MNI US OPEN - Reeves to Drop Plans to Raise Income Tax

EXECUTIVE SUMMARY

- REEVES TO DROP TAX-RISE PLANS BECAUSE OF BETTER UK FORECASTS

- CHINA AND US STILL TO AGREE ON RARE EARTH DEAL WEEKS AFTER TALKS

- ECB’S KAZAKS SAYS RATES APPROPRIATE, WILLING TO ADJUST IF NEEDED

- CHINA INDUSTRIAL PRODUCTION MISSES FORECASTS, RETAIL SALES STEADIES

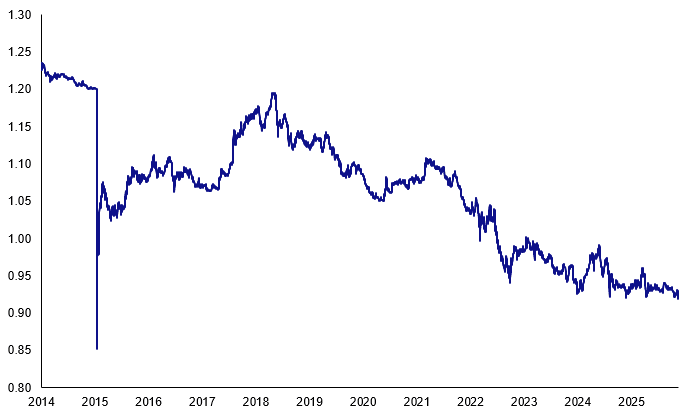

Figure 1: EUR/CHF briefly falls below 0.92 to lowest since withdrawal of 1.20 floor in 2015 (chart shows low price)

Source: MNI, Bloomberg Finance L.P.

NEWS

UK (BBG): Reeves to Drop Tax-Rise Plans Because of Better UK Forecasts

Chancellor of the Exchequer Rachel Reeves has been able to drop plans to raise income taxes because she received an improved fiscal forecast from the UK’s budget watchdog, people familiar with the matter said. The latest update from the Office for Budget Responsibility moved in a significantly more favorable direction due to the strength of government receipts and stronger wage performance, the people said, asking not to be named discussing sensitive matters. A fiscal hole predicted to be as wide as £35 billion ($46 billion) is in fact now closer to £20 billion, they said.

UK (X): Chancellor Will Still Increase Fiscal Headroom, Even Without Income Tax Rise - Peston

ITV’s Peston tweets “my sources insist that Rachel Reeves is NOT going to take greater risks with the public finances, which is what investors quite understandably fear is happening. I am being assured that whatever the eventual mix of tax rises in the budget, the Chancellor will increase “headroom” - the cushion - against future fiscal shocks from the current paltry £9bn to £15bn or more. “That will happen” said a source.”

UK (MNI): Is Income Tax U-Turn Enough To Save Reeves & Starmer?

The apparent U-turn from the gov't on planned increases in income tax in the 26 Nov budget, instead the gov't choosing to lower the higher rate income tax threshold clearly comes as a sign of the politics of the decision overcoming the economic concerns. It remains to be seen whether such a move will be enough to save the positions of Chancellor of the Exchequer Rachel Reeves and, indeed, embattled PM Sir Keir Starmer.

For Reeves, the tenability of her position could come down to the market reaction. The fact that Reeves is being forced into apparent late-notice changes to her budget due to political pressure from Labour backbenchers may raise market concerns that she has 'lost control' of the budget. For Starmer, who has endured a torrid 36 hours following anonymous briefings that senior cabinet figures were planning leadership challenges, the U-turn may be a last gamble to try and avoid a major backlash from a restless Parliamentary Labour Party concerned that it is seeing challenges on both the right (from Reform UK) and the left (from a resurgent Green Party) eat into their support.

GERMANY (BBG): Germany Lifts Planned Net New Borrowing for 2026 by €8 Billion

Net new borrowing by Germany’s federal government will be €8 billion ($9.3 billion) more than originally planned next year, according to the draft 2026 budget signed off by lawmakers on Friday. After talks in the lower house of parliament thrashing out the final details of next year’s finance plan, new borrowing was set at €98 billion, up from €90 billion in a previous draft, according to a document seen by Bloomberg.

