RBNZ: RBNZ’s Conway Nervous CPI Elevated But Further Easing Possible

Oct-15 01:25

RBNZ Chief Economist Conway revealed in a Bloomberg interview that the October 50bp rate cut decision was “finely balanced” and that it was a response to the sharp Q2 GDP contraction, which shifted the “balance of risks” towards less inflation pressures, and then was set by the soft Q3 QSBO survey. He reiterated that the MPC is open to further easing dependent on the data. While inflation is expected to moderate to 2% in 2026, Conway said it was “nerve-racking” that it was close to the top of the band. Q3 CPI prints on 20 October.

- Growth is still expected to improve over H2 2025 and into 2026. While the factors driving inflation to the top of the band are expected to fade.

- Conway would accept attributed votes but said that it will be up to the new governor who starts on 1 December.

- TD Securities now expects the RBNZ to cut the OCR 25bp to 2.25% in November, according to Dow Jones.

- Given the importance of the QSBO survey to the last decision, it is worth noting that the September BNZ services and manufacturing PMIs were consistent with the RBNZ’s assessment in the October statement that “economic activity recovered modestly in the September quarter”.

- Key data before the 26 November RBNZ decision include Q3 CPI on 20 October, Q3 jobs/wages 5 November, Q4 inflation expectations 11 November, October ANZ business confidence 31 October, October card spending 13 November (Sept fell), October BNZ PMI & PSI 14 & 17 November, and October prices 17 November.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

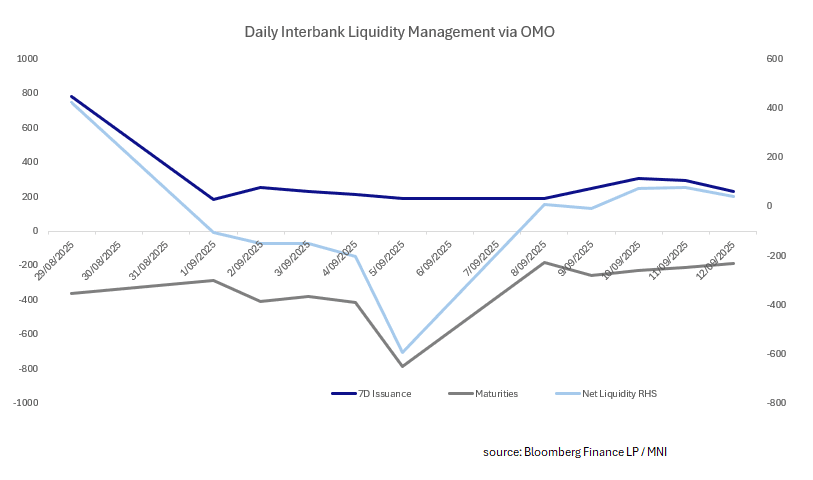

CHINA: Central Bank Injects CNY88.5bn via OMO

Sep-15 01:23

- The PBOC issued CNY280bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY191.5bn.

- Net liquidity injects CNY88.5bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.42%, from prior close of 1.45%.

- The China overnight interbank repo rate is at 1.40%, from the prior close of 1.41%.

- The China 7-day interbank repo rate is at 1.50%, from the prior close of 1.45%.

MNI: CHINA PBOC CONDUCTS CNY280 BLN VIA 7-DAY REVERSE REPO MON

Sep-15 01:21

- CHINA PBOC CONDUCTS CNY280 BLN VIA 7-DAY REVERSE REPO MON

CHINA SETS YUAN CENTRAL PARITY AT 7.1056 MON VS 7.1019

Sep-15 01:19

- CHINA SETS YUAN CENTRAL PARITY AT 7.1056 MON VS 7.1019