FOREX: GBP Vol Shows How Sensitive Markets are to Fiscal Risk

- GBP is comfortably the most active currency in G10 so far Friday, with acute volatility accompanying several mixed stories on UK fiscal risk - reinforcing the link between GBP & Gilt markets to the incoming Budget on November 26th. An overnight report that Chancellor Reeves has scrapped any income tax rate rises triggered a sell-off in UK assets, which had become accustomed to a settled tax plan to shore up fiscal headroom. The resultant GBP weakness (and, to a lesser extent, Gilt weakness) was then briefly reversed as Bloomberg reported the U-turn was due to "improved" OBR forecasts, reducing her need for action on tax-and-spend.

- The recovery rally in GBP was short-lived, however, suggesting markets will remain unsteady and await the details at the end of the month for a more convictive move in either direction. Reeves may plug some of the remaining fiscal hole with income tax threshold changes, but what remains is that the market may be less convinced of Labour's willingness to put UK finances on stable footing now, undermining confidence in GBP.

- From a technical perspective, bullish conditions in EURGBP remain intact and fresh cycle highs reinforce current conditions. A break of 0.8865 would put attention on 0.8893, a Fibonacci projection. For GBPUSD, immediate support stands at 1.3085, the Nov 12 low, a break of which would open up 1.3010, the Nov 4 & 5 low and the bear trigger.

- EURCHF meanwhile has pierced significant support during this morning's volatility, with the 0.9206-0.9211 zone having held prices well just last month, as well as twice last year. As a result, prices hit the lowest levels since the withdrawal of the 1.20 floor in 2015 but have since recovered back above 0.9200. Markets will be closely watching both the formation of the daily candle (as well as the weekly candle) for any evidence prices are trying to find a bottom.

- Markets await any firm schedules for data releases from US statistics agencies after the government reopen following yesterday's BLS announcement they are working to release information "as soon as possible". Canada manufacturing / wholesale sales are on the calendar for today next to ECB's Lane and a set of Fed speakers. Further UK fiscal headlines would also be met with attention.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Oct14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E537mln), $1.1500(E848mln), $1.1600(E663mln), $1.1650(E636mln)

- USD/JPY: Y151.50($691mln), Y152.00($751mln)

- AUD/USD: $0.6500(A$1.0bln), $0.6580-00(A$1.2bln)

- USD/CAD: C$1.4000-10($598mln)

US 10YR FUTURE TECHS: (Z5) Sights Are On The Bull Trigger

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-29 High Sep 11 and the bull trigger

- RES 1: 113-17+ High Oct 14

- PRICE: 113-14 @ 11:10 BST Oct 15

- SUP 1: 112-26 20-day EMA

- SUP 2: 112-16/01 50-day EMA / 50.0% of Jul 15 - Sep 11 upleg

- SUP 3: 111-26 Low Aug 26

- SUP 4: 111-13+ Low Aug 18 and a key support

Treasuries are holding on to this week’s gains and a bullish theme remains intact. Last Friday’s climb resulted in a break of the 113-00 handle, signalling scope for stronger rally towards 113-29, the Sep 11 high and a bull trigger. Clearance of this hurdle would confirm a resumption of the M/T uptrend. Support at the 50-day EMA at 112-16 remains intact for now. A clear break of the average would expose 111-13+, the Aug 18 low and a key support.

