U.S. President Donald Trump said Tuesday he will pick a new Federal Reserve governor by the end of the week and again named National Economic Council Director Kevin Hassett and former Fed Governor Kevin Warsh as contenders to be the next Fed leader.

ECB (BBG): ECB’s Holzmann Sees No Reason To Cut Rates Again, Ooen Reports

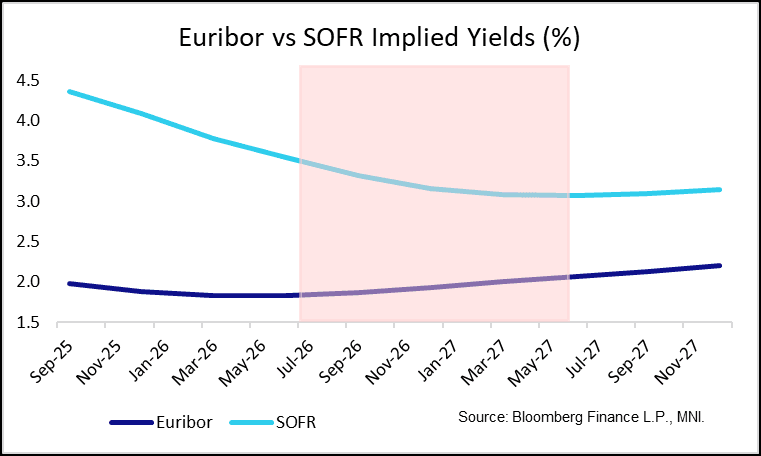

European Central Bank shouldn’t lower borrowing costs again, outgoing Governing Council member Robert Holzmann told Oberösterreichische Nachrichten.

GERMANY (BBG): Germany Readies €100 Billion Fund to Invest in Strategic Assets

Germany is preparing to launch a €100 billion ($116 billion) investment fund to help secure strategic sectors such as defense, energy and critical raw materials.

UK (BBC): Reeves Must Raise Tax To Cover £41bn Gap, Says Think Tank

Taxes must rise in the autumn if Chancellor Rachel Reeves is to meet her self-imposed borrowing rules, according to an economic think tank.

BOJ (BBG): Japan LDP’s Kono Adds to Chorus Urging BOJ to Tighten Policy

A member of parliament in the Liberal Democratic Party added his voice to those calling for the Bank of Japan to tighten monetary policy in order to bolster the yen.

BOJ (RTRS): Japan Ruling Party Heavyweight Warns Against BOJ Rate Hike

The Bank of Japan must be cautious about raising interest rates given the expected hit from U.S. tariffs on the fragile economy, ruling party heavyweight Ken Saito told Reuters.

RBA (MNI): Further RBA Cuts Risk Policy Mistake - McKibbin

An ex-RBA board member warns against over easing -- on MNI Policy MainWire now, for more details please contact sales@marketnews.com.

SOUTH KOREA (Chosun): Koo Yoon-Cheol Outlines Tariff Negotiations With U.S. While Promoting Domestic Production

Deputy Prime Minister and Minister of Economy and Finance Ku Yoon-chul said on the 6th that he has "avoided the worst-case scenario" regarding tariff negotiations with the United States, while stating his position on the introduction of tax incentives for domestic manufacturing and the possibility of additional opening of agricultural markets.

RUSSIA (RTRS): Trump's Envoy Witkoff Lands In Moscow On Last-Minute Trip Before Sanctions Deadline

U.S. envoy Steve Witkoff arrived in Moscow on Wednesday on a last-minute mission to seek a breakthrough in the Ukraine war, two days before the expiry of a deadline set by President Donald Trump for Russia to agree to peace or face new sanctions.

CANADA (CBC): Carney Hints At Dropping Some U.S. Tariffs If It Will Help Canadian Industries Hit By Trade War

Prime Minister Mark Carney showed no signs of retaliating against U.S. President Donald Trump's increased tariffs — and even suggested he's open to removing existing tariffs if it would help Canadian industries.

CANADA/MEXICO (RTRS):Canadian Minister Hails 'Productive' Mexico Meeting As U.S. Tariffs Loom

Top Canadian ministers held a "productive" meeting with Mexican President Claudia Sheinbaum and some of her top officials during a visit to Mexico City on Tuesday, Canada's top diplomat said, as the two nations navigate a volatile tariff environment.

The Reserve Bank of India (RBI) Wednesday maintained policy interest rates citing ongoing transmission of its recent actions and global trade uncertainties. The central bank also kept the monetary stance at 'neutral', citing a likely increase in consumer inflation and macroeconomic uncertainties.

TURKEY (RTRS): Turkey's Simsek Says Determined To Maintain Lasting Disinflation Process

Turkey's disinflation process is continuing in a determined manner that will bring inflation into single digits in two years, Treasury and Finance Minister Mehmet Simsek told Reuters, adding the government would not allow the process to be derailed.

