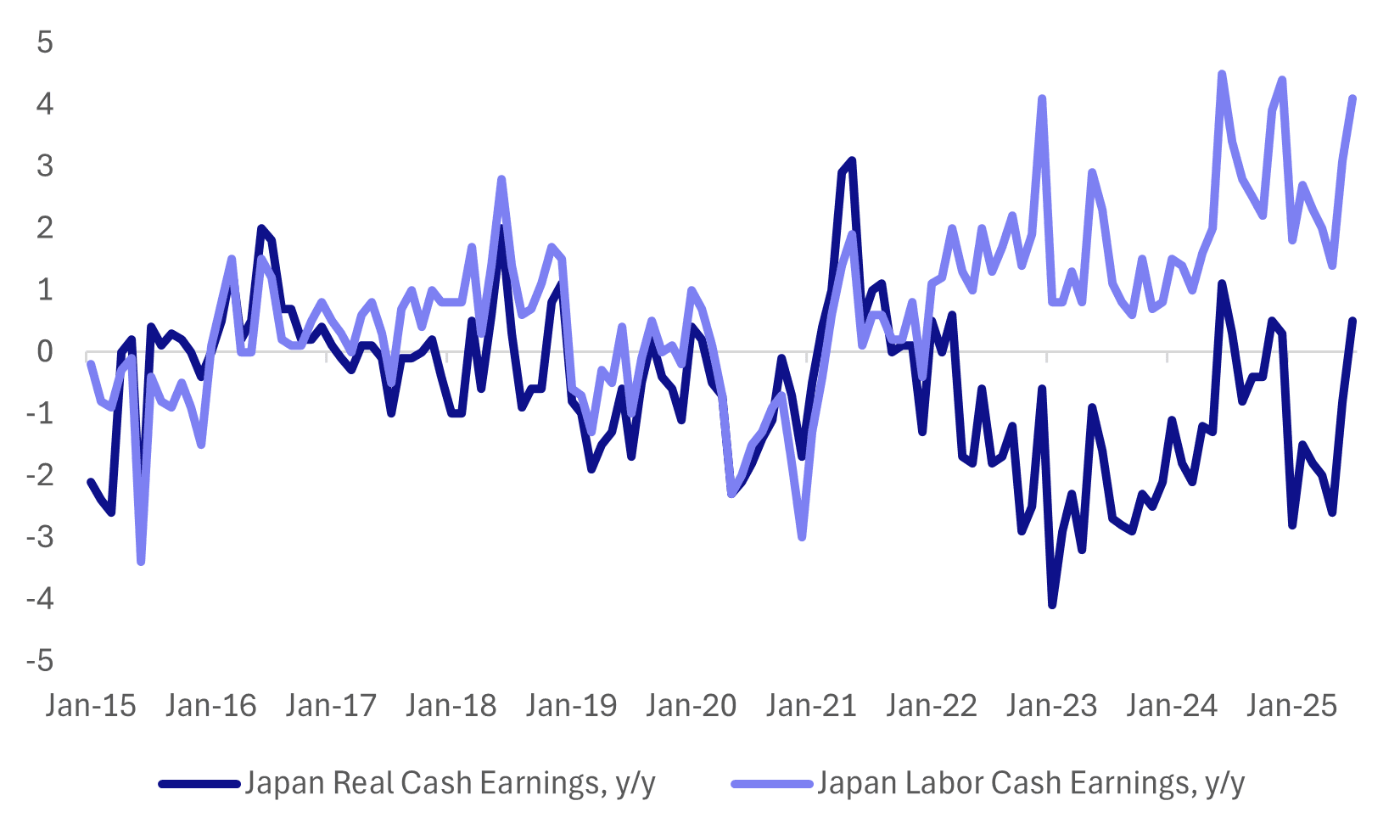

JAPAN DATA: July Cash Earnings Beat Estimates, Aided By Bonus Payments

Japan July labor earnings data was mostly better than forecast. The headline nominal read was +4.1%y/y, against a forecast rise of 3.0% and prior 3.1% (which was revised higher from the initial 2.5% estimate). In real terms, cash earnings rose 0.5%y/y, against a 0.6% forecast and -0.8% prior. The chart below plots nominal and real earnings in y/y terms.

- On a same sample base, cash earnings rose 2.9%, versus the 3.3% forecast (although June was revised up to 3.4% from 3.0%). Scheduled full time pay (same base) rose 2.4%y/y, versus 2.5% forecast and 2.3% prior.

- Bonus payments were up 7.9%y/y in July, versus 4.4% for June. This was the strongest rise since the 14.5% gain in March. This component can be volatile, so if we see a pull back in August it could weigh on the headline earnings outcomes.

- Scheduled full time pay, on a same sample base, painted a resilient picture with earnings up 2.4%y/y for the third straight month. We are off 2024 highs for this metric of 3%y/y, but are still well above historical averages.

- The authorities continue to see sustained positive real wages growth as a key policy goal. Today's data is a step in the right direction, but such trends have been elusive to maintain in recent years.