US/CHINA (BBG): China and US Still to Agree on Rare Earth Deal Weeks After Talks

The US and China are still negotiating over the key details of how Beijing will free up sales of rare earths, according to a person familiar with the matter, weeks after a trade truce that Washington said would pave the way for increased exports. The two sides have given their teams until the end of November to agree on terms for “general licenses” that China pledged to offer for US-bound exports of rare earths and other critical minerals, said the person, who declined to give a reason for the delay.

US (WSJ): Amazon and Microsoft Back Effort That Would Restrict Nvidia’s Exports to China

Amazon.com is joining Microsoft in supporting legislation that threatens to further limit Nvidia’s ability to export to China, a rare split between the chip designer and two of its biggest customers. The moves by Microsoft and Amazon to work against a company they are deeply intertwined with highlights the fierce nature of the artificial-intelligence race. The companies are all jockeying for favorable policy to stay ahead of competitors. Nvidia is fighting for access to the lucrative Chinese market despite security concerns.

ECB (BBG): ECB’s Kazaks Says Rates Appropriate, Willing to Adjust If Needed

European Central Bank Governing Council member Martins Kazaks said the current monetary policy stance is appropriate, according to an interview with Tvnet. “In the euro area as a whole, inflation is close to 2%, so the ECB has fulfilled its task of achieving its long-term inflation target — as we know, our aim is to have inflation at 2% in the medium term,” the Latvian central bank chief was cited as saying. “The information currently available suggests that the current level of interest rates is in line with inflation. If the economic situation changes, we will also change the euro interest rates accordingly.”

CHINA (MNI EXCLUSIVE): PBOC to Increase CGB Purchases, Add Longer Tenors

Chinese economists and traders share their outlook on the PBOC's CGB operations. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI): China CPI Positive Trend But Prices Remain Low - NBS

MNI (Beijing) The 0.2% y/y rise of China's CPI in October reflected a positive trend, Fu Linghui, spokesperson and chief economist at the National Bureau of Statistics, told reporters Friday, but he cautioned that overall prices remain low and demand in the economy is still weak. Looking ahead, authorities plan to promote a moderate price recovery through industrial capacity management, improvements to the market’s competitive environment, and a better balance of supply and demand, Fu added.

CHINA (MNI): China Needs 4.5% GDP Growth in Next Five Years

MNI (Beijing) China aims to leverage the stability of its domestic circulation to offset external uncertainties over the next five years, targeting an economic growth rate of at least 4.5%, Yang Weimin, former vice chairman of the Economic Affairs Committee of the CPPCC National Committee, said Friday at Caixin Summit 2025. Over the next decade, an average annual growth rate of 4.17% will be needed, with total GDP projected to reach CNY175 trillion by 2030, an increase of CNY35 trillion from 2025, Yang said.

CHINA (MNI): PBOC to Boost Yuan Use Despite Challenges Ahead

MNI (Beijing) The People’s Bank of China will promote the cross-border use of the yuan in trade, investment and financing, and provide more products to facilitate foreign investor participation in the stock and bond markets, while improving the payment system and incorporating the currency's use into multilateral and bilateral agreement frameworks, Deputy Governor Tao Ling said Friday at the Caixin Summit 2025.

CHINA (FT): China’s Secretive Gold Purchases Help Fuel Record Rally

China's unreported gold purchases could be more than 10 times its official figures, as the country quietly tries to diversify away from the US dollar, say analysts, highlighting the increasingly opaque sources of demand behind bullion’s record-breaking rally.

RBA (MNI INTERVIEW): Spare Capacity Risks 2026 H2 RBA Hike - Fabo

A former RBA economist shares his cash rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

INDIA (BBG): Modi Coalition Set to Retain Control of India’s Key Bihar State

India’s ruling Bharatiya Janata Party coalition is poised to retain power in key Bihar state, early vote-counting trends showed. The National Democratic Alliance, which includes Prime Minister Narendra Modi’s BJP, is leading in more than 180 seats, according to the Election Commission of India website. The opposition, comprising Indian National Congress, is ahead in more than 50 seats. The majority threshold is 122 in the 243-member legislature. Most exit polls had projected that the ruling party would secure another term.

