MNI US OPEN - Fed's Collin Says Prudent to Ease More in 2025

EXECUTIVE SUMMARY

- FED’S COLLINS SAYS IT’S PRUDENT TO EASE A BIT MORE IN 2025

- TRUMP THREATENS CHINA COOKING OIL AS PAYBACK FOR SOY BOYCOTT

- REEVES SAYS BUDGET MAY INCLUDE BOTH TAX RISES AND SPENDING CUTS

- CHINA CPI AND PPI REMAIN NEGATIVE IN SEPTEMBER, CORE CPI REBOUNDS

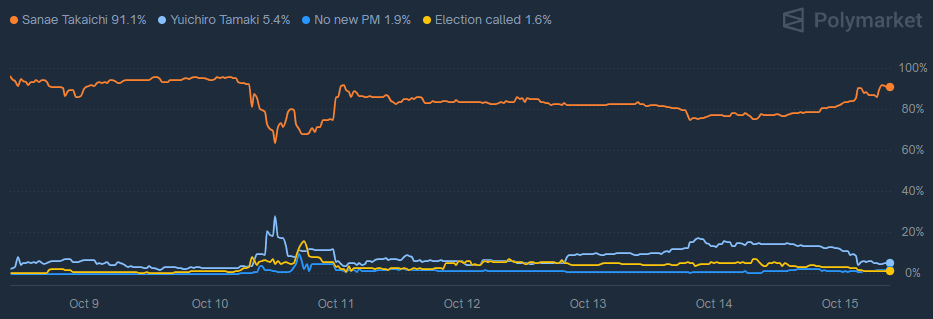

Figure 1: Political Betting Market, Implied Probability of Next Japanese PM, %

Source: Polymarket

NEWS

FED (BBG): Fed’s Collins Says It’s Prudent to Ease a Bit More in 2025

Federal Reserve Bank of Boston President Susan Collins said the US central bank should continue lowering interest rates this year to support the labor market, while keeping them high enough to make sure inflation remains in check. “With inflation risks somewhat more contained, but greater downside risks to employment, it seems prudent to normalize policy a bit further this year to support the labor market,” Collins said Tuesday in remarks prepared for an event at the Boston Fed.

US/CHINA (BBG): Trump Threatens China Cooking Oil as Payback for Soy Boycott

US President Donald Trump said he might stop trade in cooking oil with China, injecting fresh tensions into the relationship between the world’s two largest economies. Trump on Tuesday cast the potential move as retaliation against Beijing for its refusal to buy American soybeans, which he said “is an Economically Hostile Act” that is purposefully “causing difficulty for our Soybean Farmers.” China remains well supplied with the oilseed, largely thanks to South American purchases.

US/CHINA (BBG): Apple’s Cook Vows to Boost Chinese Investment During Visit

Apple Inc. Chief Executive Officer Tim Cook pledged to boost investment in China during a visit to the world’s second largest economy, despite threats from US President Donald Trump to slap tariffs on its foreign-made products. Cook met Chinese Minister of Industry and Information Technology Li Lecheng on Wednesday, the agency said in a post on its official WeChat account. Li urged Apple to work closely with local suppliers, while Cook said Apple will boost cooperation with China.

US/CHINA (WSJ): China, Betting It Can Win a Trade War, Is Playing Hardball With Trump

In its trade standoff with Washington, Beijing thinks it has found America’s Achilles’ heel: President Trump’s fixation on the stock market. China’s leader, Xi Jinping, is betting that the U.S. economy can’t absorb a prolonged trade conflict with the world’s second-largest economy, according to people close to Beijing’s decision-making. China is holding a firm line because of its conviction, the people said, that an escalating trade war will tank markets, as it did in April after Trump announced his so-called Liberation Day tariffs, prompting Beijing to hit back.