CHILE (BBG): Chile Central Bank to Buy up To $25M FX Daily Starting Aug. 8

Chile’s central bank will start an international reserves accumulation program on August 8, where it will buy up to $25m of reserves per day for a three-year period, according to a statement.

PHILIPPINES (BBG): Philippines To Intervene More Forcefully In Streaks Of Weak Peso

The Philippine central bank is intervening more forcefully during periods of extended peso weakness as part of a new strategy, gradually moving away from day-to-day intervention, Governor Eli Remolona said.

EQUITIES (WSJ): Novo Nordisk’s Wegovy Weight-Loss Drug Sales Surge Despite Copycat Issues

Novo Nordisk said second-quarter sales of its blockbuster Wegovy weight-loss drug soared 67% on year, despite waves of U.S. patients using generic unbranded versions of the drug. The Danish company last week slashed full-year guidance, warning that copycat versions of its obesity and diabetes drugs in the U.S. were holding back sales of its branded treatments. Its share price plummeted on the news.

OIL (BBG): Trump Says He’s Readying More Tariffs on Russian Energy Buyers

President Donald Trump suggested he would impose increased tariffs on additional countries buying energy from Russia — including China — after saying earlier Tuesday that he would raise levies on Indian exports within 24 hours.

DATA

EUROZONE DATA (MNI): June Retails Sales Stronger Than Expected After Revisions

Eurozone (real) retail sales were inline with expectations in June on a sequential comparison, at 0.3% M/M, but the print was stronger on a level basis considering a positive revision to May (now -0.3%, revised from -0.7%). The uptrend in place since late-2023 continues even the level is still a little below 2021 highs.

GERMAN DATA (MNI): June Factory Orders Constitute A Move Sideways On Weak Levels

German factory orders were weaker than expected in June, at -1.0% M/M vs 1.1% consensus even considering a 0.6pp upward revision of the May figures to -0.8% (due to a large-scale order in the manufacture of other transport equipment which was reported late). Excluding large-scale one-offs, June orders were stronger, at +0.5% M/M. Considering that, the print broadly constitutes a move sideways on weak levels. Sentiment (ifo business climate manufacturing balance, Manufacturing PMI) meanwhile stands at cycle highs.

FRANCE DATA (MNI): Sequential Private Employment Growth Remains Tepid

French private payrolled employment growth was flat in Q2, according to INSEE’s flash data. That’s a marginal improvement from the -0.1% Q/Q in Q1 and -0.4% Q/Q in Q4 2024. However, on an annual basis private payrolls remain down 0.4% Y/Y.

JAPAN DATA (MNI): Japan June Negative Real Wages Narrow

Japan’s inflation-adjusted real wage, a key gauge of household purchasing power, remained in negative territory for a sixth consecutive month in June but narrowed to -1.3% from May’s 2.6% decline, preliminary data from the Ministry of Health, Labour and Welfare showed Wednesday.

NEW ZEALAND DATA (MNI): Q2 Sees Increased Labour Market Capacity

NZ employment was weaker in Q2 than the RBNZ projected in May declining 0.1% q/q and 0.9% y/y, in line with consensus, after a downwardly-revised 0.0% q/q & -0.7% y/y in Q1. The unemployment rate rose 0.1pp to 5.2%, highest since Covid-impacted Q3 2020, but as the RBNZ forecast. The next rate decision is on August 20 and will include an updated outlook. With job shedding continuing and activity indicators remaining lacklustre and inflation in the band, another 25bp rate cut is likely.

MARKETS

FOREX: USD Index Rangebound, Trump Announcement Eyed

The USD Index holds within a tight range so far Wednesday, keeping the weekly range at 98.585 - 99.073 for now. With relatively little data to distract, focus will remain on Trump's activities this week, particularly as the White House's deadline for Russia establishing a ceasefire with Ukraine expires this Friday. Trump's special envoy is meeting with the Russian President in Moscow today - and any comments following the discussions will be carefully watched.

As such, the USD is mixed across G10 - but outperformance in AUD, NZD currencies is noted. AUD/USD is through to a new weekly high at 0.6496 on continued equity strength - but the 50-dma remains out of reach for now at 0.6513. Equities in Europe are firmer, and US futures are also strong as markets look to reverse the weak daily close on Wall Street after the ISM services print.

AUD/JPY continues to trade either side of the 200-dma, and a break above 96.17 is needed to make progress back toward the cycle high of 97.43 and a formal resumption of the broader uptrend.

