MNI US MARKETS ANALYSIS - Tsys Hold Gains Ahead of House Vote

Highlights:

- Treasuries hold gains as government on cusp of re-opening; House vote due later today

- USDJPY looks through verbal warnings, hits new cycle high

- Heavy Fedspeak schedule, balance sheet discussions in focus

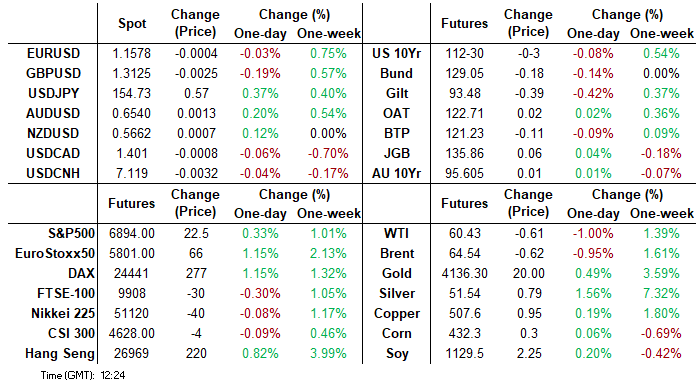

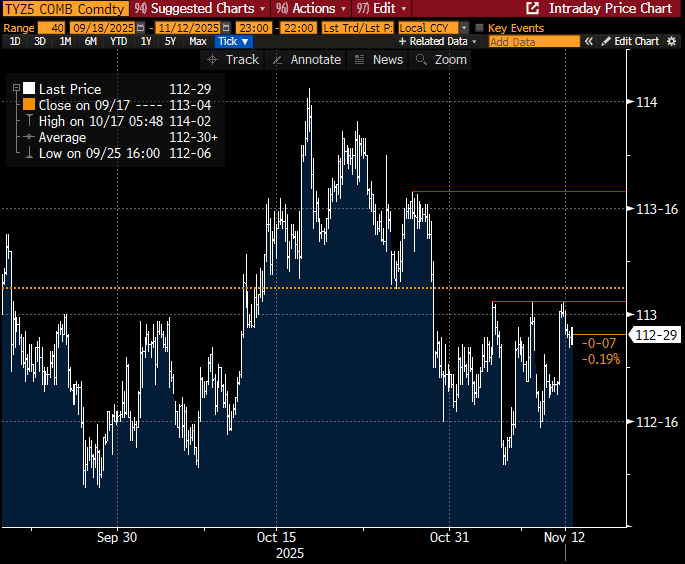

US TSYS: TYA Hovering Close To Tuesday’s Latest Test Of Key Resistance

- Cash Treasuries have modestly pared sizeable gains seen with the Asia open after yesterday’s cash closure for Veterans Day, catching up with a rally in futures on soft weekly ADP employment data.

- Today sees focus on Tsy Sec Bessent speaking at the 2025 Treasury Market Conference, balance sheet discussions from Fed speakers and 10Y supply.

- Tomorrow could then greater focus on potential timing of official data releases that have been delayed under the government shutdown. See the MNI Re-Opening Guide here.

- Cash yields are 1-3.5bp lower since Monday’s close, with declines led by 5s.

- TYZ5 trades at 112-28+, holding only a mild easing away from yesterday’s high of 113-02 on light overnight volumes of 225k.

- That high marked another test of key near-term resistance having also hit 113-02 on Nov 5 & 7, after which lies 113-18+ (Oct 28 high). A bear threat is still present at 112-06 (Sep 25 low) before which lies 112-09+ (Nov 5 high) and other support levels.

- Data: MBA mortgage applications (0700ET)

- Fedspeak: Williams (0920ET), Paulson (1000ET), Waller (1020ET), Bostic (1215ET), Miran (1230ET), SOMA Manager Perli (1550ET), Collins (1600ET) – see FED bullet

- US Tsy Sec Bessent speaks at 2025 Treasury Market Conference (1045ET)

- Coupon issuance: US Tsy $42B 10Y Note - 91282CPJ4 (1300ET). The first auction of the week, a 3Y, stopped through by 1bp and saw healthy demand whlist last month’s 10Y tailed by 0.5bp with the bid-to-cover falling from 2.65 to 2.45.

