MNI US MARKETS ANALYSIS - UK Econ Weak Even Prior to Oil Shock

Highlights:

- Stubbornly high oil prices results in another upleg for USD; USD Index now targeting range breakout

- GBP among the weakest in G10 as GDP data points to economy already soft ahead of any oil price shock

- PCE data in focus, Canadian jobs numbers also due

US TSYS: Broad Consolidation Of Yesterday's Significant Bear Flattening

Treasuries have recently seen a small bid from news that an Indian oil tanker moved through the Strait of Hormuz but still broadly consolidate yesterday’s large bear flattening on a renewed surge in energy prices. Middle East conflict headlines and Strait of Hormuz flows will remain in clear focus but today also sees data including January PCE/Q4 GDP revisions at 0830ET before January JOLTS at 1000ET.

- Cash yields are 1.1bp lower (3s) to 0.7bp higher (30s) for mild twist steepening.

- 2Y yields trade at 3.734% (-0.7bp) after yesterday’s first clearance of 3.75% since August, having briefly pushed above it again earlier today.

- 2s10s trades at 52.9bp (+0.5bp) after yesterday’s 49.6bp was the flattest since November.

- TYM6 trades at 111-17+ (+04+) off an earlier low of 111-12, on solid cumulative volumes of 475k albeit light by recent week standards.

- A bear cycle remains intact and yesterday's strong sell-off reinforces current bearish conditions. Sights are on the next key support at 111-06+ (Jan 20 low) with clearance highlighting an important medium-term bearish development. A clear break of firm resistance at 112-15+ (20-day EMA) is required to signal a possible reversal.

- Data: PCE Jan (0830ET), GDP 2nd Q4 release (0830ET),Durable goods Jan prelim (0830ET), JOLTS Jan (1000ET), U.Mich consumer survey Mar prelim (1000ET)

- Politics: Trump signs executive orders (1400ET), Trump in greeting with national finals rodeo winners (1500ET)

STIR: US Rates Consolidate Hawkish Shift, Next Hike Not Seen Until Mid-2027

- US rates broadly consolidate yesterday’s latest hawkish shift from higher oil prices, with a next Fed cut not fully priced until mid-2027.

- Markets will remain acutely sensitive to geopol headlines but today also sees the delayed Jan PCE/2nd Q4 GDP release at 0830ET before January JOLTS at 1000ET.

- FF cumulative cuts from 3.64% effective: 0bp for next week, 1bp Apr, 5.5bp Jun, 9.5bp Jul, 12.5bp Sep, 14.5bp Oct and Dec 20bp

- SOFR futures are currently up to 3 ticks firmer in most 2027 contracts, with the terminal implied yield of 3.365% (Z7/H8) only 2.5/3bps lower on the day after yesterday’s 13.5bp increase.

US TSY FUTURES: Short Setting Dominated On Thursday

OI data points to net short setting dominating as Tsy futures sold off on Thursday, with net long cover in TY futures providing the only break in the wider theme. TU futures saw the biggest net positioning shift (~$6.1mln DV01).

| 12-Mar-26 | 11-Mar-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,723,240 | 4,568,593 | +154,647 | +6,123,812 |

FV | 6,669,235 | 6,634,965 | +34,270 | +1,514,513 |

TY | 5,345,996 | 5,371,475 | -25,479 | -1,694,119 |

UXY | 2,348,697 | 2,348,364 | +333 | +30,077 |

US | 1,825,790 | 1,819,218 | +6,572 | +889,766 |

WN | 2,231,945 | 2,218,835 | +13,110 | +2,364,805 |

|

| Total | +183,453 | +9,228,855 |

SOFR: Short Setting Dominated In Futures On Thursday

OI data indicates that short setting dominated as SOFR futures sold off on Thursday, with the most prominent moves once again coming in the reds. Only 3 rounds of net long cover were seen through the blues, all coming further back on the strip (SFRU8, Z8 & M9).