Tier one datapoints are few and far between Wednesday, with just Canadian final July PMI numbers and Weekly MBA mortgage applications due. Fed's Cook, Collins and Daly are on the schedule to speak today, and while none of them dissented at the most recent Fed meeting, markets will still be looking to gauge any signal on what could tip their vote to cut rates later this year.

Possibly more importantly, President Trump is set to make an announcement at 2130BST/1630ET today, and while the President has yet to specify what topic this will cover, markets expect he could be covering a decision on Russian secondary sanctions, his nomination for the next Fed governor to replace Kugler or the appointee to lead the Bureau of Labor Statistics, after he fired the previous head of the department on Friday.

EGBS: German Curve Bear Steepens Ahead Of Bund Supply

The German curve has bear steeped ahead of this morning’s 15-year Bund auction, with Schatz yields little changed at 1.91% and 30-year yields up 3bps at 3.17%. The 5s30s curve has moved away from Thursday’s 86.8bp multi-week low, now back at 94bps.

Bund futures are biased lower, albeit on light volumes, but a bullish technical theme remains intact. Futures are currently -17 ticks at 130.18, still above the 50-day EMA.

10-year EGB spreads to Bunds are up to 0.5bps wider today. The 10-year BTP/OAT spread has taken another leg lower since the end of July, now just below 14bps for the tightest since 2007.

This morning’s regional data has not been market moving. German factory orders were skewed lower by the volatile large-scale orders category (-1.0% M/M vs 1.1% cons, an upwardly revised -0.8% prior), while Italian industrial production was stronger-than-expected at 0.2% M/M (vs -0.2% cons, -0.8% prior). French private payrolls growth remains tepid, while Eurozone retail sales were in line at 0.3% M/M.

GILTS: Early Bear Steepening Holds, Global Supply & Crude Eyed

Gilts hold lower with the presence of global supply and an uptick in crude oil weighing.

Lows of 92.36 seen in futures so far, contract last -31 at 92.44.

Bears will look to force a break of Monday’s low (92.24) to expose the 20-day EMA (91.86), as they look to quell some of the recent bullish momentum. Initial resistance at yesterday’s high (92.84).

Yields 0.5-3.0bp higher, curve bear steepens.

2s10s back above 70bp after the first close below since early July, while 5s30s remains pinned around 140bp.

SONIA futures +1.0 to -3.5, strip twist steepens.

BoE-dated OIS showing ~49bp of easing through year-end, with over 90% odds of a cut priced for tomorrow.

Click for our full preview of tomorrow’s decision.

NIESR’s warning on the UK fiscal situation/need for meaningful tax hikes, has garnered most of the interest when it comes to local news developments.

Our political risk team notes that with Reform UK benefiting from significant public anger at Labour's handling of immigration and crime, breaking its manifesto promises on tax could further damage the gov'ts standing ahead of elections to the Scottish and Welsh parliaments and English local councils in 2026.

Little of note on the UK macro calendar today, which will leave focus on cross-market matters (Fed leadership, global trade etc.) for much of the day.

EQUITIES: Stock Futures Point to Higher Open Wednesday

US Equities sold off sharply Friday on the back of the soft NFP print - pushing prices through mid-July lows in the process. This puts price well clear of support at the 20-day EMA, at 6325.25, signalling scope for a deeper retracement. The trend condition in Eurostoxx 50 futures faltered Friday, with short-term weakness resulting in a break of the bear trigger. Having shown below 5194.00, the Jun 23 low, the April 30 hi/lo range at 5078-5138 becomes the area of downside interest.

Japan's NIKKEI closed higher by 245.32 pts or +0.61% at 40794.86 and the TOPIX ended 30.03 pts higher or +1.02% at 2966.57.

Elsewhere, in China the SHANGHAI closed higher by 16.397 pts or +0.45% at 3633.995 and the HANG SENG ended 8.1 pts higher or +0.03% at 24910.63.

Across Europe, Germany's DAX trades higher by 41.44 pts or +0.17% at 23887.69, FTSE 100 higher by 13.77 pts or +0.15% at 9156.33, CAC 40 up 19.85 pts or +0.26% at 7640.89 and Euro Stoxx 50 up 11.6 pts or +0.22% at 5261.19.

Dow Jones mini up 159 pts or +0.36% at 44401, S&P 500 mini up 21.75 pts or +0.34% at 6347, NASDAQ mini up 43 pts or +0.19% at 23175.25.

COMMODITIES: Gold Consolidating at Higher Levels

Gold benefited from the soft NFP print on Friday, returning prices toward the top-end of the recent range. This supports the view that short-term weakness is corrective - for now - and a bull cycle that started Jun 30 remains intact. WTI futures fell for a fourth consecutive session into the Tuesday close, keeping S/T momentum pointed lower. Support to watch remains the 50-day EMA, at $65.48 - a level pierced yesterday. A clear break would expose $58.17, the May 30 low.