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: White House Press Sec Leavitt conference (1300ET), Trump hosts private dinner (1930ET)

STIR: Fed Rates Mostly Still Reflect Soft Weekly ADP

- Fed Funds implied rates have pared most of yesterday’s reaction to soft weekly ADP data specifically for next month's FOMC meeting, although the dovish impact is held further out.

- Cumulative cuts from 3.87% effective: 15.5bp Dec, 26bp Jan, 37bp Mar, 44bp Apr and 58bp Jun.

- Some notable earlier Fed Funds flow: FFF6/G6 paper paid -9.5 on 22.5K, ~24K trades there all day.

- SOFR futures are 1-2 ticks lower on the day, with the implied yield at

- The SOFR implied terminal yield of 3.08% (H7, -1.5bp) holds a sizeable pullback from last week’s multi-month high of 3.16% prior to a softening in a succession of lower tier labor releases.

FED: Today’s Fedspeak Likely More Notable On Balance Sheet Discussions

Today sees six different scheduled FOMC speakers, even if we expect the main interesting comments from a traditional monetary policy angle to come Collins late on. Speaking focus instead is likely on balance sheet considerations, first with NY Fed’s Williams before NY Fed SOMA Manager Perli, seen in light of funding pressures last month as reserves have moved closer to ample.

- 0920ET – NY Fed’s Williams (voter) keynote speech at Treasury Market Conference (text only). He said on Friday that it won’t be long before reserves are ample at which point the Fed will begin gradual purchases of assets to maintain growth in liabilities. As for the rate outlook, he repeated that the natural interest rate is hard to pin down but he still thinks a low r* era is still with us.

- 1000ET – Paulson (’26) at fintech conference (text only). The topic could limit mon pol discussion although she indicated ahead of the Oct 29 FOMC decision that she’s in-line with the median FOMC voter looking for another cut in December.

- 1020ET – Gov. Waller (voter) on payments at fintech conference (no text). Again, unlikely to meaningfully touch on mon pol and he’s clearly in the camp for another cut in December.

- 1215ET – Bostic (non-voter) at Atlanta Economics Club (text + Q&A). He "eventually got behind" last month’s cut but finds it preferable to move slower when there's so little clarity.

- 1230ET – Miran (voter) in fireside chat (no text). The outright dove on the FOMC with two dissents for 50bp cuts in both Sept and Oct meetings, he continues to call for a 50bp cut next month as well.

- 1600ET – Collins (’25) at community banking conference (text only). These could be her first mon pol comments since the Oct FOMC decision, having said beforehand that perhaps another 25bp of easing might be appropriate. That of course was delivered last month which could see in a December pause camp.

- Outside of those FOMC speakers, we also note that Roberto Perli (NY Fed SOMA Manager) will give closing remarks at the Treasury Market Conference today at 1550ET, with the 20min slot allowing reasonable detail.

US (MNI): U.S. Federal Data Re-Opening 2025: FAQs

With the U.S. federal government shutdown that began Oct 1 set to end later this week, dozens of postponed government agency data reports are due to be rescheduled for release over the coming weeks and months. Some may be cancelled altogether. We go through the prospects for major data releases over the coming weeks in the attached PDF. MNI’s rough estimates are in the table included in the link – we will publish updates to the official calendar as and when they are announced in the coming days.

US (MNI): Govt Funding Package Clears Rules Committee, Final Vote Expected After 16:00 ET

The House Rules Committee voted 8-4 along party lines to advance the Senate-passed government funding package to the floor of the House of Representatives, clearing a key procedural hurdle to reopening the government. The rule sets one hour of debate on the bill, followed by a final vote. The House will hold its first votes since September 19 at 16:00 ET 21:00 GMT. As the shutdown impasse was ended with the votes of eight 'rebel' Democrat Senators, the underlying conflict remains unresolved. If lawmakers fail to complete the remaining nine annual bipartisan spending bills by the new January 30 deadline, there is a risk of a second shutdown in February.

EUROPE ISSUANCE UPDATE

Gilt linker syndication: Priced

- GBP4.25bln (MNI expected GBP GBP4.5-5.5bln) of the 1.75% Sep-38 linker. Reoffer: 99.065 to yield 1.8319%. Spread set earlier at 1.125% Nov-37 linker (GB00B1L6W962) +10.50bps (guidance was +10.50 / +10.75bps), books closed in excess of GBP69bln.

German auction results

- E1bln (E898mln allotted) of the 2.50% Aug-46 Bund. Avg yield 3.15% (bid-to-offer 3.08x; bid-to-cover 3.43x).