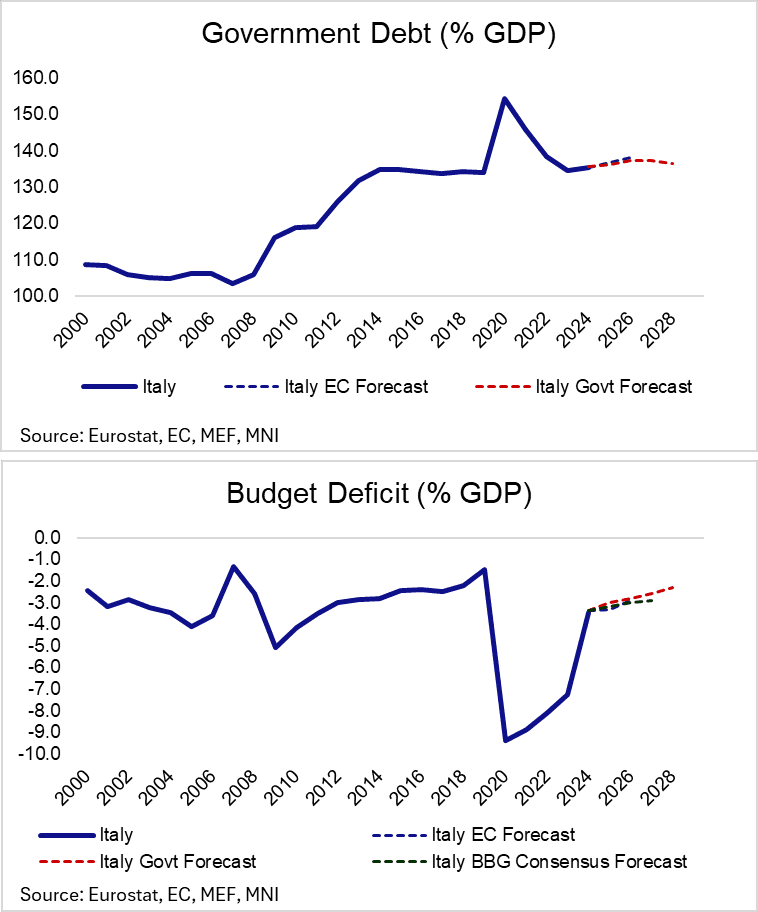

ITALY: 2026 Budget Proposal Sees 2026 Deficit At 2.8%; Growth and Ratings Key

Italy’s 2026 draft budget was approved by the government yesterday. As has been reported in recent weeks, the government expects the budget deficit to fall to 3% GDP in 2025. The deficit is expected to fall to 2.8% in 2026, 2.6% in 2027 and 2.3% in 2028. The 2026 deficit forecast is slightly more optimistic than current Bloomberg consensus of 3.0% and the EC’s Spring Projection round forecast of 2.9% (which of course do not yet account for the policies incorporated into the budget proposal).

- Having already tightened by ~35bps this year, the 10-year BTP/Bund spread has struggled to sustainably consolidated below 80bps in recent months. Upcoming growth data and ratings action will be key in determining whether further near-term narrowing is plausible.

- Growth: Q3 flash GDP is due on October 30. Consensus (according to Bloomberg’s ECFC page) looks for 0.1% Q/Q growth (vs -0.1% prior). We have previously noted that the main barrier to continued Italian fiscal consolidation is the country’s weak growth trajectory.

- Ratings: Moody’s will review Italy’s rating on November 21 (current rating Baa3, Outlook Positive). Moody's rating is two notches below Fitch and S&P, so at least a one notch upgrade is expected. We still think a one notch upgrade to Baa2 while maintaining a positive outlook seems reasonable.

- Some details of the budget proposal via Politico:

- “While ongoing discussions between the government and banks have yet to yield an agreement on what form the tax would take, the hard-right League, of which Giorgetti is a member, is seeking between €4 billion and €4.5 billion from a range of measures, according to two people familiar with the matter. The measures would also apply to insurers, one of the people said”.

- “Major policies in the draft budget, which Italian lawmakers will study in the coming months, includes a €9 billion cut to income taxes for the Italian middle class to 33 percent from 35 percent and €2 billion to align salaries with the cost of living after years of stagnation.

“The draft, which is due to be sent to the European Commission on Wednesday, also earmarks €3.5 billion for “anti-poverty measures” and €2.4 billion for health care in 2026".