SWEDEN: CPIF ex-energy Confirms Flash; Food and Goods Drive Pullback

Swedish September inflation confirmed flash estimates, leaving CPIF ex-energy in line with the Riksbank’s September MPR projection at 2.70% Y/Y (vs 2.92% prior). The signal for monetary policy is neutral – we don’t expect a move away from 1.75% for at least the next few months.

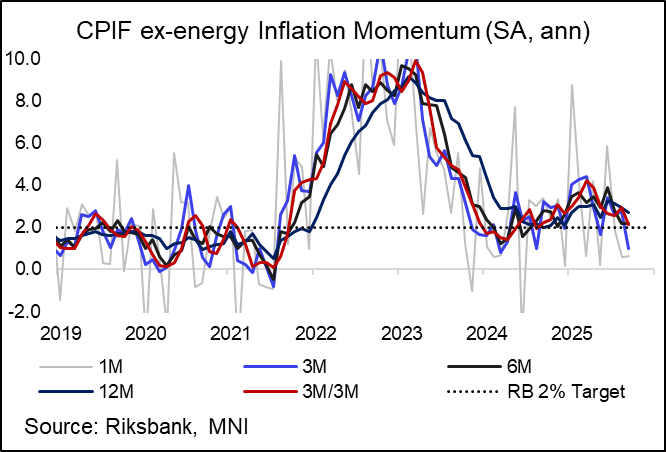

- Our estimate of seasonally adjusted CPIF ex-energy inflation for September was 0.05% M/M for the second consecutive month. That pulled 3m/3m annualised inflation momentum down to a 13-month low of 2.12%.

- There was another sharp pullback in food inflation in September, to 2.66% Y/Y (vs 3.94% in August, 4.26% in June and July). This was the lowest annual rate since January.

- Meanwhile, goods inflation pressures appear soft:

- Clothing eased to 2.02% Y/Y (vs 2.95% prior) while footwear pulled back to 0.61% Y/Y (vs 4.66% prior). Monthly price developments were well below September 2024 and the 2010-2019 average for September.

- Furnishings and household equipment inflation was also soft at -2.31% Y/Y (vs -0.41% prior).

- Vehicle inflation was -0.05% Y/Y (vs 0.38% prior).

- These trends were somewhat offset by stronger annual services inflation, but we caveat that familiar volatile categories were at play:

- Car rental and international flight prices saw sequential declines for the second consecutive month (further unwinding summer strength), but Y/Y rates still accelerated relative to August.

- Meanwhile, package holidays reversed a little of August’s -22.5% M/M fall with a 3.1% rise. The annual rate became less negative at -0.49% Y/Y (vs -5.56% in August) as a result.

- Accommodation services rose 5.26% M/M, compared to a -0.62% M/M fall in September 2024. That pushed the annual rate up to 6.13% Y/Y (vs 0.2% prior).

- The proportion of subcomponents with annual inflation rates below 3% rose to 65% in September, up from 60% in August.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US-CHINA: Bessent And He Meet For Second Day Of Trade Talks In Madrid

MNI London: Treasury Secretary Scott Bessent told reporters the US is “not willing to sacrifice national security,” in pursuit of a trade deal with China, ahead of a second day of talks with Chinese Vice Premier He Lifeng in Spain, per Reuters.

- Reuters reports six hours of talks yesterday concluded with “no indication of a breakthrough” in trade or the Sept. 17 deadline for Chinese TikTok divestment. Bessent said the two sides are “very close” to a TikTok resolution but stressed, “it does not affect overall relationship with China.”

- Bessent is due in London on Tuesday for a meeting with UK Chancellor Rachel Reeves ahead of Trump’s UK state visit. Reuters notes, “China's embassy in Madrid notified reporters of a potential concluding news conference on Monday afternoon, indicating that the talks could wrap up quickly.”

- One outcome today could be an agreement on a meeting between Trump and Chinese President Xi Jinping ahead of the Oct. 31 APEC forum in South Korea. FT reports that White House hasn't yet responded to an invitation for Trump to visit China as the countries "are still far apart on trade issues and the flow of fentanyl.” Meanwhile, Beijing continues to push for further easing of US export controls on chips and high-tech.

- Without a positive outcome today, a Trump-Xi meeting could be scaled back from a bilateral in Beijing to a lower-profile meeting at APEC. The prospects of a bilateral may also be reduced by Trump’s message to NATO on Saturday, calling for 50%-100% tariffs on China as a prerequisite for new US sanctions on Russia.

GILTS: Friday's Low In Futures Holds

Gilt futures test Friday’s low (91.14) with the contract then recovering to 91.30, aided by an uptick in both Tsys and Bunds.

- The recent bullish cycle in the contract remains intact, with support and resistance of note located at 90.65 & 91.82.

- Yields 1-2bp lower, curve bull steepens after last week’s flattening left 2s10s and 5s30s 13bp & 11bp off their respective September closing highs.

- SONIA futures +1.0 to -1.0.

- BoE-dated OIS continues to price ~8bp of easing through year-end.

- As we have noted already, Tuesday will see labour market data released, while Wednesday will bring inflation data, with both coming ahead of Thursday’s BoE MPC decision.

- With expectations for Bank Rate to be left unchanged, the BoE’s QT decision is set to dominate when it comes to the latter.

- From the 17 sell-side previews that we have read the median expectation is for a GBP70bln annual reduction (~GBP69bln). This would be a smaller total APF reduction than the GBP100bln seen in the 24/25 year but would imply active sales of around GBP20-21bln, vs. GBP13bln in the 24/25 year (due to smaller redemptions in the upcoming year).

- There is plenty of uncertainty around this and given that the size of the balance sheet is to approach the top of the PMRR range through passive reduction alone, we would argue that either active sales continuing at their current pace or being suspended completely would be the optimal position for the market.

- Analysts are split on whether there will be a skew away from long-dated gilts being sold.

EQUITIES: Option expiries in Notional term

Looking ahead at Triple Witching Friday, Option expiries in Notional terms:

US:

- SPX: $2.73T.

- NDX: $107.39bn.

- Amazon: $17.57bn.

- Apple: $20.65bn.

EU:

- SX5E: €198.35bn.

- SX7E: €18.69bn.

- DAX: €40.20bn.

- FTSE: £21.25bn.

- Lloyds: £5.38bn.