US TSYS: Broad Consolidation Of Yesterday's Significant Bear Flattening

Treasuries have recently seen a small bid from news that an Indian oil tanker moved through the Strait of Hormuz but still broadly consolidate yesterday’s large bear flattening on a renewed surge in energy prices. Middle East conflict headlines and Strait of Hormuz flows will remain in clear focus but today also sees data including January PCE/Q4 GDP revisions at 0830ET before January JOLTS at 1000ET.

- Cash yields are 1.1bp lower (3s) to 0.7bp higher (30s) for mild twist steepening.

- 2Y yields trade at 3.734% (-0.7bp) after yesterday’s first clearance of 3.75% since August, having briefly pushed above it again earlier today.

- 2s10s trades at 52.9bp (+0.5bp) after yesterday’s 49.6bp was the flattest since November.

- TYM6 trades at 111-17+ (+04+) off an earlier low of 111-12, on solid cumulative volumes of 475k albeit light by recent week standards.

- A bear cycle remains intact and yesterday's strong sell-off reinforces current bearish conditions. Sights are on the next key support at 111-06+ (Jan 20 low) with clearance highlighting an important medium-term bearish development. A clear break of firm resistance at 112-15+ (20-day EMA) is required to signal a possible reversal.

- Data: PCE Jan (0830ET), GDP 2nd Q4 release (0830ET),Durable goods Jan prelim (0830ET), JOLTS Jan (1000ET), U.Mich consumer survey Mar prelim (1000ET)

- Politics: Trump signs executive orders (1400ET), Trump in greeting with national finals rodeo winners (1500ET)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - S&P E-Minis Bull Trigger Remains Exposed

- In the equity space, the firm reversal higher on Feb 6 in S&P E-Minis refocuses attention on the primary uptrend and key resistance at 7043.00, the Jan 28 high. Clearance of this level would confirm a resumption of the trend and mark the end of a flat correction in the contract. Key short-term support has been defined at 6751.50, the Feb 6 low, where a break is required to highlight a top and a stronger short-term reversal.

- The medium-term trend condition in EUROSTOXX 50 futures remains bullish and yesterday's fresh cycle high reinforces the bull theme. The move higher paves the way for a climb towards 6100.00, and 6134.00, a 1.382 projection of the Nov 21 - Dec 12 - 18 price swing. Key support to watch lies at the 50-day EMA, at 5890.56. Clearance of this average would highlight a short-term top and signal scope for a deeper pullback.