US/MIDEAST (BBG): Trump Threatens Hamas Over Disarmament as Hostage Deal Hits Snag

US President Donald Trump demanded that Hamas return the bodies of deceased hostages and threatened the militant group with retaliation if it does not lay down its arms. “If they don’t disarm, we will disarm them. They know I’m not playing games,” Trump told reporters at the White House during a meeting with Argentina’s president.

ECB (BBG): ECB’s Makhlouf Says Inflation Above 2% Is Bigger Risk Than Below

European Central Bank Governing Council member Gabriel Makhlouf dismissed concerns about inflation dropping below the 2% target, saying he’s actually more worried that it will come in above that threshold. While the Frankfurt-based central bank projects a temporary undershoot next year, Makhlouf said this isn’t a problem as long as the medium-term outlook remains anchored around 2%. Food inflation — which has been trending higher this year and is now around 3% — is an area to pay particular attention to, he said in an interview.

UK (The Times): Rachel Reeves: Budget May Include Both Tax Rises and Spending Cuts

Rachel Reeves has admitted for the first time she will need to consider both tax rises and spending cuts in her November budget as she attempts to fill a financial “black hole” of up to £30 billion. The chancellor told Sky News that “of course we’re looking at tax and spending as well” after she was asked how she would deal with Britain’s economic woes. It is the first time Reeves has acknowledged that tax rises are being considered.

UK (FT): Rachel Reeves Revives Plans to Overhaul Cash Isas

Chancellor Rachel Reeves is looking to use her Budget to revive plans for a major overhaul of tax-free Isas to divert tens of billions of pounds of savings from cash into domestic stocks, as she tries to import a US-style investment culture to Britain. But Reeves knows that lowering the tax-free limit for cash ISAs — possibly halving it from £20,000 to £10,000 per year — will provoke a fierce backlash from building societies and wants British business to help her make the case for the changes.

NORWAY (MNI): Key Figures From 2026 Budget Proposal

With the fiscal stance in line with Norges Bank expectations and having an approximately neutral impact on mainland GDP, the market reaction is limited. Structural non-oil deficit spending in NOK (current prices): NOK579.4bln vs NOK534.2bln in 2025. A little above the ~NOK570-573bln estimates we saw from JP Morgan and DNB. "This includes continued support to Ukraine amounting to NOK 85 billion." Structural non-oil deficit spending as a % of Government pension fund assets (fiscal rule stipulates maximum spending of 3% of the GPFG): 2.8% vs 2.7% in 2025.

NATO (MNI): Def Mins Meet for Ukraine Talks w/Focus on Tomahawks & Air Defences

NATO defence ministers are meeting at the alliance's HQ in Brussels. Speaking on 14 Oct, US President Donald Trump raised again the potential sale of Tomahawk missiles, which could strike deep into Russia, to Kyiv. Trump hosts President Volodymyr Zelenskyy at the White House on 17 Oct, claiming "He would like to have Tomahawks...We have a lot of Tomahawks." Russian President Vladimir Putin said the sale of Tomahawks, capable of carrying a nuclear warhead and capable of reaching Moscow, would mark a "qualitatively new stage of escalation."

CHINA (BBG): China Boosts Yuan Support Via Fixing as Trade Headwinds Grow

China ramped up its support for the yuan on Wednesday, underscoring its commitment to foreign-exchange stability as a trade war with the US showed few signs of letting up. The People’s Bank of China set the yuan’s reference rate at 7.0995 per dollar, the strongest level in almost a year and past the 7.1 mark that authorities had sought to defend since September. The move helped boost the offshore yuan while weighing on the dollar.

JAPAN (MNI): DPFP Chief - LDP's Takaichi Proposed Coalition, More Talks 20 Oct

Japanese politics remains in a state of uncertainty, with opposition parties holding the balance of power on whether to back the governing Liberal Democratic Party (LDP)'s new president, Sanae Takaichi, to succeed Shigeru Ishiba, or to pursue a three-party alliance to nominate an opposition figure. Takaichi has held in-person meetings with all three main party leaders today, with the opposition leaders also holding their own talks. Conservative populist Democratic Party for the People (DPFP) leader Yuichiro Tamaki says that there is "still some distance" between his party and the main opposition liberal Constitutional Democratic Party (CDP).

