KRW: KRW Suffers on Foreign Outflow, Reinforcing Link with Risk Appetite

Nov-07 15:46

- The latest spell of equity weakness at the open puts the e-mini S&P at new pullback lows of 6683.50, with bounce off lows so far today distinctly shallow. The risk-off sentiment is being keenly felt in KRW, which trades a new multi-month low against the USD today - despite the greenback dip on the UMich sentiment print.

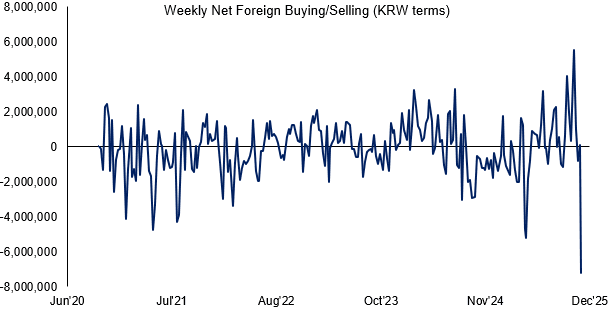

- 1460.30 in USDKRW is the highest since mid-April and the highest since Trump's Liberation Day tariff announcements and is consistent with acute profit-taking, likely via sizeable foreign equity outflow - evident in the KOSPI's 3.75% decline this week.

- The equity outflow pattern is clear to see in the KOSPI net foreign buying data - which today showed this week's cumulative net outflow the largest in five years in nominal KRW terms.

- This makes Korean equities, and thereby the Korean currency, particularly susceptible to concerns over AI valuations given the heavy reliance on the tech sector (semiconductors account for ~20% of all exports). Should these concerns materialize further into year-end, it may be too soon to call an end to the BoK easing cycle, with their next decision due on November 27th.

Source: MNI/Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROPEAN FISCAL: German Government GDP Revisions Likely To Lower Financing Gap

Oct-08 15:36

- Today's upward revisions of the German government's GDP estimates will likely have a net reductive impact on the current E172.3bln financing gap in the federal fiscal plan through 2029 relative to the estimates using the previous GDP assumptions.

- The new GDP forecast (0.2% 2025, 1.3% 2026, 1.4% 2027) will first flow into updated tax estimates scheduled for publication on October 23, and should, on balance, result in higher estimates for taxes including VAT, corporation tax, and income tax. Note that new legislation approved since the last estimates (includes the "growth booster" legislation package as well as the restaurant VAT decrease starting Jan 2026) will mechanically act counter to today's GDP impact.

- These tax estimates will subsequently be used in the finance ministry's financial plans / budget calculations.

FED: US TSY 17W BILL AUCTION: HIGH 3.775%(ALLOT 33.62%)

Oct-08 15:32

- US TSY 17W BILL AUCTION: HIGH 3.775%(ALLOT 33.62%)

- US TSY 17W BILL AUCTION: DEALERS TAKE 24.91% OF COMPETITIVES

- US TSY 17W BILL AUCTION: DIRECTS TAKE 3.70% OF COMPETITIVES

- US TSY 17W BILL AUCTION: INDIRECTS TAKE 71.39% OF COMPETITIVES

- US TSY 17W BILL AUCTION: BID/CVR 3.28

FED: Any Balance Sheet/Admin Rates Discussion Eyed, Analysts Mixed On Tone (3/3)

Oct-08 15:32

In more of a curiosity, we will be intrigued by how Miran's last-minute introduction to the Committee translates into the description of the proceedings. In particular it will be no surprise given his dissent and “dot” for 150bp of cuts this year if there is “a” participant that argues vociferously for aggressive front-loaded cuts.

- We'll be looking for any discussion about balance sheet policy. The meeting preceded September’s quarter/month-end pressures and drawdown of reserves below the $3T mark, and it may soon be time for the Committee to make decisions about how it will handle the transition from abundant to ample reserves. (We note also that the NY Fed’s latest survey of market participants should be out today, offering the latest consensus take on when QT will end and at what size of Fed balance sheet.)

- Additionally, Dallas Fed President Logan’s comments on the Fed selecting a new policy target rate (she eyes TGCR) to replace the Fed funds rate raise the question of whether the FOMC discussed more technical operational aspects at this meeting.

Some sell-side analysts’ identified areas to watch:

- BMO: “will be of particular relevance as it relates to the Fed's recent shift toward outweighing the employment aspect of its mandate over inflation. The benchmark revisions and lackluster payroll gains this summer were an inflection point for the Fed and investors. After all, the loss of the ‘labor market is resilient’ mantra has ushered in a re-think of how restrictive policy has been and, therefore, how quickly the Fed should seek to return to neutral. As September was Miran’s first FOMC meeting, the market will be watching the Minutes for any response on the Committee to his decidedly more dovish stance, even if the tone of the official communication will surely err on the side of diplomatic.”

- BofA: “we will be looking to understand why the Fed projected deeper cuts than in June despite moving to more hawkish macro forecasts.”

- Deutsche: “Though we have heard the majority of Fed officials since the meeting, the minutes could nonetheless shed some further light on the wide rift amongst officials with respect to the policy outlook… Aside from views on the current policy outlook in the minutes, we will also focus on potential staff presentations related to the Fed’s policy implementation framework.

- ING: “What we’ll be looking for in the minutes is evidence that Chair Jerome Powell’s cautious view on further cuts is shared by the majority of the FOMC. The risks appear slightly tilted to the dovish side and therefore to a negative USD reaction to the minutes.”

- Natixis: “The debate was likely lively given the vastly different economic forecasts and disperse views on the Fed’s appropriate reaction function to ongoing economic developments.”

- TD: “likely to highlight the division on the Committee between the hawks and doves. Most participants likely saw the policy recalibration as necessary. However, we expect some participants saw further easing this year as unlikely given tariff-driven inflation risks. Many participants likely anticipate further easing owing to labor market risks.”