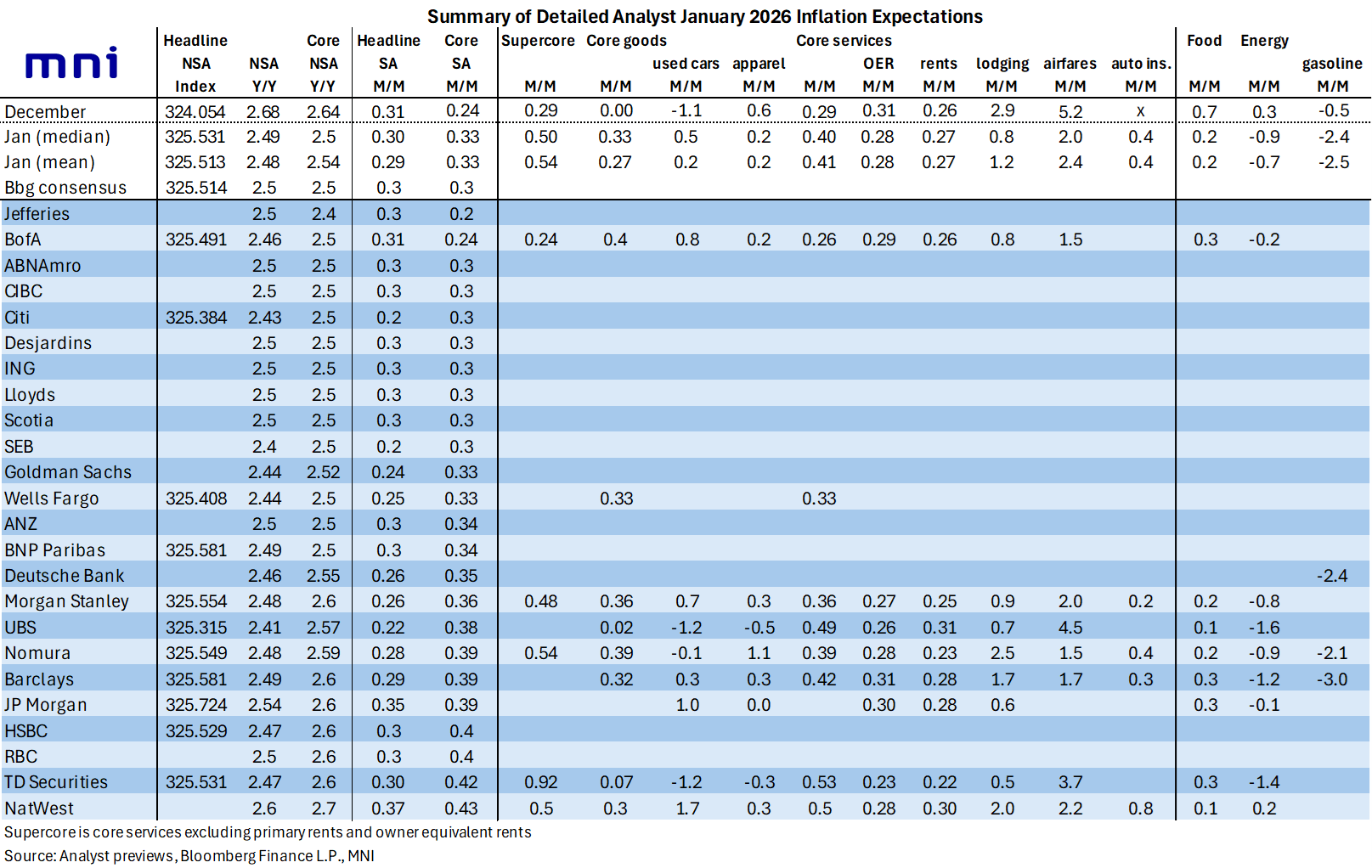

US PREVIEW: Used Cars and Smaller Services Behind Expected Core CPI Firming

Analysts look for the acceleration in core CPI to come from both goods and services:

- on the core goods side, used cars are on balance expected to play a large role in the sequential firming, shifting from -1.1% M/M in December to perhaps a small positive. That’s far from a uniform view though with an analyst range of -1.2% to 1.7%.

- going against this but with a smaller weight, apparel is on balance expected to moderate with a median 0.2% estimate after a strong 0.6% M/M in December.

- on the core services side, the sequential firming comes despite relative softening in some of the noisier non-housing categories that can swing broader inflation from month-to-month. In particular, airfares (no feed through to PCE) and lodging away from home (feeds through to PCE) are expected to moderate after strong increases in December.

- rental inflation is expected to be fractionally softer than in December, with an average estimate of 0.28% for OER (range 0.23-0.31) after 0.31% but tenants’ rents at 0.27% (range 0.22-0.31) after 0.26%.

- the gap, with these large service components at similar monthly pace/softer than in December likely reflects a residual seasonality boost expected more broadly.

Away from core CPI, headline inflation is expected to be weighed on by softer food and energy inflation.

- Food inflation is expected to moderate heavily after a far stronger than expected 0.7% M/M in December, its strongest monthly increase since Aug 2022 but also a move that looked suspiciously like a reversal of November holiday discounting (with the later than survey period back in November).

- Energy prices are also expected to have seen a reasonable seasonally adjusted decline after a modest increase in December. Note the wider than usual range to analyst estimates this month (from -1.6% to 0.2%) which we suspect is down to treatment of differing natural gas and electricity price assumptions.

[A quick reminder that the below table shows median/mean figures across all estimates. The core CPI median of 0.33% M/M would be 0.36% M/M if only taking unrounded estimates per the separate table shown above]

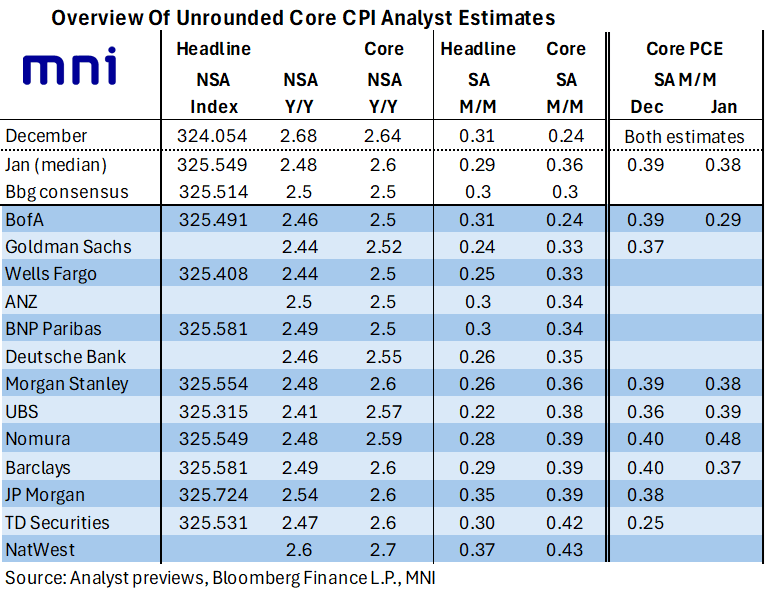

US PREVIEW: Unrounded Core CPI Estimates Point To Upside Risk In January

Today’s NFP report is clearly in immediate focus but we quickly look ahead to Friday’s CPI report, where unrounded core CPI estimates point to upside risk to consensus compared to more in-line/softer readings for headline.

- We see a median of thirteen unrounded estimates for core CPI at 0.36% M/M (Bloomberg cons 0.3) having surprised clearly lower back in December with 0.24% M/M vs the median estimate of 0.35% at the time.

- This monthly strength also translates to upside risk for the Y/Y figures in NSA data, with a median 2.6% vs 2.5% consensus after 2.64% in December. Include a wider range of rounded estimates and this would sit on the cusp of a 2.5-2.6% Y/Y print (to be shown in a second table in part two).

- Headline estimates look more in line with consensus however, with a median 0.29% M/M (Bloomberg cons 0.3). They are also closer to the rounded consensus of 2.5% Y/Y with some seeing risk of rounding lower.

- A smaller sample of unrounded estimates for core PCE currently tracks at 0.39% M/M in December and 0.38% M/M in January. The delayed December PCE report is currently due to be released on Feb 20 before the January report on Mar 13.

- The full MNI US CPI Preview will be published later today once the payrolls report is fully wrapped up.