INR: Risk of USD/INR Downside Evident via Options, RBI Continue to Intervene

Oct-16 08:28

Reports yesterday from Bloomberg and Reuters pointed to heavy FX intervention by the RBI in both the onshore and offshore market, with further intervention seen as highly likely given that the central bank sees the recent build up in short rupee positions as speculative. Reuters report, citing traders, that the RBI sold an estimated $3-5bln – its heaviest round of intervention in months – with significant activity noted to have taken place in the NDF market.

- Bloomberg report that the central bank continued with its intervention on Thursday, albeit at a relatively smaller scale compared to yesterday. USD/INR has fallen a further 0.2% today, placing the pair at its lowest level since September and below the 50-day EMA – an average spot has not closed below since July. The 100-DMA, at 87.0609, marks next notable support.

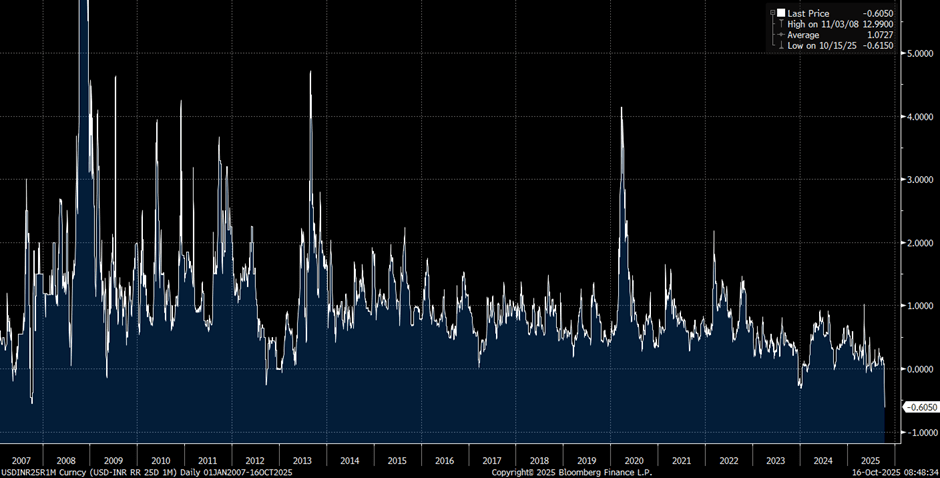

- Given the likelihood of further intervention, net downside demand for USD/INR is still evident via options, tipping the vol skew firmly in favour of puts – 1-month USD/INR risk reversals are currently at their most negative since 2007 (see chart below).

- Indeed, MUFG think that short INR positions will probably be reduced in the near-term given RBI’s strong signal. Over the medium-term, they still think that some modest FX weakness is not a bad thing for India given the global uncertainties and to maintain some export competitiveness. MUFG therefore say they will be biased to look for opportunities to go long USD/INR later depending on where FX settles.

- Yesterday, SocGen recommended initiating a short position in 1-month USD/INR at 88.28, targeting 86.00 with a stop at 89.40. They believe that USD/INR has already priced in most of the key INR-negative factors, and that the RBI’s pledge to stabilise the currency presents a compelling case for a tactically short USD/INR trade.

Figure 1: 1-month USD/INR 25d risk reversal

Source: Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOBL: Block trade

Sep-16 08:08

Bobl Block trade, suggest seller:

- OEZ5 ~3k at 117.89.

GILTS: Flat Start, Limited By Labour Market Data

Sep-16 08:04

Gilts little changed, futures steady around 91.50.

- A bullish cycle remains in play. Initial resistance at 91.82. Initial support at 90.65.

- Yields within 0.5bp of yesterday’s close.

- Cross-market, gilts giveback some of yesterday’s outperformance vs. Bunds on the back of the firmer-than-expected quantity side of the labour market data.

- We don’t think this data will be gamechanger for the BoE, particularly with wage data slightly softer than expected at this early stage in the Q3 cycle (see our earlier run of post-data bullets for more colour).

- A reminder that we have CPI data tomorrow ahead of the BoE decision on Thursday.

- Our detailed CPI preview can be found here.

- Focus following Thursday’s BoE decision is likely to fall on the QT decision for 25/26, with consensus looking for no change in Bank Rate.

- There is plenty of uncertainty around the QT decision and given that the size of the balance sheet is to approach the top of the PMRR range through passive reduction alone, we would argue that either active sales continuing at their current pace or being suspended completely would be the optimal position for the market.

- Former MPC member Wadhwani suggested that the BoE should stop active gilt sales

- Analysts are split on whether there will be a skew away from long-dated gilts being sold.

- On the issuance front, the DMO will sell GBP3bln of the 4.375% Jan-40 gilt this morning.

- U.S. President Trump’s state visit is set to provide headlines over the next 48 hours, with U.S. firms outlining increased investment intentions re: the UK in recent days.

MNI: ITALY AUG FINAL HICP 1.6% (VS 1.7% FLASH, 1.7% JUL)

Sep-16 08:03

- MNI: ITALY AUG FINAL HICP 1.6% (VS 1.7% FLASH, 1.7% JUL)