UK FISCAL: Is Income Tax U-Turn Enough To Save Reeves & Starmer? (1/2)

The apparent U-turn from the gov't on planned increases in income tax in the 26 Nov budget, instead the gov't choosing to lower the higher rate income tax threshold (see UK FISCAL: Income tax rates may not be increased, thresholds under consideration,) clearly comes as a sign of the politics of the decision overcoming the economic concerns. It remains to be seen whether such a move will be enough to save the positions of Chancellor of the Exchequer Rachel Reeves and, indeed, embattled PM Sir Keir Starmer.

- For Reeves, the tenability of her position could come down to the market reaction. The fact that Reeves is being forced into apparent late-notice changes to her budget due to political pressure from Labour backbenchers may raise market concerns that she has 'lost control' of the budget. The 'smorgasbord' approach of lots of tax hikes on measures that will each only hit a relatively narrow band of people may raise further market concerns that the gov't is not serious about getting the UK's finances on a more sustainable footing.

- For Starmer, who has endured a torrid 36 hours following anonymous briefings that senior cabinet figures were planning leadership challenges, the U-turn may be a last gamble to try and avoid a major backlash from a restless Parliamentary Labour Party concerned that it is seeing challenges on both the right (from Reform UK) and the left (from a resurgent Green Party) eat into their support.

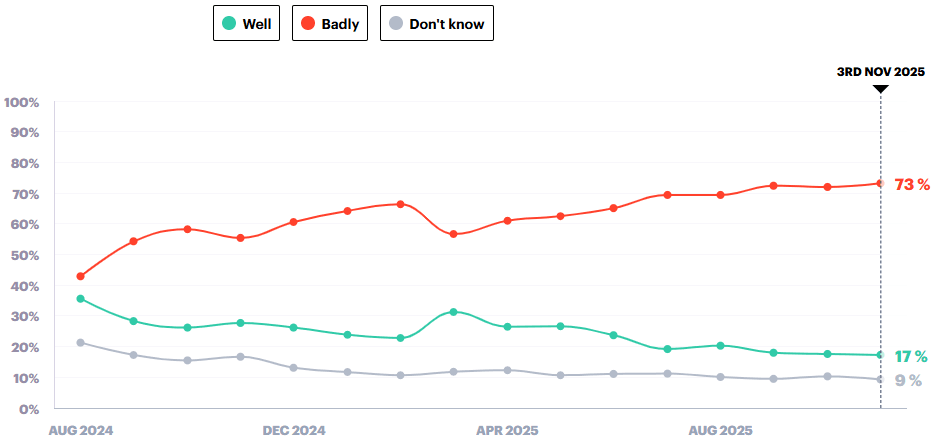

Chart 1. Opinion Poll, 'How Well or Badly Do You Think Keir Starmer Is Doing As PM?', %

Source: YouGov

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: Easing French Political Risks Lends Support To Major EGB Futures

Major EGB futures remain biased to the upside, with yesterday’s easing of near-term French political risks lending support. OAT futures are +32 ticks at 123.01, while Bunds are +17 ticks at 129.85.

- A bull cycle in Bund futures remains intact, with next resistance at 130.05, a Fibonacci retracement point. Note that moving average studies have crossed into a bull-mode position, a bullish signal.

- The German curve is lightly bull flatter, with Schatz yields down 1bp and 10 to 30-year yields down 2bps. 10-year Bund yields are hovering just below the 2.60% figure. A clear break would expose 2.55% as the next downside target.

- Germany will sell E1.0bln of the 0% Aug-50 Bund alongside E1.5bln of the 2.90% Aug-56 Bund this morning,

- 10-year EGB spreads to Bunds are biased up to 1bp wider, with SPGBs and PGBs underperforming.

- Eurozone August industrial production was a little stronger-than-expected at -1.2% M/M (vs -1.6% cons), with last month’s reading also revised up to 0.5% (vs 0.3% initial). There was little market reaction.

- The remainder of today’s regional calendar includes comments from ECB’s Villeroy. He already said yesterday that if the ECB were to move again, a cut is more likely than a hike. This wasn’t surprising, in our view.