DATA

EUROZONE FLASH Q3 GDP +0.2% Q/Q, +1.4% Y/Y (MNI)

FRANCE OCT HICP +0.1% M/M, +0.8% Y/Y (MNI)

FRANCE OCT CPI +0.1% M/M, +0.9% Y/Y (MNI)

SPAIN OCT HICP +0.5% M/M, +3.2% Y/Y (MNI)

SWEDEN DATA (MNI): Weak October LFS Data Throws Cold Water on Recent Positive Signals

- SWEDEN OCT SA UNEMPLOYMENT 9.3%

The Swedish October LFS data was weak, tempering the more positive signals from the Public Employment Service's report on Wednesday. The unemployment rate jumped to 9.3%, well above last month's upwardly revised 8.8% and consensus of 8.6%. This was mostly due to an increase in the participation rate to 75.8% (vs 75.5% prior), but employment also fell 0.1% M/M. As always, we caution that the LFS data can be volatile month-to-month. However, 3m rolling trends indicate the unemployment rate is still deviating from the Riksbank's projections. Meanwhile, 3m/3m employment growth was 0.1% (vs -0.2% prior).

CHINA DATA (MNI): Industrial Production Misses Forecasts, Retail Sales Steadies

- CHINA OCT RETAIL SALES +2.9% Y/Y VS MEDIAN +2.8% Y/Y

- CHINA OCT INDUSTRIAL OUTPUT +4.9% Y/Y VS MEDIAN +5.5% Y/Y

Amongst all of the data released today, industrial production were the areas where focus is likely to be. The focus on the consumer and domestic demand is the cornerstone to the next 5-Year plan and whilst it seems that retail sales is becoming less likely to return to the days of +10%, October's result was slightly ahead of market expectations. Expanding +2.9% against forecasts of +2.8%, and below prior month of 3.00%. With the coming data to capture the Single's Days sales, which by all accounts was a success, there may be upside potentials for retail sales and we look back on October's result as being resilient.

CHINA DATA (MNI): China's Investment Dips Further to Over 5-Year Low

- CHINA JAN-OCT FIXED-ASSET INVESTMENT -1.7% Y/Y VS MEDIAN -0.8%

- CHINA YTD PROPERTY INVESTMENT -14.7% Y/Y VS MEDIAN -14.5% Y/Y

MNI (Beijing) China’s fixed-asset investment growth fell further by 1.7% y/y in the first 10 months, expanding from the 0.5% fall in the Jan-Sep period and missing the -0.8% median forecast, also hitting the lowest level since Jun 2020, National Bureau of Statistics data showed Friday. Property investment fell further by 14.7% in the first 10 months, the sharpest drop since Feb 2020, after a 13.9% decline in Jan-Sep. Infrastructure investment fell 0.1% while manufacturing investment grew 2.7%, compared with the previous 1.1% and 4.0% growth.

CHINA OCT UNEMPLOYMENT RATE +5.1% VS SEP +5.2% (MNI)

FOREX: GBP Vol Shows How Sensitive Markets Are to Fiscal Risk

- GBP is comfortably the most active currency in G10 so far Friday, with acute volatility accompanying several mixed stories on UK fiscal risk - reinforcing the link between GBP & Gilt markets to the incoming Budget on November 26th. An overnight report that Chancellor Reeves has scrapped any income tax rate rises triggered a sell-off in UK assets, which had become accustomed to a settled tax plan to shore up fiscal headroom. The resultant GBP weakness (and, to a lesser extent, Gilt weakness) was then briefly reversed as Bloomberg reported the U-turn was due to "improved" OBR forecasts, reducing her need for action on tax-and-spend.