- SFRZ6 saw the largest net OI swing (rising by over 133K lots).

| 12-Mar-26 | 11-Mar-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,312,337 | 1,304,260 | +8,077 | Whites | +99,047 |

SFRH6 | 1,350,937 | 1,337,367 | +13,570 | Reds | +228,249 |

SFRM6 | 1,323,419 | 1,280,000 | +43,419 | Greens | +46,345 |

SFRU6 | 1,264,556 | 1,230,575 | +33,981 | Blues | +2,314 |

SFRZ6 | 1,477,564 | 1,343,900 | +133,664 |

|

|

SFRH7 | 1,038,339 | 991,362 | +46,977 |

|

|

SFRM7 | 983,675 | 943,639 | +40,036 |

|

|

SFRU7 | 804,261 | 796,689 | +7,572 |

|

|

SFRZ7 | 1,052,203 | 1,038,663 | +13,540 |

|

|

SFRH8 | 553,757 | 531,625 | +22,132 |

|

|

SFRM8 | 470,194 | 457,569 | +12,625 |

|

|

SFRU8 | 398,175 | 400,127 | -1,952 |

|

|

SFRZ8 | 408,051 | 428,963 | -20,912 |

|

|

SFRH9 | 258,780 | 242,666 | +16,114 |

|

|

SFRM9 | 196,284 | 197,901 | -1,617 |

|

|

SFRU9 | 184,765 | 176,036 | +8,729 |

|

|

WHITE HOUSE: Politico-VP Vance 'Sceptical' Of Iran Strikes

Politico reports that, according to two Trump administration officials, Vice President JD Vance was a sceptical voice within the White House in the run-up to the launch of strikes on Iran. While the officials emphasised that once the decision was made to go ahead, the VP gave the plan his full backing, there will still be speculation that a schism is emerging between Vance and President Donald Trump. Speaking to reporters earlier in the week, Trump acknowledged the difference of opinion, saying Vance “was, I’d say, philosophically a little different from me. I think he was maybe less enthusiastic about going, but he was still quite enthusiastic.”

- The VP has been a long-term isolationist voice within the Republican party, and was initially not in favour of US strikes on the Houthis in Yemen in 2025 following attacks on shipping in the Red Sea. The sharp pivot to international intervention in 2026, including the operation to capture Venezuelan President Nicolas Maduro, the strikes on Iran, and threats against Cuba, has resulted in a less-prominent role for Vance in public messaging. Instead, Secretary of State Marco Rubio has been front and centre alongside Trump and Secretary of Defense/War Pete Hegseth.

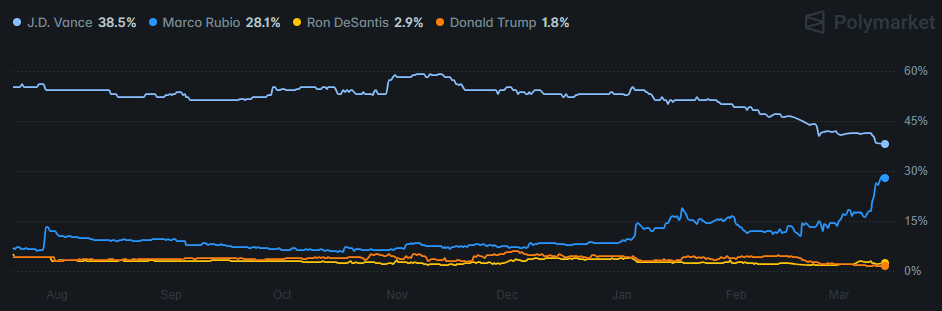

- The immediate impact of Vance's scepticism is minimal in terms of market relevance. The more notable impact could come further in the future. Trump has spoken of both Vance and Rubio as potential 2028 Republican presidential candidates, while refusing to state a preference. While it is still too far away for any concrete predictions, political prediction markets have shown a narrowing in the gap between the two, with Vance's implied probability of getting the nomination falling from 59% in mid-November to 38.5% presently, according to Polymarket. Meanwhile, Rubio's implied probability has risen from 7.8% to 28.1% in the same timeframe.

