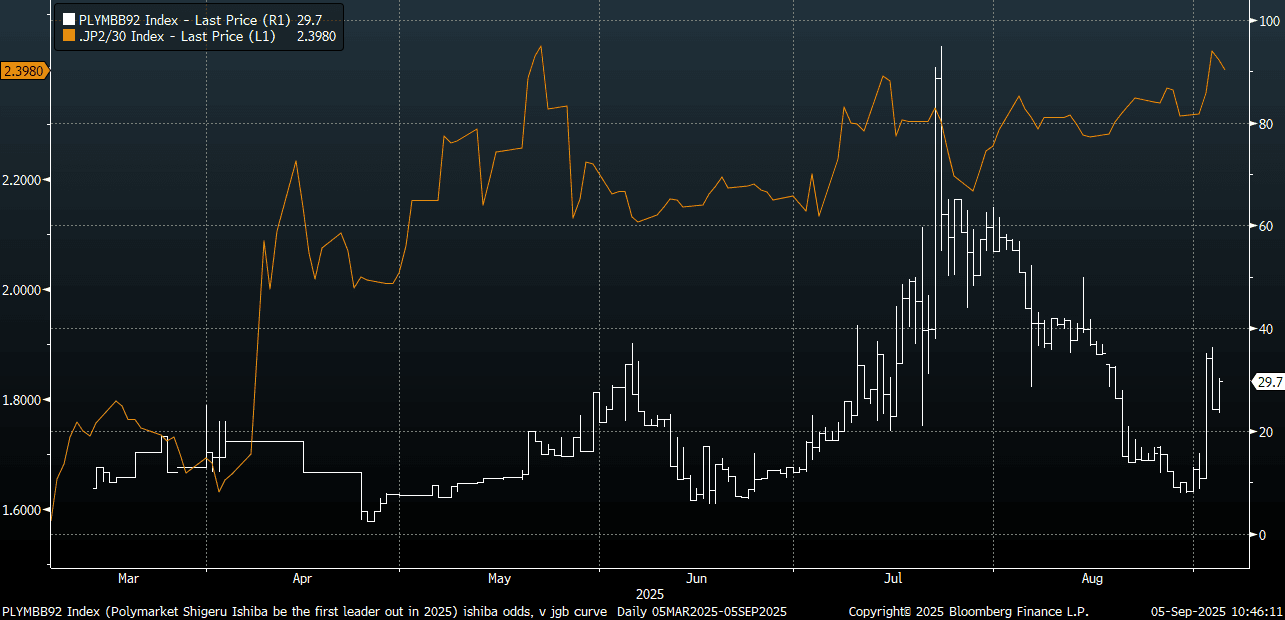

- The JGB 2/30's curve is flatter, back to +240bps. The chart below overlays this curve against PM Ishiba removal odds for 2025 (via Polymarket). In general, Ishiba's removal will create fresh political uncertain and potentially further push back BoJ tightening expectations.

- These odds are well below 2025 highs but have ticked up ahead of a possible LDP leadership election this coming Monday.

- Later on today we get leading and coincident indices for July. Next Monday, Q2 GDP revisions are out.

Fig 1: JGB 2/30's Curve & Ishiba Removal Odds

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: ACGB Mar-36 Supply Faces Lower Yield With A Similar Curve

The Australian Office of Financial Management (AOFM) will today sell A$900mn of the 4.25% 21 March 2036 bond. The line was last sold on 16 July 2025 for A$800mn. This new line was sold by syndication on 5 February 2025 for A$15.0bn. Bidding at today’s auction is likely to be shaped by several key factors:

- The outright yield is roughly 20bps lower than the previous auction level and about 30bps below the late February peak.

- However, the 3/10 yield curve is similar to the previous auction level and sits around 30bps flatter than its recent high.

- On the other hand, sentiment toward longer-dated global bonds has improved over the past week.

- This bond is also included in the XM futures basket, which may support demand.

- Overall, firm pricing is still anticipated at today’s auction, given the higher yields and other favourable factors.

- Results are due at 0200 BST / 1100 AEST.

AUSSIE BONDS: AUCTION PREVIEW: ACGB Mar-36 Supply Due

The Australian Office of Financial Management (AOFM) will today sell A$900mn of the 4.25% 21 March 2036 bond. The line was last sold on 16 July 2025 for A$800mn. The sale drew an average yield of 4.4476%, a high yield of 4.4500% and was covered 4.0000x. This new line was sold by syndication on 5 February 2025 for A$15.0bn.

- This week's ACGB supply is at the top end of the recent average weekly issuance of $1500-2200mn, with A$300mn of the 4.25% 21 June 2034 bond issued on Tuesday and A$1000mn of the 3.00% 21 November 2033 bond due on Friday.