- The recovery rally in GBP was short-lived, however, suggesting markets will remain unsteady and await the details at the end of the month for a more convictive move in either direction. Reeves may plug some of the remaining fiscal hole with income tax threshold changes, but what remains is that the market may be less convinced of Labour's willingness to put UK finances on stable footing now, undermining confidence in GBP.

- From a technical perspective, bullish conditions in EURGBP remain intact and fresh cycle highs reinforce current conditions. A break of 0.8865 would put attention on 0.8893, a Fibonacci projection. For GBPUSD, immediate support stands at 1.3085, the Nov 12 low, a break of which would open up 1.3010, the Nov 4 & 5 low and the bear trigger.

- EURCHF meanwhile has pierced significant support during this morning's volatility, with the 0.9206-0.9211 zone having held prices well just last month, as well as twice last year. As a result, prices hit the lowest levels since the withdrawal of the 1.20 floor in 2015 but have since recovered back above 0.9200. Markets will be closely watching both the formation of the daily candle (as well as the weekly candle) for any evidence prices are trying to find a bottom.

- Markets await any firm schedules for data releases from US statistics agencies after the government reopen following yesterday's BLS announcement they are working to release information "as soon as possible". Canada manufacturing / wholesale sales are on the calendar for today next to ECB's Lane and a set of Fed speakers. Further UK fiscal headlines would also be met with attention.

EGBS: 10-Year Bund Yields Pierce 2.70%, Narrow Gap to FV

10-year Bund yields have pierced the 2.70% figure, a level which contained upside earlier this week. Today’s 2bp rise has narrowed the gap to our rough fair value estimate of around 2.75%. We’ve previously highlighted that a move back towards the 2.80% seen in early September may require increased conviction that the ECB's easing cycle has concluded, alongside durable signs that the ramp-up in German fiscal spending and associated issuance is underway heading into 2026. There has been progress on both these dynamics in recent days.

- The implied probability of another ECB cut this cycle has fallen to 30% (vs ~45% a week ago), and Germany’s 2026 core budget (which was approved by the budget committee yesterday) has pencilled in E8bln more borrowing than assumed in initial drafts.

- Intraday upward pressure in yields has largely been spillover from Gilts and to a lesser extent USTs.

- There has been no safe-haven support for Bunds from the 1% pullback in European equity futures. However, 10-year EGB spreads to Bunds are up to 2.5bps wider, led by the risk-sensitive BTPs.

- With French fiscal developments back in focus this week, note that the French government has announced that the National Assembly will not sit to debate the 2026 budget this weekend, pointing to "fatigue" in the chamber. Parties to the left have deemed the decision to be "unacceptable".

- The German curve has bear steepened, with 5s30s up 2bp to move back above the 100bp figure (which has limited upside since mid-September).

- Bund futures are -22 ticks at 128.70, pushing through prior support at 128.80 and reinforcing the current corrective bearish condition.

- The second reading of Eurozone Q3 GDP confirmed flash estimates of 0.2% Q/Q, while employment growth of 0.1% was in line with the ECB’s projections.

GILTS: Income Tax U-turn Speculation Steepens Curve

Gilts bear steepen vs. yesterday’s close.

- Multiple source reports suggesting that Chancellor Reeves will not deploy income tax hikes drove a sharp sell off at the open (despite some offsetting measures being outlined), as the market became worried that she would not be able to deliver a credible Budget in just under two weeks.

- BBG sources then suggested that the move was facilitated by improved OBR forecasts (with other factors partially offsetting the productivity downgrades), providing a limited relief rally for UK paper.

- Still, the uncertainty triggered by Reeves’ apparent u-turn on income take hikes has dominated when it comes to price action.

- Futures traded as low as 92.07 (breaking the 50-day EMA), before recovering to ~92.60 last, -80 on the day.

- Next support of note located at the September 11 high (91.82).

- Meanwhile, bulls need to retake the 20-day EMA (93.16).

- Yields 4-10bp higher, curve steeper. Fresh November highs registered across the curve.

- At one stage 10-Year yields were on track for the biggest one-day move since July 2. A reminder that the move on July 2 was driven by questions over the UK’s fiscal outlook and the future of Chancellor Reeves after an appearance in the House of Commons.