- E1.5bln (E1.14bln allotted) of the 2.90% Aug-56 Bund. Avg yield 3.26% (bid-to-offer 0.99x; bid-to-cover 1.30x).

US TSY FUTURES: Net Long Setting Most Prominent After Weekly ADP

OI data points to net long setting (TU, FV, TY, US & WN) dominating more modest instances of net short cover (UXY) as Tsy futures rallied in the wake of the soft weekly ADP employment data on Tuesday.

- Still, limited net OI swings may point to low conviction given the lack of market familiarity with the weekly readings and questions surrounding crossover with official labour market data.

| 11-Nov-25 | 10-Nov-25 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,642,944 | 4,628,965 | +13,979 | +523,673 |

| FV | 6,928,004 | 6,904,085 | +23,919 | +1,026,220 |

| TY | 5,427,595 | 5,421,361 | +6,234 | +417,163 |

| UXY | 2,499,406 | 2,501,417 | -2,011 | -180,794 |

| US | 1,853,883 | 1,850,407 | +3,476 | +443,286 |

| WN | 2,170,561 | 2,167,018 | +3,543 | +663,085 |

| Total | +49,140 | +2,892,633 |

SOFR: Long Setting Most Prominent In Futures On Tuesday

OI data shows a clear skew towards net long setting as SOFR futures rallied in the wake of the soft weekly ADP employment data on Tuesday. Only limited instances of net short cover were seen through the blues.

- Still, akin to what was seen in the long end, limited net OI swings may point to low conviction given the lack of market familiarity with the weekly ADP readings and questions surrounding crossover with official labour market data.

| 11-Nov-25 | 10-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,363,554 | 1,364,053 | -499 | Whites | +32,362 |

SFRZ5 | 1,435,679 | 1,417,618 | +18,061 | Reds | +15,498 |

SFRH6 | 1,216,739 | 1,213,147 | +3,592 | Greens | +2,736 |

SFRM6 | 1,108,661 | 1,097,453 | +11,208 | Blues | +1,517 |

SFRU6 | 1,111,865 | 1,104,872 | +6,993 |

|

|

SFRZ6 | 1,194,466 | 1,196,404 | -1,938 |

|

|

SFRH7 | 837,646 | 830,816 | +6,830 |

|

|

SFRM7 | 820,498 | 816,885 | +3,613 |

|

|

SFRU7 | 766,722 | 764,859 | +1,863 |

|

|

SFRZ7 | 806,859 | 804,365 | +2,494 |

|

|

SFRH8 | 430,004 | 429,602 | +402 |

|

|

SFRM8 | 408,577 | 410,600 | -2,023 |

|

|

SFRU8 | 352,291 | 356,268 | -3,977 |

|

|

SFRZ8 | 330,459 | 330,641 | -182 |

|

|

SFRH9 | 206,732 | 201,849 | +4,883 |

|

|

SFRM9 | 187,098 | 186,305 | +793 |

|

|

FOREX: USDJPY Uptrend Extends, Ignoring Verbal Warnings

- The Japanese yen has weakened again Wednesday, with USDJPY’s move higher notable given further FX jawboning from Finance Minister Katayama, who reiterated authorities are closely watching FX moves with a high sense of urgency.

- This has led USDJPY to erase the ADP-driven losses from Tuesday, and then accelerate through 154.50, a level that had been holding across early November. Furthermore, 154.80 has also been cleared, placing the pair at the highest level since February. This puts sights on 155.35, a Fibonacci projection. A number of cross-Yen also stand at noteworthy levels, CHFJPY for example sees fresh all-time highs at 193.82.

- EURCHF (-0.23%) sees further downside pressure as a function of the looming US-Swiss trade deal, to session lows of 0.9246 at typing. This keeps the extremely significant support cluster between 0.9206-22 for EURCHF in high focus for those looking for a break to the lowest levels since the peg removal in 2015. Meanwhile USDCHF (-0.15%) has tracked further back below the 0.8000 handle.

- Internal criticism from a senior Labour party member weighed on GBP this morning, followed by a sudden move lower that may have been flow or fix related. On net, GBPUSD sits at 1.3118, with first support and the bear trigger for the pair at 1.3010, the Nov 4 and 5 lows.