RBA (MNI): RBA's Hunter Sees Stronger Q3 Inflation

Reserve Bank of Australia Assistant Governor Sarah Hunter said third-quarter inflation is likely to come in stronger than anticipated in the August forecasts, while labour market and economic conditions appear tighter than expected. Speaking at an industry conference, Hunter said the Bank is “actively analysing this question ahead of our next set of forecasts, which will be released in November.”

RBNZ (MNI): RBNZ's Conway Nervous CPI Elevated But Further Easing Possible

RBNZ Chief Economist Conway revealed in a Bloomberg interview that the October 50bp rate cut decision was "finely balanced" and that it was a response to the sharp Q2 GDP contraction, which shifted the "balance of risks" towards less inflation pressures, and then was set by the soft Q3 QSBO survey. He reiterated that the MPC is open to further easing dependent on the data.

INDIA (BBG): RBI Sees Rupee Under Speculative Attack, Will Intervene Further

India’s central bank considers recent weakness in the rupee as driven by speculative attacks and is prepared to continue its market intervention until the currency settles at a stronger level, a person familiar with the matter said. The RBI was alarmed to see the rupee nearing the 89 a dollar level in recent trading sessions, the person said, asking not to be identified to discuss internal matters. The central bank is unwilling to let the currency breach its record low of 88.8050 a dollar level anytime soon, the person said.

ARGENTINA (BBG): Argentina Says US Treasury Will Continue to Support Peso

Economy Minister Luis Caputo said the US remains committed to a $20 billion currency-swap line with Argentina, regardless of the outcome of midterm elections in the South American nation later this month. The US Treasury is still finalizing details of the swap line, but a decision to make it available to Argentina has already been made, Caputo told reporters in Washington, adding that the US administration will continue to support the peso as needed.

DATA

FRANCE SEP CPI -1.0% M/M, +1.2% Y/Y (MNI)

FRANCE SEP HICP -1.1% M/M, +1.1% Y/Y (MNI)

SWEDEN DATA (MNI): CPIF Ex-energy Confirms Flash; Food and Goods Drive Pullback

- SWEDEN FINAL SEP CPIF +3.1% Y/Y

- SWEDEN FINAL SEP CPIF EX-ENERGY +2.7% Y/Y

Swedish September inflation confirmed flash estimates, leaving CPIF ex-energy in line with the Riksbank's September MPR projection at 2.70% Y/Y (vs 2.92% prior). The signal for monetary policy is neutral - we don't expect a move away from 1.75% for at least the next few months. Our estimate of seasonally adjusted CPIF ex-energy inflation for September was 0.05% M/M for the second consecutive month. That pulled 3m/3m annualised inflation momentum down to a 13-month low of 2.12%.

CHINA DATA (MNI): China's Sep CPI, PPI Fall Narrow, Core CPI Rebounds

- CHINA SEP CPI -0.3% Y/Y VS MEDIAN -0.2%; AUG -0.4%: NBS

China’s Consumer Price Index fell 0.3% y/y in September, narrowing from August's 0.4% fall but missing expectations for a 0.2% drop, mainly due to the lower comparison base for the same period last year, according to data from the National Bureau of Statistics released Wednesday. On a monthly basis, CPI rose 0.1%, edging up from August's 0.0% growth. Core CPI, which excludes food and energy, rose 1.0% y/y for the first time in 19 months, expanding for the fifth consecutive month from August's 0.9% rise.