Chart 1. Predictions Market Implied Probability of Winning 2028 Republican Presidential Nomination, %

GERMANY: Merz: It Is Wrong For US To Ease Sanctions On Russian Oil

Speaking from Andøya, Norway, German Chancellor Friedrich Merz says that his gov't learned earlier this morning about the US decision to ease sanctions to allow other countries to purchase Russian oil already at sea. US Treasury Secretary Scott Bessent claimed that the relaxation was aimed at promoting "stability in global energy markets". He said the "short-term measure" would "not provide significant financial benefit to the Russian government". Merz says he would like to know the motivations of the US gov't regarding the waiver, and that "We believe it is wrong to ease sanctions [on Russia] now, for whatever reason."

- Merz: "Unfortunately, Russia continues to show no willingness to negotiate. We will therefore, and must, continue to increase the pressure on Moscow. We will not be deterred or distracted from [supporting Ukraine] by the Iran nuclear deal." In the initial aftermath of the US/Israeli strikes on Iran, Merz was viewed as delivering some of the most, if not positive, then at least measured comments from an EU leader, saying Germany would not 'lecture' the US regarding the attacks. In recent days, this tone has shifted somewhat.

- Speaking in Prague on 10 March, Merz said, “With each day of war, more questions arise. What concerns us most is that there is clearly no common plan for bringing this war to a swift and convincing conclusion. We have no interest in an endless war”. Today, Merz added that "Germany is not part of the Iran war, [and] has no intention to become one".

CROSS ASSET: Oil Off Highs After Turkish Ship Passes Strait Of Hormuz

Bonds and equities trade away from session lows and the broader USD pulls back from highs as crude backs off from session highs.

- The pullback in crude was already in play before an Axios report, suggesting that President Trump told G7 leaders in a virtual meeting Wednesday that Iran is "about to surrender”, provided some brief additional downside.

- Our commodities team didn’t see a clear driver for weakness in crude oil at the time but a RTRS report covering comments from the Turkish Transport Minister noted that “a Turkish-owned ship that had been waiting near Iran was allowed to pass through the Strait of Hormuz after authorities received permission from Tehran”. Prior dissemination of the comments may have generated at least some of the recent downside in crude.

- If a Turkish vessel has been allowed passage through the Strait it may help to explain/verify comments made by Iran’s Deputy FM yesterday, noting that Iran has allowed ships from some countries to pass.

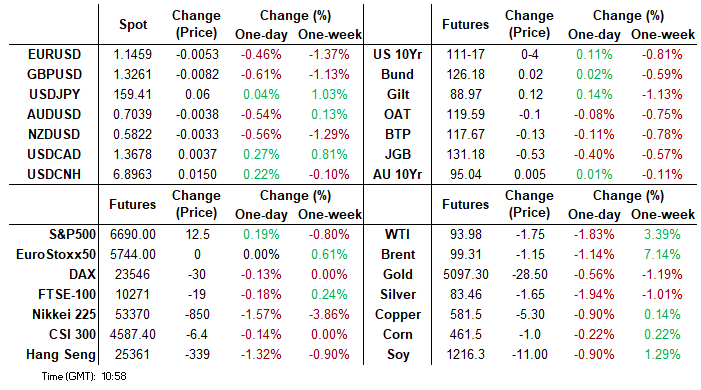

FOREX: DXY Extends March Higher, EURUSD Below Key Support

- Despite a steadier session for energy prices on Friday, expectations that the conflict in the Middle East could persist for longer than first thought are continuing to drive the dollar higher. This has prompted the USD index to extend weekly highs above he 100 mark, and notably narrowing the gap to the November highs for the index.

- There was a notable pop higher for USDJPY overnight, which saw the pair breach the bull trigger at 159.45. Session highs of 159.69 represent the highest traded levels since July 2024, and have prompted some further FX jawboning from officials in Japan. Finance Minister Satsuki Katayama told reporters on Friday that financial authorities are staying in closer contact with their US counterparts than usual, and that she would refrain from commenting on the topic of currency intervention.