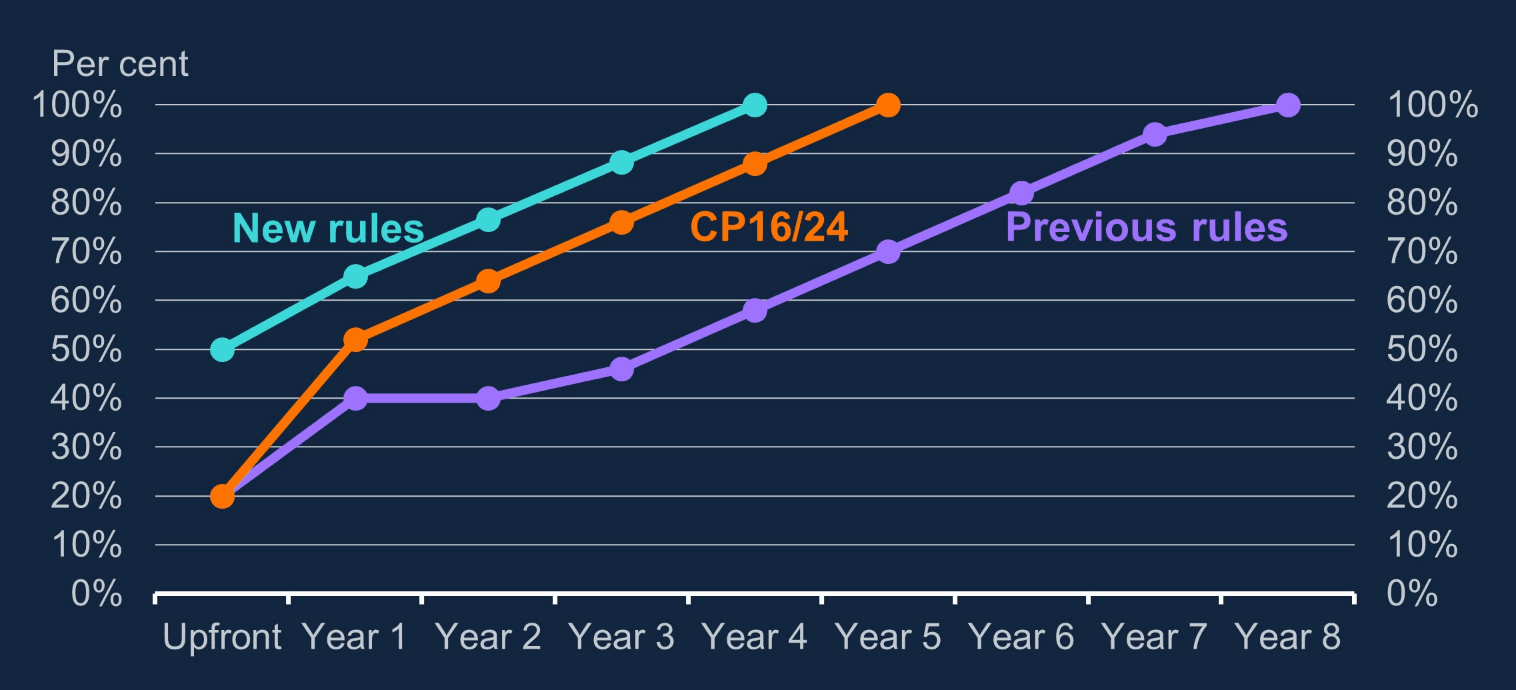

BOE: PRA announces new bonus deferral rules for financial services

- The BOE's PRA has announced new bonus deferral rules for the financial services sector will come into place tomorrow, shortening the required deferral periods.

- Full story here.

- Chart from the BOE on the new deferral rules for bonuses the below. The orange line is the minimum change that was under consultation.

FOREX: Powell Ripple Effect, CNY Fix Drive USD Lower

- The USD Index has stepped lower early Wednesday, prompting USD to fade further off the early October highs. This leaves the USD Index 0.8% off the October highs of 99.563, however still well toward the upper-end of the month's range. The USD is lower for a second session, with European markets taking the lead of the Wall Street close and Powell's appearance just after the close.

- Markets are growing in conviction that an October rate cut is far from the last at the Fed - and Powell's focus on the downside risk for the labour market raises focus for the 10y yield, which is narrowing in on 4.00%. A major break lower here could be the next trigger to extend the USD weaker. In tandem, the stronger-than-expected CNY fix has also proved USD negative. The PBOC set the reference rate at 7.0995, the strongest level in close to twelve months.

- Japanese political uncertainty has failed to keep JPY under pressure, with the currency broadly higher against the rest of G10. Opposition talks are scheduled over the coming days and while betting markets have shifted back in Takaichi's favour. A bullish trend condition in USDJPY remains intact and the pullback from last week’s high appears corrective. The next important support lies at 149.92, the 20-day EMA. On the upside, clearance of 153.27, the Oct 10 high, would resume the uptrend and open 154.39, a Fibonacci retracement point.

- EURUSD has made further progress as markets de-risk after the suspension of France's pension reform yesterday. Increased political stability is outweighing fiscal concerns, but rallies may be contained by potential ratings downgrades on any fiscal slippage. EURUSD printed 1.1645 just after the open, meeting the 100-dma in the process.

- US September CPI was originally set to print today, but with the government shutdown extending further (and looking likely to persist well toward the end of October / early November) it's set to be a quieter session for economic data. Canada's manufacturing sales data, NY Fed's Empire Manufacturing and the latest Beige Book are still due, however.

- This should keep focus on what's already been a busy week of central bank communications. Fed's Miran, Waller & Schmid are due, as well as BoE's Breeden, RBA's Bullock and ECB's Villeroy.