CHINA JAN-SEP NEW LOANS CNY14.75 TRLN VS MEDIAN CNY14.92 TRLN (MNI)

CHINA JAN-SEP TSF CNY30.09 TRLN VS MEDIAN CNY29.90 TRLN (MNI)

CHINA END-SEP M2 +8.4% Y/Y VS MEDIAN +8.5%; END-AUG +8.8% Y/Y (MNI)

AUSTRALIA DATA (MNI): Westpac Lead Indicator Signals Around Trend Growth

The Westpac lead index fell 0.03% m/m in September bringing the 6-month annualised rate to +0.04% from -0.16%. It has oscillated around zero over the last 5 months. This measure leads detrended growth by 3 to 9 months and signals that growth may slow in H2 but be around trend early in 2026. Westpac is forecasting 2% growth in 2025 with it improving in 2026.

FOREX: Powell Ripple Effect, CNY Fix Drive USD Lower

- The USD Index has stepped lower early Wednesday, prompting USD to fade further off the early October highs. This leaves the USD Index 0.8% off the October highs of 99.563, however still well toward the upper-end of the month's range. The USD is lower for a second session, with European markets taking the lead of the Wall Street close and Powell's appearance just after the close.

- Markets are growing in conviction that an October rate cut is far from the last at the Fed - and Powell's focus on the downside risk for the labour market raises focus for the 10y yield, which is narrowing in on 4.00%. A major break lower here could be the next trigger to extend the USD weaker. In tandem, the stronger-than-expected CNY fix has also proved USD negative. The PBOC set the reference rate at 7.0995, the strongest level in close to twelve months.

- Japanese political uncertainty has failed to keep JPY under pressure, with the currency broadly higher against the rest of G10. Opposition talks are scheduled over the coming days and while betting markets have shifted back in Takaichi's favour. A bullish trend condition in USDJPY remains intact and the pullback from last week’s high appears corrective. The next important support lies at 149.92, the 20-day EMA. On the upside, clearance of 153.27, the Oct 10 high, would resume the uptrend and open 154.39, a Fibonacci retracement point.

- EURUSD has made further progress as markets de-risk after the suspension of France's pension reform yesterday. Increased political stability is outweighing fiscal concerns, but rallies may be contained by potential ratings downgrades on any fiscal slippage. EURUSD printed 1.1645 just after the open, meeting the 100-dma in the process.

- US September CPI was originally set to print today, but with the government shutdown extending further (and looking likely to persist well toward the end of October / early November) it's set to be a quieter session for economic data. Canada's manufacturing sales data, NY Fed's Empire Manufacturing and the latest Beige Book are still due, however.

- This should keep focus on what's already been a busy week of central bank communications. Fed's Miran, Waller & Schmid are due, as well as BoE's Breeden, RBA's Bullock and ECB's Villeroy.

EGBS: Easing French Political Risks Lends Support to Major EGB Futures

Major EGB futures remain biased to the upside, with yesterday’s easing of near-term French political risks lending support. OAT futures are +32 ticks at 123.01, while Bunds are +17 ticks at 129.85.

- A bull cycle in Bund futures remains intact, with next resistance at 130.05, a Fibonacci retracement point. Note that moving average studies have crossed into a bull-mode position, a bullish signal.

- The German curve is lightly bull flatter, with Schatz yields down 1bp and 10 to 30-year yields down 2bps. 10-year Bund yields are hovering just below the 2.60% figure. A clear break would expose 2.55% as the next downside target.

- Germany will sell E1.0bln of the 0% Aug-50 Bund alongside E1.5bln of the 2.90% Aug-56 Bund this morning,

- 10-year EGB spreads to Bunds are biased up to 1bp wider, with SPGBs and PGBs underperforming.

- Eurozone August industrial production was a little stronger-than-expected at -1.2% M/M (vs -1.6% cons), with last month’s reading also revised up to 0.5% (vs 0.3% initial). There was little market reaction.

- The remainder of today’s regional calendar includes comments from ECB’s Villeroy. He already said yesterday that if the ECB were to move again, a cut is more likely than a hike. This wasn’t surprising, in our view.

GILTS: Firmer on Global Cues

Gilts have rallied, largely on spillover from wider core global FI markets.