- US MBA Mortgage applications as well as Canada building permits highlight the data calendar today. A set of Fed speakers is scheduled for today, while ECB's de Guindos and BoE's Pill are also set to speak but likely won't move the needle. The US government is expected to reopen tomorrow if the House expectedly signs the deal on that today.

SOUTH KOREA: Bond Market Pressures Raise Risk of Hawkish Turn from BoK

Local market tumult persists in South Korea - and reduces the risk of another BoK rate cut, and raises the risk of a return of hawkish language across the rest of 2025.

- The front-end of the curve added as much as 11bps overnight, triggering a report in Yonhap that the government are "closely monitoring" bond yields, which they see as showing signs of excessive volatility. ( Yonhap article is here: https://news.einfomax.co.kr/news/articleView.html?idxno=4383595 ) The article makes reference to the 3-year yield hitting 2.96% for a new 2025 high.

- More importantly, the spread of the 3-year yield over the BoK base rate has risen sharply, and is nearing the highest levels in two years - a signal that market conditions are tightening despite the BoK insisting they remain in an easing cycle.

- Much of the market stress stems from Rhee pinning property price rises as "way above" expectations, and the optionality over the direction of policy ahead: "even the change of direction [of policy rates] will depend on the new data that we'll see".

- USDKRW edged off a new cycle high of 1470.10 overnight on Rhee's comments, and leaves a possible November rate cut as considerably less likely - particularly as November CPI isn't due until December 1st, just 4 days after the next BoK meeting.

- A conclusion of BoK easing and a hawkish outturn may not mean a reversal of KRW strength, however, which remains more closely tied to net foreign outflows from local equities: https://www.mnimarkets.com/articles/krw-suffers-on-foreign-outflow-reinforcing-link-with-risk-appetite-1762530364740

OPTIONS: Expiries for Nov12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-05(E1.1bln), $1.1550(E790mln), $1.1585-90(E565mln), $1.1645-50(E855mln), $1.1688-90(E1.3bln)

- USD/JPY: Y154.00($500mln)

- GBP/USD: $1.3100(Gbp1.9bln), $1.3150(Gbp674mln), $1.3225-30(Gbp1.3bln)

- AUD/USD: $0.6500(A$1.4bln), $0.6530-50(A$1.4bln)

- NZD/USD: $0.5600(N$538mln)

EQUITIES: This Week's Climb for Eurostoxx Reinforces Bullish Conditions

A medium-term bull trend in Eurostoxx 50 futures remains intact and this week’s gains reinforce bullish conditions. The contract has traded through resistance at 5742.00, the Oct 29 high to confirm a resumption of the uptrend. This paves the way for an extension towards 5777.41 next, a Fibonacci projection. On the downside, initial firm support is seen at 5655.99, the 20-day EMA. The trend condition in S&P E-Minis remains bullish and the bear leg since the Oct 30 high appears to have been a correction. The contract has managed to find support below the 50-day EMA, currently at 6722.19, and a key level. Activity on Nov 7 highlights a potential reversal signal - a bullish doji candle. This defines key support at 6655.50, the Oct 7 low. Sights are on 6953.75, Oct 30 high and bull trigger.

- Japan's NIKKEI closed higher by 220.38 pts or +0.43% at 51063.31 and the TOPIX ended 37.75 pts higher or +1.14% at 3359.33.

- Elsewhere, in China the SHANGHAI closed lower by 2.618 pts or -0.07% at 4000.14 and the HANG SENG ended 226.32 pts higher or +0.85% at 26922.73.

- Across Europe, Germany's DAX trades higher by 299.74 pts or +1.24% at 24387.14, FTSE 100 lower by 2.35 pts or -0.02% at 9897.22, CAC 40 up 73.29 pts or +0.9% at 8229.52 and Euro Stoxx 50 up 60.93 pts or +1.06% at 5786.63.

- Dow Jones mini up 77 pts or +0.16% at 48107, S&P 500 mini up 26.25 pts or +0.38% at 6897.75, NASDAQ mini up 173 pts or +0.67% at 25815.5.

COMMODITIES: Recent Gains Suggests Corrective Cycle for Gold is Over

The pullback in WTI futures since Oct 24, appears to be a flag formation - a bullish continuation pattern. This suggests that an upward corrective cycle is intact for now. Price has recently traded through the 50-day EMA, at $60.85, signalling scope for a stronger recovery. Note too that resistance at $62.34, the Oct 8 high, has been pierced. A clear move through it would expose key resistance at $65.77, Sep 26 high. The bear trigger is $55.96, the Oct 20 low. The downleg in Gold since Oct 20 appears to have been a correction and has allowed an overbought condition to unwind. Recent gains suggest the correction is over. Price remains above a key support at the 50-day EMA, at $3899.2. Clearance of this EMA would signal scope for a deeper retracement. Initial resistance is at $4161.4, the Oct 22 high. A stronger recovery would refocus attention on $4381.5, the Oct 20 high and bull trigger.

- WTI Crude down $0.58 or -0.95% at $60.47

- Natural Gas down $0 or -0.09% at $4.559

- Gold spot down $2.63 or -0.06% at $4124.23

- Copper up $0.2 or +0.04% at $506.75

- Silver up $0.56 or +1.08% at $51.787

- Platinum up $0.43 or +0.03% at $1587.14

| Date | GMT/Local | Impact | Country | Event |

| 12/11/2025 | 1140/1240 | ECB de Guindos at FIBI International Banking Conference | ||

| 12/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 12/11/2025 | 1205/1205 | BOE Pill in Panel at International Monetary Research Conference | ||

| 12/11/2025 | - | ECB Lagarde, Cipollone at Eurogroup Meeting in Brussels | ||

| 12/11/2025 | - | BOE MPG Meeting | ||

| 12/11/2025 | 1330/0830 | * | Building Permits | |

| 12/11/2025 | 1420/0920 | New York Fed's John Williams | ||

| 12/11/2025 | 1500/1000 | Philly Fed's Anna Paulson | ||

| 12/11/2025 | 1505/1005 | Kansas City Fed's Jeff Schmid | ||

| 12/11/2025 | 1520/1020 | Fed Governor Chris Waller | ||

| 12/11/2025 | 1730/1230 | Fed Governor Stephen Miran | ||

| 12/11/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 12/11/2025 | 1830/1330 | Bank of Canada meeting minutes | ||

| 12/11/2025 | 2050/1550 | New York Fed's Roberto Perli | ||

| 12/11/2025 | 2100/1600 | Boston Fed's Susan Collins | ||

| 13/11/2025 | 0030/1130 | *** | Labor Force Survey | |

| 13/11/2025 | 0700/0700 | *** | UK Monthly GDP | |

| 13/11/2025 | 0700/0800 | *** | Final Inflation Report | |

| 13/11/2025 | 0700/0700 | ** | Trade Balance | |

| 13/11/2025 | 0700/0700 | ** | Index of Services | |

| 13/11/2025 | 0700/0700 | ** | Index of Production | |

| 13/11/2025 | 0700/0700 | ** | Output in the Construction Industry | |

| 13/11/2025 | 0700/0700 | *** | GDP First Estimate | |

| 13/11/2025 | 0700/0800 | *** | Final Inflation Report | |

| 13/11/2025 | 0730/0730 | BOE MPG Minutes Released | ||

| 13/11/2025 | 0930/0930 | Productivity Flash Estimates | ||

| 13/11/2025 | 1000/1100 | ** | EZ Industrial Production | |

| 13/11/2025 | 1200/1200 | BOE Greene in Panel on Central Bank Independence | ||

| 13/11/2025 | - | *** | Money Supply | |

| 13/11/2025 | - | *** | New Loans | |

| 13/11/2025 | - | *** | Social Financing | |

| 13/11/2025 | - | ECB de Guindos at ECOFIN Meeting in Brussels | ||

| 13/11/2025 | 1300/1400 | ECB Elderson Moderates Climate and Banks Panel | ||

| 13/11/2025 | 1300/0800 | San Francisco Fed's Mary Daly | ||

| 13/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 13/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 13/11/2025 | 1330/0830 | *** | CPI | |

| 13/11/2025 | 1330/0830 | *** | CPI | |

| 13/11/2025 | 1330/0830 | *** | CPI | |

| 13/11/2025 | 1530/1030 | Minneapolis Fed's Neel Kashkari | ||

| 13/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 13/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 13/11/2025 | 1700/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 13/11/2025 | 1700/1200 | ** | US DOE Petroleum Supply | |

| 13/11/2025 | 1715/1215 | St. Louis Fed's Alberto Musalem | ||

| 13/11/2025 | 1720/1220 | Cleveland Fed's Beth Hammack | ||

| 13/11/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 13/11/2025 | 1900/1400 | ** | Treasury Budget |