- From a BoJ standpoint, the result is welcome, but may not change near term thinking, given bonuses were a factor in the upside surprise. It is watching the tariff impact on corporate profitability and flow on effects closely. Household spending for July was also a touch below expectations.

Fig 1: Japan Nominal & Real Earnings Bounce In July

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

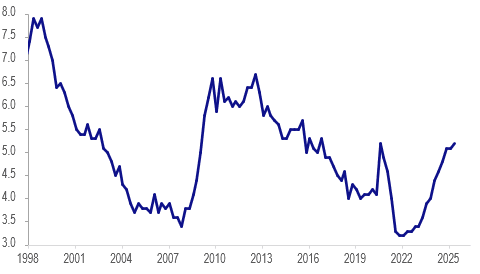

NEW ZEALAND: Q2 Sees Increased Labour Market Capacity

NZ employment was weaker in Q2 than the RBNZ projected in May declining 0.1% q/q and 0.9% y/y, in line with consensus, after a downwardly-revised 0.0% q/q & -0.7% y/y in Q1. The unemployment rate rose 0.1pp to 5.2%, highest since Covid-impacted Q3 2020, but as the RBNZ forecast. The next rate decision is on August 20 and will include an updated outlook. With job shedding continuing and activity indicators remaining lacklustre and inflation in the band, another 25bp rate cut is likely.

NZ unemployment %

Source: MNI - Market News/LSEG

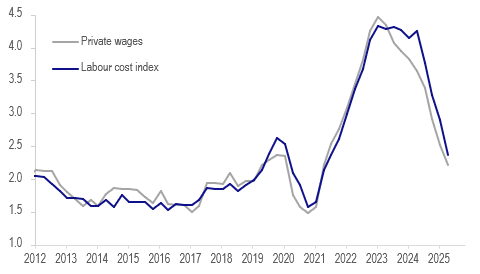

- With excess supply in the labour market, wage inflation continues to moderate. April 1 pay rises are included in the Q2 data boosting the quarterly rates but they were below Q2 2024.

- Q2 labour costs rose 0.6% q/q to be up 2.4% y/y down from 2.9% y/y in Q1 and the slowest rate since Q2 2021. Private wages rose 0.6% q/q to moderate to 2.2% y/y from 2.5%, lowest since Q1 2021.

NZ wages y/y%

- Underutilisation continues to trend higher too. It troughed recently at 9% in Q3 2022 and rose 0.4pp to 12.8% in Q2, the highest since Q3 2020. It is up 0.9pp since Q2 2024.

- The participation rate fell 0.2pp to 70.5%. There was a 5% y/y rise in 15-24 year olds in education which is probably being driven by difficulties in finding employment. The employment rate for this age group is down 3pp to 53.1%.

JGBS: Futures Weaker Overnight, Cash Earnings Due

In post-Tokyo trade, JGB futures closed weaker, -11 compared to settlement levels, after US tsys lost ground on Tuesday following stagflationary signals from the July services ISM and after a disappointing 3-year auction.

- US yields ended mostly higher, led by the short end with the 2-year cheapening 5bps to 3.72%. The 10-year yield was up 2bps to 4.21% while the 30-year was 1bp lower at 4.78%. Bonds focused on the pop in the prices paid component that slightly softened September Fed rate cut hopes.

- Bloomberg - " In a break from a decades-old policy, the Japanese government will encourage farmers to disregard a de facto cap on rice production and boost cultivation of the food staple, a step that could win support from the agriculture sector and soothe consumers' frustration over soaring living costs."

- (Bloomberg) - "The Japanese yen has rallied more than 2% so far this month, among the biggest gainers out of 31 G-10 and EM currencies tracked by Bloomberg. The outperformance will persist as stalling US economic growth boosts the yen's haven appeal, while seasonal patterns support an extension of the rally."

- Today, the local calendar will see Cash Earnings data.

AUSSIE BONDS: Flat, US Tsys Twist-Flatten After Services PMI

ACGBs (YM flat & XM flat) are unchanged after US tsys finished mixed Tuesday, curves twist-flattened.

- The headline Services PMI reading fell by 0.7 points to 50.1 (51.5 expected, 50.8 prior), merely a 2-month low but suggesting that an anticipated pickup in momentum and sentiment is not materialising.

- Trump spoke on his possible Fed picks to replace Kugler following her resignation over the weekend. The President declared he had a shortlist of 4, which includes both Kevin Warsh and Kevin Hassett, and while the President said he may use this Fed pick as a precursor to selecting the next Fed chair, he remained vague about the timing of such an announcement.

- Cash ACGBs are unchanged with the AU-US 10-year yield differential at +1bp.

- The bills strip is weaker, with pricing -1 to -2.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in August is given a 100% probability, with a cumulative 64bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Today, the local calendar will be empty apart from the AOFM planned sale of A$900mn of the 4.25% 21 March 2036 bond. A$1000mn of the 3.00% 21 November 2033 bond is planned for Friday.