- The reduction of short-term French political risks and late Tuesday comments from Fed Chair Powell (pointing to further rate cuts and the potential for the end of QT in the coming months) have provided the support.

- Gilts outperform swaps following Powell’s comments.

- Futures trade as high 92.41 before fading to 92.27 last.

- Fresh extension higher would target projection resistance (92.72).

- Yields 3-4bp lower across the curve, wings underperform.

- 10s pierced support at the August 11 low (4.548%). Uptrend support drawn from the Dec ’24 low was also tested (4.536%). The next level of note below there is the August low (4.496%), which equates to 92.73 in futures today.

- 30s have broken through uptrend support drawn off the April low (5.370%) and trade ~5bp above their August low (5.309%).

- This morning’s I/L supply saw a solid cover ratio (~3.5x), but pricing was on the soft side.

- The rally further out the curve has allowed yesterday’s dovish move in GBP STIRs to extend.

- SONIA futures flat to +3.0.

- BoE-dated OIS pricing ~10bp of easing through year-end.

- BoE’s Ramsden didn’t touch on monetary policy in his morning address.

- Fellow Deputy Governor Breeden is unlikely to cover monetary policy when she speaks later.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.944 | -2.4 |

Dec-25 | 3.870 | -9.7 |

Feb-26 | 3.733 | -23.4 |

Mar-26 | 3.690 | -27.8 |

Apr-26 | 3.590 | -37.8 |

Jun-26 | 3.558 | -40.9 |

Jul-26 | 3.500 | -46.7 |

Sep-26 | 3.484 | -48.3 |

EQUITIES: Eurostoxx 50 Futures Remain Above Key Support Zone

The trend condition in Eurostoxx 50 futures is unchanged, the direction is up and the latest pullback appears to have been a correction. A key support zone between 5553.01 - 5481.41, the area between the 20- and 50-day EMAs, remains intact. A clear break of the 50-day average would highlight a stronger reversal. On the upside, the bull trigger is 5689.00, the Oct 2 high. Clearance of this hurdle would confirm a resumption of the uptrend. A sharp sell-off in S&P E-Minis last Friday appears corrective - for now. The contract has found support below the 50-day EMA, currently at 6605.62, and the Oct 10 low of 6540.25 has been defined as a key short-term support. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high. A breach of this hurdle would confirm a resumption of the uptrend.

- Japan's NIKKEI closed higher by 825.35 pts or +1.76% at 47672.67 and the TOPIX ended 49.65 pts higher or +1.58% at 3183.64.

- Elsewhere, in China the SHANGHAI closed higher by 46.98 pts or +1.22% at 3912.209 and the HANG SENG ended 469.25 pts higher or +1.84% at 25910.6.

- Across Europe, Germany's DAX trades higher by 42.58 pts or +0.18% at 24276.34, FTSE 100 lower by 30.15 pts or -0.32% at 9422.39, CAC 40 up 195.92 pts or +2.47% at 8115.54 and Euro Stoxx 50 up 76.23 pts or +1.37% at 5628.28.

- Dow Jones mini up 126 pts or +0.27% at 46626, S&P 500 mini up 29 pts or +0.43% at 6715.5, NASDAQ mini up 155.75 pts or +0.63% at 24918.25.

Time: 10:00 BST

COMMODITIES: Gold Pierces $4200 Round Number Resistance

A bearish theme in WTI futures remains intact and Tuesday’s fresh cycle low reinforces current conditions. The move down last week resulted in a break of support at $60.40, the Oct 2 low. This highlights an extension of the bearish price sequence of lower lows and lower highs and the move down opens $57.50 next, the May 30 low. On the upside, key resistance is at $66.42, the Sep 26 high. First resistance is at $62.47, the 50-day EMA. A bull cycle in Gold remains intact and this week’s extension reinforces current conditions. The move higher maintains the price sequence of higher highs and higher lows. Sights are on the $4200.00 handle, and $4239.7, a Fibonacci projection point. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support lies at $3889.3, 20-day EMA.