- This has prompted a moderation for the pair back to 159.35, and has allowed the broader dollar strength to be concentrated against other majors within the G10. The likes of EUR, GBP, AUD and NZD are all trading with 0.5% declines today.

- For EURUSD, spot has notably traded back below 1.15, and downside momentum has gathered pace on a break of the November lows through 1.1469. The next notable target on the downside is at 1.1392, the Aug 2025 low.

- AUDUSD extends its reversal from this week’s cycle highs to 2% on Friday. Despite, expectations for an RBA rate hike this week being behind the Aussie’s resilience, spot remains sensitive to broader risk pullbacks. Key support for the pair remains further down at 0.6963, the 50-day EMA.

- ECB's Wunsch is unlikely to speak on monetary policy matters today as the ECB remains in its pre-decision quiet period. On data, we'll get Eurozone industrial production, Canada employment, US PCE, Michigan consumer expectations, and JOLTS.

OPTIONS: Expiries for Mar13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E967mln), $1.1550(E740mln), $1.1585-00(E3.0bln),$1.1645-50($1.1bln), $1.1670(E1.8bln), $1.1700(E2.3bln)

- USD/JPY: Y158.00-05($800mln), Y159.00($625mln)

- EUR/JPY: Y184.00(E528mln)

- GBP/USD: $1.3420-25(Gbp1.1bln)

- AUD/USD: $0.7100(A$896mln), $0.7130(A$839mln)

- USD/CAD: C$1.3835-40($770mln)

EQUITIES: E-Mini S&P Narrows Gap to Key Medium-Term Support at 6583.00

- The sharp rebound in EuroStoxx 50 futures from Monday’s low is for now, considered corrective and this is allowing an extreme oversold trend condition to unwind. Key short-term resistance to watch is 5919.41, the 50-day EMA. A clear break of this average is required to signal a possible reversal. A resumption of the bear leg would open 5500.00, the Nov 21 ‘25 low. A clear breach of it would strengthen the bear cycle.

- A sharp bounce in S&P E-Minis on Monday and the reversal from Tuesday’s high highlights the fact that recent gains were most likely corrective. This has allowed a recent oversold trend condition to unwind. A continuation lower would open 6583.00, the Nov 21 ‘25 low and the next key medium-term support. Clearance of this level would strengthen a bearish threat. Initial firm resistance is 6878.09, the 50-day EMA.

COMMODITIES: WTI Futures Hoilding Onto Bulk of Thursday's Rally

- A volatile impulsive bull wave in WTI futures remains intact. The recent sharp pullback has allowed an extreme overbought trend condition to unwind. A key support zone to monitor is $76.92 - $68.95, the area between the 20- and 50-day EMAs. A clear break through this zone would signal a possible trend reversal. On the upside, a continuation higher near-term would open $103.15 next, a Fibonacci retracement.

- Gold remains in consolidation mode and is trading below $5419.11, the Mar 2 high. A short-term bullish theme is intact following recent gains. The metal has cleared all key retracement points of the sharp sell-off between Jan 29 - Feb 2. This strengthens the short-term bullish theme and signals scope for an extension towards key resistance and the bull trigger at $5595.5, the Jan 29 high. Initial firm support to watch lies at $4921.6, the 50-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 13/03/2026 | 1230/0830 | *** | Labour Force Survey | |

| 13/03/2026 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 13/03/2026 | 1230/0830 | * | Intl Investment Position | |

| 13/03/2026 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 13/03/2026 | 1230/0830 | *** | Personal Income and Consumption | |

| 13/03/2026 | 1230/0830 | ** | Durable Goods New Orders | |

| 13/03/2026 | 1400/1000 | *** | JOLTS | |

| 13/03/2026 | 1400/1000 | *** | UMich Surveys of Consumers | |

| 13/03/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |