MNI US MARKETS ANALYSIS - Tsys Hold Firm, Busy Fedspeak Ahead

Highlights:

- Treasuries hold near top-end of range ahead of busy Fedspeak session

- MNI compiles “Shadow” Employment Report, with alternative measures painting a mixed picture for jobs

- AUD slides as employment softer than expected in September, August revised lower too

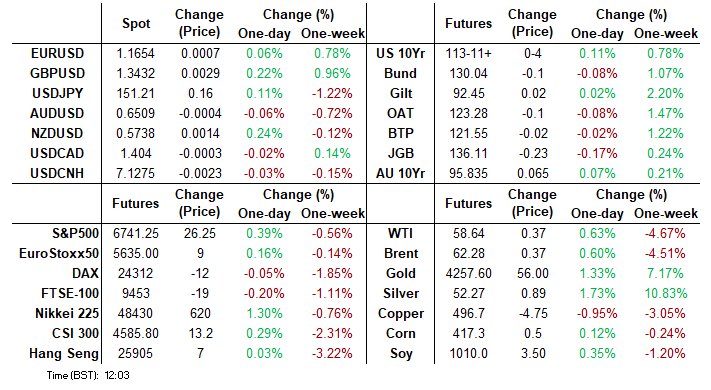

US TSYS: Mildly Firmer Within Ranges, State-Level Claims Data Watched Late On

- Treasuries are mildly firmer on the day, comfortably within yesterday’s range, having struggled to move below 4% 10Y yields earlier this week.

- Today sees heavy Fedspeak, albeit from some repeat speakers plus data focus on regional Fed measures before state-level claims later on when they should be released in the afternoon. President Trump is set to make an announcement this afternoon but with no known topic just yet.

- Cash yields are 0.5-1.5bp lower across the curve, within yesterday’s range.

- 10Y yields (currently 4.020%, -0.8bps) again tested the 4% handle yesterday on two separate occasions, including a low of 3.9975% after Tuesday’s 3.9976%, finding clear support at this level. Whilst there were brief clearances on Sep 17 and Sep 11, yields were last materially sub-4% in early April under reciprocal tariff deliberations.

- TYZ5 trades at 113-11+ (+04) on subdued cumulative volumes of 230k.

- Tue/Wed highs of 113-17+ mark initial resistance ahead of a bull trigger at 113-29 (Sep 11 high). Alternatively, the recent uplift has dragged support up to 112-27+ (20-day EMA).

- Data: Philly Fed mfg (0830ET), NY Fed services Oct (0830ET), NAHB housing index Oct (1000ET), Dallas Fed weekly economic index (1130ET), State-level jobless claims likely to be released from afternoon ET

- Fedspeak: Miran on Fox (~0700ET), Waller on BBG TV (~0730ET), Waller (0900ET), Barr (0900ET), Miran (0900ET), Bowman (1000ET), Miran (1615ET), Kashkari (1800ET) – see Fedspeak bullet.

- Bill issuance: US Tsy $110B 4W, $95B 8W bill auctions (1130ET)

- Politics: Trump makes an announcement (1500ET)

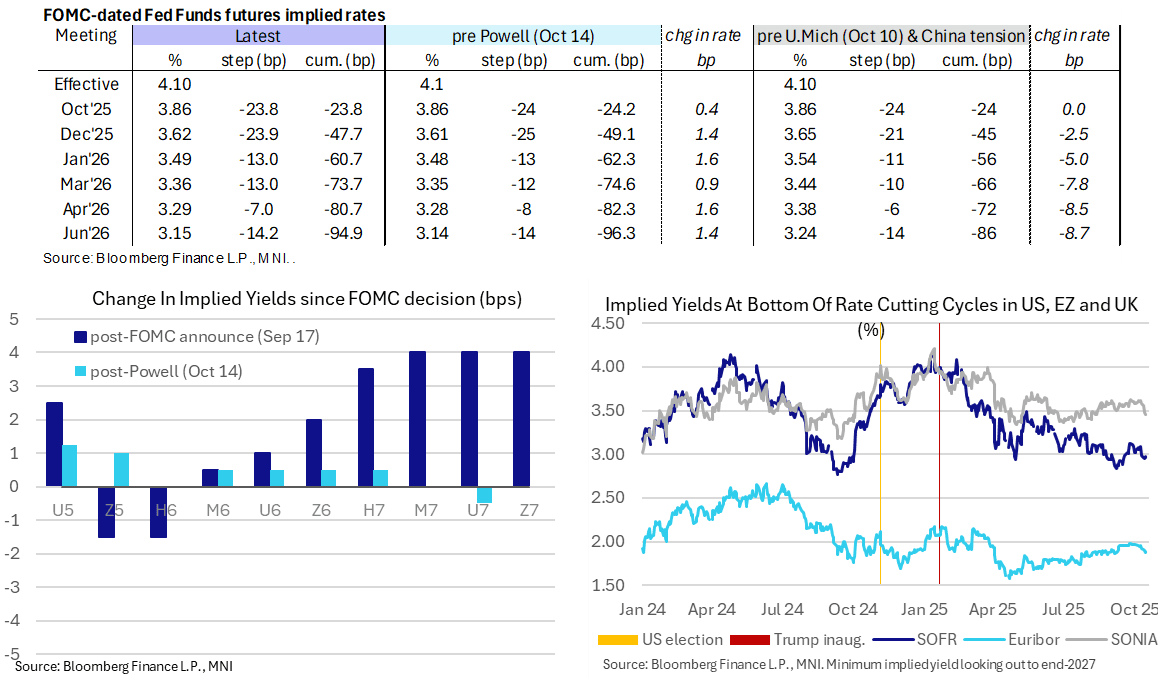

STIR: Fed Rates Holding Recent Narrow Ranges

- Fed Funds implied rates are little changed overnight, still hovering just shy of fully pricing back-to-back cuts in the two meetings left for this year.

- Cumulative cuts from 4.10% effective: 24bp Oct, 47.5bp Dec, 60.5bp Jan, 73.5bp Mar, 80.5bp Apr and 95bp Jun.

- SOFR futures range from unchanged to +1.5 ticks looking out to end-2027 contracts.

- The SOFR implied terminal yield of 2.965% (SFRZ6 and H7) is 1bp lower on the day, holding within narrow ranges having closed between 2.95-2.975% so far this week.

- It points to at least 4.5x25bp cuts ahead depending on fixed rate assumptions.

- Yesterday's Fed Beige Book noted that overall economic activity looks to have been weaker on balance than prior although it was arguably its joint most inflationary from the description of prices. The employment picture was relatively unchanged to slightly improved at least compared to the prior report, but still considerably weaker than earlier in the year (mirroring broader employment data).

FED: Waller Probably The Pick Of Today’s Heavy Fedspeak

- Today sees another heavy day of Fedspeak in the last week before the FOMC blackout, although most have spoken recently.

- One area we’ll watch is whether Fed Governor Waller, reportedly still on the shortlist for next Fed Chair, is more dovish than prior measured remarks as was the case with Miran yesterday.

- Miran cited a new tail risk from trade tensions: “There’s now more downside risks than there was a week ago […] “I wouldn’t say that I want even lower rates now than I did a week or a month ago. However, with the change to the balance of risks, I think it becomes even more urgent that we get to a more neutral place in policy quickly.” Going against that, yesterday’s Beige Book was arguably the joint most inflationary Beige Book of 2025 when it comes to price comments.

- Speaking on CNBC on Friday, Waller unsurprisingly affirmed his view that the Fed should follow through with a series of cuts in light of developing labor market weakness (saying the labor market is "not tight in any way, shape or form"). While it's clear he's among the most dovish members on the Committee, eyeing 2 more rate cuts this year, he doesn't advocate too aggressive an easing: "I'm still in the belief we need to cut rates, but we need to kind of be cautious about it."

Today’s schedule:

- ~0700ET – Gov. & CEA’s Miran (voter, dove) on Fox Business

- ~0730ET – Gov. Waller (voter, dove) on Bloomberg TV

- 0900ET – Gov. Waller (voter, dove) at Council on Foreign Relations (text + Q&A)

- 0900ET – Gov. Barr (voter) on stablecoins (text + Q&A)

- 0900ET – Gov. & CEA’s Miran (voter, dove) in IIF moderated conservation (no text)

- 1000ET – VC Supervision Bowman (voter, dove) at stress testing research conference (text only)

- 1000ET – Gov. & CEA’s Miran (voter, dove) in Semafor moderated conversation (no text)

- 1800ET – Kashkari (’26 voter) in town hall event (no text)

MNI US Employment Report, Oct 2025: Labor Market Stays Soft

DOWNLOAD FULL REPORT HERE

Executive Summary

- With the BLS’s nonfarm payrolls report for September delayed indefinitely, MNI has compiled a “Shadow” Employment Report that assesses latest developments via the data we do have for the month.

- Alternative private sector indicators of jobs growth paint a mixed picture on the extent of the latest additional softening beyond that seen in latest BLS payrolls data to August.

- With ratios keenly watched by FOMC members, various unemployment rate metrics point to further increases including to new recent highs in the Chicago Fed’s final indicators report.

- State-level jobless claims data look contained though, with the labor market still best characterized as in a low fire, low hire state.

US TSY FUTURES: Net Short Setting & Long Cover Seen On Wednesday

OI data points to a mix of net short setting (TU, FV, TY & WN) and long cover (UXY & US) as Tsy futures ticked lower on Wednesday.

- The former was slightly more prominent, with the most meaningful DV01 adjustment coming via the net short setting seen in WN.

| 15-Oct-25 | 14-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,561,715 | 4,553,734 | +7,981 | +310,777 |

FV | 6,715,928 | 6,693,946 | +21,982 | +960,878 |

TY | 5,410,600 | 5,409,869 | +731 | +49,607 |

UXY | 2,463,933 | 2,466,185 | -2,252 | -204,942 |

US | 1,878,415 | 1,880,796 | -2,381 | -308,313 |

WN | 2,071,970 | 2,064,636 | +7,334 | +1,400,353 |

|

| Total | +33,395 | +2,208,359 |

SOFR: Mix Of Long Cover & Short Setting In Futures On Wednesday

OI data points to a mix of net long cover and short setting as SOFR futures ticked lower on Wednesday.

- Net long cover was slightly more prominent in the whites, before net short cover came to the fore further out the strip.

| 15-Oct-25 | 14-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,423,545 | 1,425,083 | -1,538 | Whites | -3,931 |

SFRZ5 | 1,553,164 | 1,544,991 | +8,173 | Reds | +29,803 |

SFRH6 | 1,124,693 | 1,137,141 | -12,448 | Greens | +9,973 |

SFRM6 | 1,024,370 | 1,022,488 | +1,882 | Blues | +8,381 |

SFRU6 | 1,008,497 | 1,009,768 | -1,271 |

|

|

SFRZ6 | 1,027,678 | 1,008,008 | +19,670 |

|

|

SFRH7 | 816,957 | 802,745 | +14,212 |

|

|

SFRM7 | 781,170 | 783,978 | -2,808 |

|

|

SFRU7 | 686,148 | 680,903 | +5,245 |

|

|

SFRZ7 | 773,574 | 749,910 | +23,664 |

|

|

SFRH8 | 425,118 | 440,799 | -15,681 |

|

|

SFRM8 | 373,657 | 376,912 | -3,255 |

|

|

SFRU8 | 306,465 | 302,753 | +3,712 |

|

|

SFRZ8 | 329,356 | 327,253 | +2,103 |

|

|

SFRH9 | 194,499 | 193,814 | +685 |

|

|

SFRM9 | 174,304 | 172,423 | +1,881 |

|

|

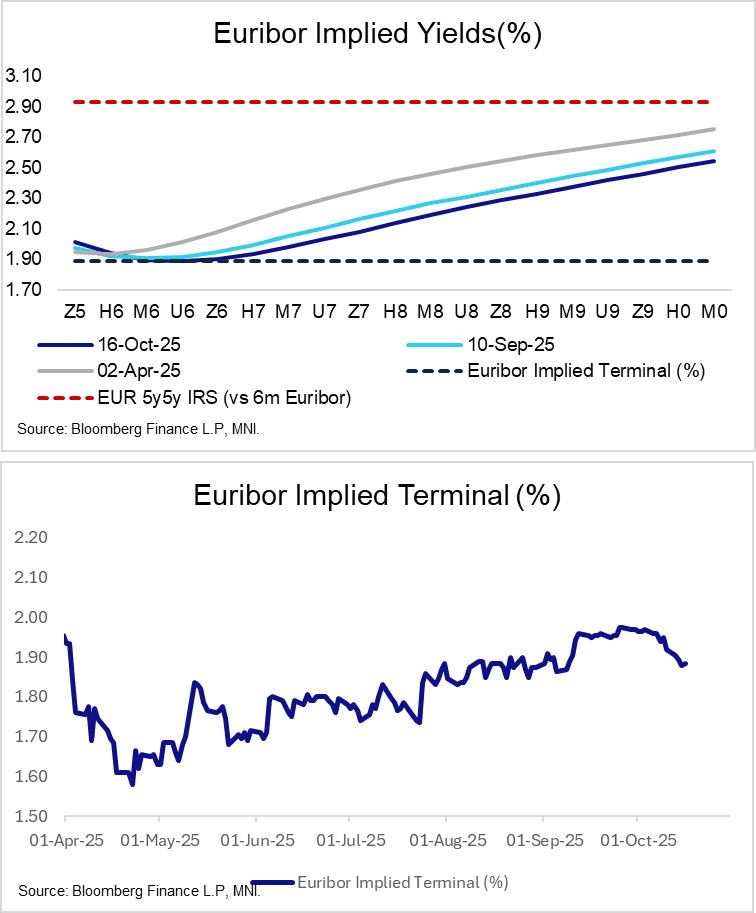

STIR: Euribor Implied Terminal May Struggle To Push Through 1.90% Without Data

The Euribor implied terminal rate may struggle to push meaningfully below 1.90% in the absence of fresh data catalysts. ECB speakers are unlikely to deviate materially from their prior stances, and near-term French political risks have eased from recent extremes with PM Lecornu likely to survive today’s no-confidence votes.

- The terminal rate is now indicated by the U6 contract (previously M6), currently at 1.89%.

- Across the strip, futures are little changed versus yesterday’s settlement levels.

- ECB-dated OIS price ~17.5bps of easing through September 2026. While risks still tilt towards another rate cut this cycle, Governing Council members will need to be convinced by incoming data to justify such a move. Focus remains on the flash PMI, GDP and inflation reports towards the end of this month.

- Today’s regional calendar sees Eurozone August merchandise trade data released. ECB’s Wunsch, Lane and Lagarde are scheduled to speak from the IMF/World Bank meetings in DC.

FOREX: AUDNZD Fades Hard, GBP Outperforms on Better Fiscal Picture

- AUDNZD faded hard today. AUD slipped overnight, pushing prices below the 0.6500 figure following a very poor employment report. Both the employment change headline and unemployment rate were weaker than expected, while the August release was marked lower in the first revision. This put the unemployment rate at a 4 year high, forcing markets to consider an accelerated pace of RBA rate cuts going forward.

- Cementing the theme, local desks note some potential position squaring and profit-taking in AUDNZD which could be putting the mullti-month uptrend at risk. NZDUSD is off highs, but remains higher by ~0.2% in early trade. As such, the price hasn't managed to break above Monday's high at 0.5759.

- As a November RBA cut is becoming more likely, AUDNZD lost 0.4% on the session at 1.1337. AU-NZ 2yr swap rates are not implying further sharp AUDNZD downside - despite the recent run higher in the cross. Monday's Q3 NZ CPI will be the next key input.

- GBP modestly outperforms. UK August activity data was broadly inline and is unlikely to have any real impact on the next BoE decision, however Gilt futures have steadied as markets see marginally less fiscal tightening required at the November Autumn Budget than many envisage, particularly as the Chancellor signalled that taxes on the wealthy will be “part of the story”. EURGBP is lower for a second session, again proving the resilience of the 0.8676 as a key anchor level.

- Tomorrow's negotiations between Japanese LDP and Ishin parties will be the next leg in LDP leader Takaichi's attempt to be elected as the next PM next Tuesday following the failure of leader-level discussions earlier today. Ishin leader Fujita said today they will decide by Monday whether or not to join a coalition, meaning the day could prove decisive for Takaichi's fate, her expansionary agenda, and subsequently, USDJPY trends in the short- to medium term.

- Today was originally set to see the concurrent release of retail sales, PPI and weekly jobless claims from the US, but the extended government shutdown (which the Treasury now estimate is costing the US economy ~$15bln per day) will delay these releases. Instead, alternative measures remain of primary focus - keeping the Philly Fed Business Outlook and New York Fed Services Business Activity data in the spotlight.

- In central bank speak, Fed's Waller, Barr, Miran, Bowman & Kashkari are all due to speak as FOMC members look to set the tone before the pre-meeting media blackout kicks in at tomorrow's close. BoE's Mann & Greene and ECB's Wunsch, Lane and Lagarde all appear at the IMF/World Bank Forum in Washington DC.

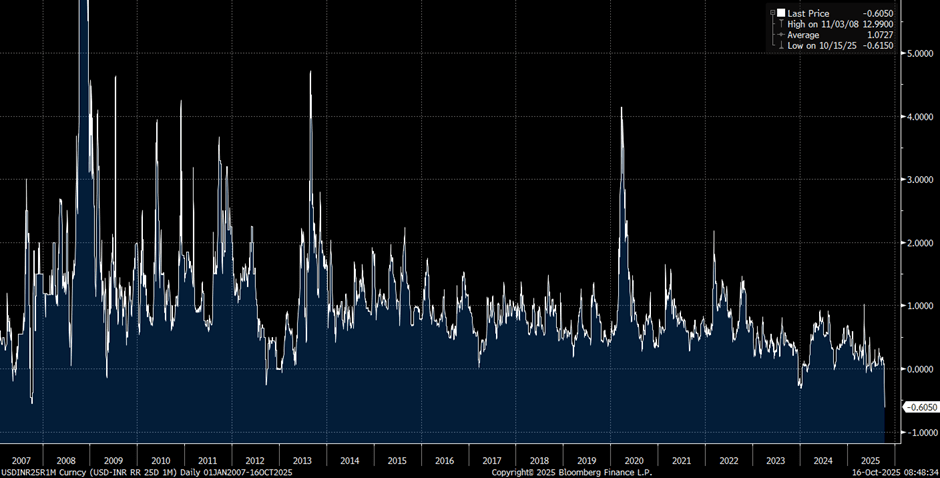

INR: Risk of USD/INR Downside Evident via Options, RBI Continue to Intervene

Reports yesterday from Bloomberg and Reuters pointed to heavy FX intervention by the RBI in both the onshore and offshore market, with further intervention seen as highly likely given that the central bank sees the recent build up in short rupee positions as speculative. Reuters report, citing traders, that the RBI sold an estimated $3-5bln – its heaviest round of intervention in months – with significant activity noted to have taken place in the NDF market.

- Bloomberg report that the central bank continued with its intervention on Thursday, albeit at a relatively smaller scale compared to yesterday. USD/INR has fallen a further 0.2% today, placing the pair at its lowest level since September and below the 50-day EMA – an average spot has not closed below since July. The 100-DMA, at 87.0609, marks next notable support.

- Given the likelihood of further intervention, net downside demand for USD/INR is still evident via options, tipping the vol skew firmly in favour of puts – 1-month USD/INR risk reversals are currently at their most negative since 2007 (see chart below).

- Indeed, MUFG think that short INR positions will probably be reduced in the near-term given RBI’s strong signal. Over the medium-term, they still think that some modest FX weakness is not a bad thing for India given the global uncertainties and to maintain some export competitiveness. MUFG therefore say they will be biased to look for opportunities to go long USD/INR later depending on where FX settles.

- Yesterday, SocGen recommended initiating a short position in 1-month USD/INR at 88.28, targeting 86.00 with a stop at 89.40. They believe that USD/INR has already priced in most of the key INR-negative factors, and that the RBI’s pledge to stabilise the currency presents a compelling case for a tactically short USD/INR trade.

Figure 1: 1-month USD/INR 25d risk reversal

Source: Bloomberg Finance L.P.

OPTIONS: Expiries for Oct16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-20(E1.5bln), $1.1580-00(E4.0bln), $1.1650-55(E783mln), $1.1700-05(E1.2bln), $1.1735-40(E837mln)

- USD/JPY: Y150.50($729mln), Y151.00($511mln), Y152.00($728mln)

- AUD/USD: $0.6500-20(A$598mln)

- USD/CAD: C$1.3975($946mln)

EQUITIES: Eurostoxx Trend Remains Up Despite Friday's Sharp Pullback

- The trend direction in Eurostoxx 50 futures is up and the latest pullback appears to have been a correction. The contract remains above key support at 5487.08, the 50-day EMA. A clear break of the 50-day average is required to highlight a stronger reversal. On the upside, the bull trigger is 5689.00, the Oct 2 high. Clearance of this hurdle would confirm a resumption of the uptrend.

- A sharp sell-off in S&P E-Minis on Oct 10 appears corrective - for now. Price has found support below the 50-day EMA, currently at 6609.91, and the Oct 10 low of 6540.25 has been defined as a key short-term support. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. The bull trigger is 6812.25, the Oct 9 high. A breach of this hurdle would confirm a resumption of the uptrend.

COMMODITIES: Tuesday's Cycle Low Reinforces Bearish WTI Futures Trend

- A bearish theme in WTI futures remains intact and Tuesday’s fresh cycle low reinforces current conditions. The move down last week resulted in a break of support at $60.40, the Oct 2 low. This highlights an extension of the bearish price sequence of lower lows and lower highs and the move down opens $57.50 next, the May 30 low. On the upside, key resistance is at $66.42, the Sep 29 high. First resistance is at $62.30, the 50-day EMA.

- A bull cycle in Gold remains intact and this week’s extension reinforces current conditions. The move higher maintains the price sequence of higher highs and higher lows. Sights are on the $4300.00 handle next, and $4317.7, a Fibonacci projection point. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support to watch lies at $3919.6, 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 16/10/2025 | 1200/0800 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/10/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 16/10/2025 | 1300/1400 | BOE Mann in Panel on MonPol and Trade Shocks | ||

| 16/10/2025 | 1300/0900 | Fed Governor Christopher Waller | ||

| 16/10/2025 | 1300/0900 | Fed Governor Michael Barr | ||

| 16/10/2025 | 1300/0900 | Fed Governor Stephen Miran | ||

| 16/10/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/10/2025 | 1400/1000 | Fed Governor Michelle Bowman | ||

| 16/10/2025 | 1445/1545 | BOE Mann in MonPol Panel at IMF/World Bank Meetings | ||

| 16/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 16/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 16/10/2025 | 1545/1745 | ECB Lane in Policy Panel at IIF Annual Meeting | ||

| 16/10/2025 | 1600/1800 | ECB Lagarde in IMF Policy Debate | ||

| 16/10/2025 | 1645/1245 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 1730/1330 | BOC Governor Macklem speaks at Peterson Institute event in Washington. | ||

| 16/10/2025 | 1830/1930 | BOE Greene in Panel on UK/EU Relations | ||

| 16/10/2025 | 2015/1615 | Fed Governor Stephen Miran | ||

| 16/10/2025 | 2030/1630 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 2200/1800 | Minneapolis Fed's Neel Kashkari | ||

| 17/10/2025 | 0600/0800 | ** | Unemployment | |

| 17/10/2025 | 0900/1100 | *** | EZ HICP Final | |

| 17/10/2025 | 0935/1035 | BOE Pill Speech at Institute of Chartered Accountants Conference | ||

| 17/10/2025 | 1100/1200 | BOE Greene Roundtable at Atlantic Council | ||

| 17/10/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/10/2025 | 1615/1215 | St. Louis Fed's Alberto Musalem | ||

| 17/10/2025 | 1630/1730 | BOE Breeden in Panel at IMF/World Bank Meetings | ||

| 17/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/10/2025 | 2000/1600 | ** | TICS |