- WTI Crude down $0.09 or -0.15% at $58.61

- Natural Gas down $0.01 or -0.46% at $3.014

- Gold spot up $65.72 or +1.59% at $4211.15

- Copper up $1.6 or +0.32% at $504.15

- Silver up $1.58 or +3.07% at $53.0244

- Platinum up $24.18 or +1.48% at $1659.3

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 15/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 15/10/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/10/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/10/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/10/2025 | 1330/0930 | Fed Governor Stephen Miran | ||

| 15/10/2025 | 1545/1645 | BOE Breeden in Panel on Financial Regulation | ||

| 15/10/2025 | 1610/1210 | Atlanta Fed's Raphael Bostic | ||

| 15/10/2025 | 1630/1230 | Fed Governor Stephen Miran | ||

| 15/10/2025 | 1700/1300 | Fed Governor Christopher Waller | ||

| 15/10/2025 | 1735/1335 | Kansas City Fed's Jeff Schmid | ||

| 15/10/2025 | 1800/1400 | Fed Beige Book | ||

| 15/10/2025 | 1800/2000 | ECB de Guindos at Alantra Anniversary Event | ||

| 15/10/2025 | 1800/1900 | BOE Breeden in Panel at Fintech Foundation | ||

| 16/10/2025 | 2350/0850 | * | Machinery orders | |

| 16/10/2025 | 0030/1130 | *** | Labor Force Survey | |

| 16/10/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 16/10/2025 | 0600/0700 | ** | Trade Balance | |

| 16/10/2025 | 0600/0700 | ** | Index of Services | |

| 16/10/2025 | 0600/0700 | ** | Index of Production | |

| 16/10/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 16/10/2025 | 0800/1000 | *** | HICP (f) | |

| 16/10/2025 | 0830/0930 | BOE Credit Conditions Survey | ||

| 16/10/2025 | 0900/1100 | * | Trade Balance | |

| 16/10/2025 | 0900/0500 | * | CREA Existing Home Sales | |

| 16/10/2025 | 0900/1100 | Foreign Trade | ||

| 16/10/2025 | 1200/0800 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 16/10/2025 | 1230/0830 | *** | Retail Sales | |

| 16/10/2025 | 1230/0830 | *** | PPI | |

| 16/10/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 16/10/2025 | 1230/0830 | *** | Retail Sales | |

| 16/10/2025 | 1300/1400 | BOE Mann in Panel on MonPol and Trade Shocks | ||

| 16/10/2025 | 1300/0900 | Fed Governor Christopher Waller | ||

| 16/10/2025 | 1300/0900 | Fed Governor Michael Barr | ||

| 16/10/2025 | 1300/0900 | Fed Governor Stephen Miran | ||

| 16/10/2025 | 1400/1000 | * | Business Inventories | |

| 16/10/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/10/2025 | 1400/1000 | * | Business Inventories | |

| 16/10/2025 | 1400/1000 | Fed Governor Michelle Bowman | ||

| 16/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 16/10/2025 | 1445/1545 | BOE Mann in MonPol Panel at IMF/World Bank Meetings | ||

| 16/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 16/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 16/10/2025 | 1545/1745 | ECB Lane in Policy Panel at IIF Annual Meeting | ||

| 16/10/2025 | 1600/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 16/10/2025 | 1600/1200 | ** | US DOE Petroleum Supply | |

| 16/10/2025 | 1600/1800 | ECB Lagarde in IMF Policy Debate | ||

| 16/10/2025 | 1645/1245 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 1730/1330 | BOC Governor Macklem speaks at Peterson Institute event in Washington. | ||

| 16/10/2025 | 1830/1930 | BOE Greene in Panel on UK/EU Relations | ||

| 16/10/2025 | 2015/1615 | Fed Governor Stephen Miran | ||

| 16/10/2025 | 2030/1630 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 2200/1800 | Minneapolis Fed's Neel Kashkari |