- SONIA futures 0.25-9.0 lower, off session lows. BoE-dated OIS 1-5bp less dovish; 19bp of easing priced for December, 27bp through February, 37bp through March and 46bp through April.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.780 | -19.0 |

Feb-26 | 3.697 | -27.3 |

Mar-26 | 3.602 | -36.7 |

Apr-26 | 3.505 | -46.4 |

Jun-26 | 3.467 | -50.2 |

Jul-26 | 3.421 | -54.8 |

Sep-26 | 3.407 | -56.2 |

EQUITIES: Thursday's Sell-Off in E-Mini S&P Appears Corrective

A medium-term bull trend in Eurostoxx 50 futures remains intact and this week’s gains reinforce bullish conditions. Note that the sharp pullback Thursday appears to be a correction - for now. A resumption of gains would signal scope for a climb towards 5853.50 next, the top of a bull channel drawn from the Aug 1 low. On the downside, initial firm support is seen at 5676.84, the 20-day EMA. The trend condition in S&P E-Minis remains bullish and Thursday’s selloff appears corrective - for now. Attention is on support at the 50-day EMA, at 6729.38. A clear break of the EMA, and of support at 6655.50, the Nov 7 low, would highlight a short-term reversal and signal scope for a deeper correction. Initial firm resistance to watch is 6900.50, the Nov 12 high. A breach of this hurdle would be a bullish development.

- Japan's NIKKEI closed lower by 905.3 pts or -1.77% at 50376.53 and the TOPIX ended 21.91 pts lower or -0.65% at 3359.81.

- Elsewhere, in China the SHANGHAI closed lower by 39.009 pts or -0.97% at 3990.492 and the HANG SENG ended 500.57 pts lower or -1.85% at 26572.46.

- Across Europe, Germany's DAX trades lower by 199.62 pts or -0.83% at 23843.22, FTSE 100 lower by 116.34 pts or -1.19% at 9690, CAC 40 down 65.25 pts or -0.79% at 8167.24 and Euro Stoxx 50 down 53.18 pts or -0.93% at 5689.61.

- Dow Jones mini down 89 pts or -0.19% at 47460, S&P 500 mini down 23.25 pts or -0.34% at 6737.5, NASDAQ mini down 157.25 pts or -0.63% at 24938.5.

Time: 10:00 GMT

COMMODITIES: Continuation Lower for WTI Could Expose Bear Trigger at $55.96

A sell-off in WTI futures on Tuesday strengthened a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Clearance of this level would confirm a resumption of the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $62.59, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction. Gold is trading closer to this week’s high. The downleg since Oct 20 appears to have been a correction and has allowed an overbought condition to unwind. Recent gains suggest that correction is over. Key support lies at the 50-day EMA, at $3921.1. Clearance of this EMA would signal scope for a deeper retracement. For bulls, a continuation higher would pave the way for a test of $4381.5, the Oct 20 high and bull trigger.

- WTI Crude up $1.15 or +1.96% at $59.76

- Natural Gas down $0.09 or -1.98% at $4.555

- Gold spot down $1.07 or -0.03% at $4169.47

- Copper down $2.9 or -0.57% at $507.3

- Silver up $0.43 or +0.83% at $52.712

- Platinum down $24.65 or -1.55% at $1560.29

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 14/11/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 14/11/2025 | 1330/0830 | ** | Wholesale Trade | |

| 14/11/2025 | 1330/1430 | ECB Elderson Remarks at COP30 Finance Day | ||

| 14/11/2025 | 1500/1000 | * | Business Inventories | |

| 14/11/2025 | 1500/1600 | ECB Lane Panel at Workshop on International Macroeconomics and Finance | ||

| 14/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1930/1430 | Dallas Fed's Lorie Logan | ||

| 14/11/2025 | 2020/1520 | Atlanta Fed's Raphael Bostic | ||

| 15/11/2025 | 1330/1430 | ECB Schnabel Chairs Panel at Econ/FinStab Conference | ||

| 17/11/2025 | 2350/0850 | *** | GDP |