- During the first half of 2025-26, the AOFM plans to: issue a new October 2036 Treasury Bond (by syndication and subject to market conditions); conduct 2 Treasury Bond tenders most weeks; hold 1-2 Treasury Indexed Bond tenders each month.

- Issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds in 2025-26 is expected to be between $2 billion and $3 billion.

- Results are due at 0200 BST / 1100 AEST.

US STOCKS: ISM Services Flashes Stagnation, S&P Wavers

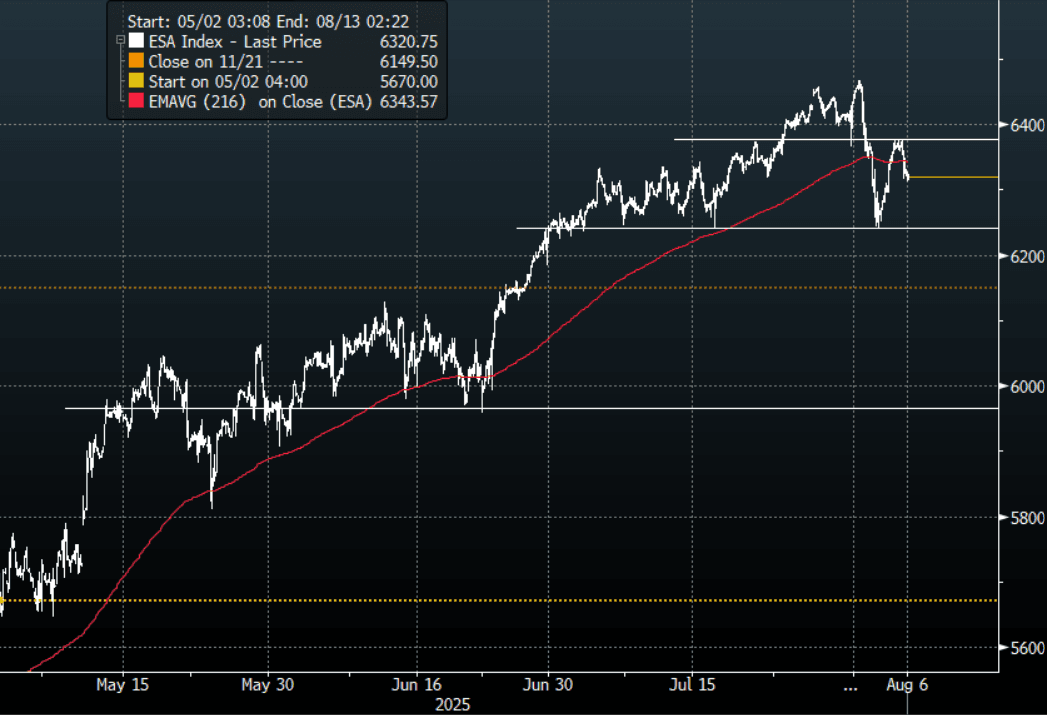

The ESU5 overnight range was 6315.50 - 6377.50, Asia is currently trading around 6322. The ESU5 contract stalled back towards 6400 and a poor ISM services report saw it trade heavy for the whole N/Y session. The market is trying to ignore the worries about growth that would make the cuts possible but the ISM services data shows these headwinds are increasing. This morning has seen US futures open a little lower, ESU5 -0.10%, NQU5 -0.20%. Price bounced strongly off its first support around 6200/6250, I suspect bounces back towards 6350/6400 should now initially find sellers as we enter a poor period based on seasonality. A break below 6200 is needed to potentially signal a deeper correction back to the 5900/6000 area.

- (Bloomberg) - The latest ISM Services report adds to evidence that the tariff impact on the economy is only starting to show, which helps explain the dissonance between the real economic data and corporate earnings.

- Craig Fuller on X: “The freight market has been sending flashing warning signs since mid February. But since the stock market has been rallying and government data has been wrong, no one has noticed the collapse in the Main Street economy.”

- Lance Roberts on X: ”Goldman's Cullen Morgan reveals that CTAs are now pretty much full, and the bank estimates that CTAs are long $159bn of global equities (100th %tile) and $50bn of US equities (92nd %tile). Such skews the risk of the next market move to the downside."

- Daily Chartbook on X: CTAs: "Estimates over the next week and month are skewed to the downside. We have CTAs as sellers of global equities in every scenario over the next week (concentrated mostly in Europe)."-GS

- Keith McCullough on X: “ One of the biggest things Consensus Bears have had dead wrong is the strength (and breadth) of US Earnings Season ”

Fig 1: SPX(ESU5) Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P